AI Compute Express Link Switch Market Insights

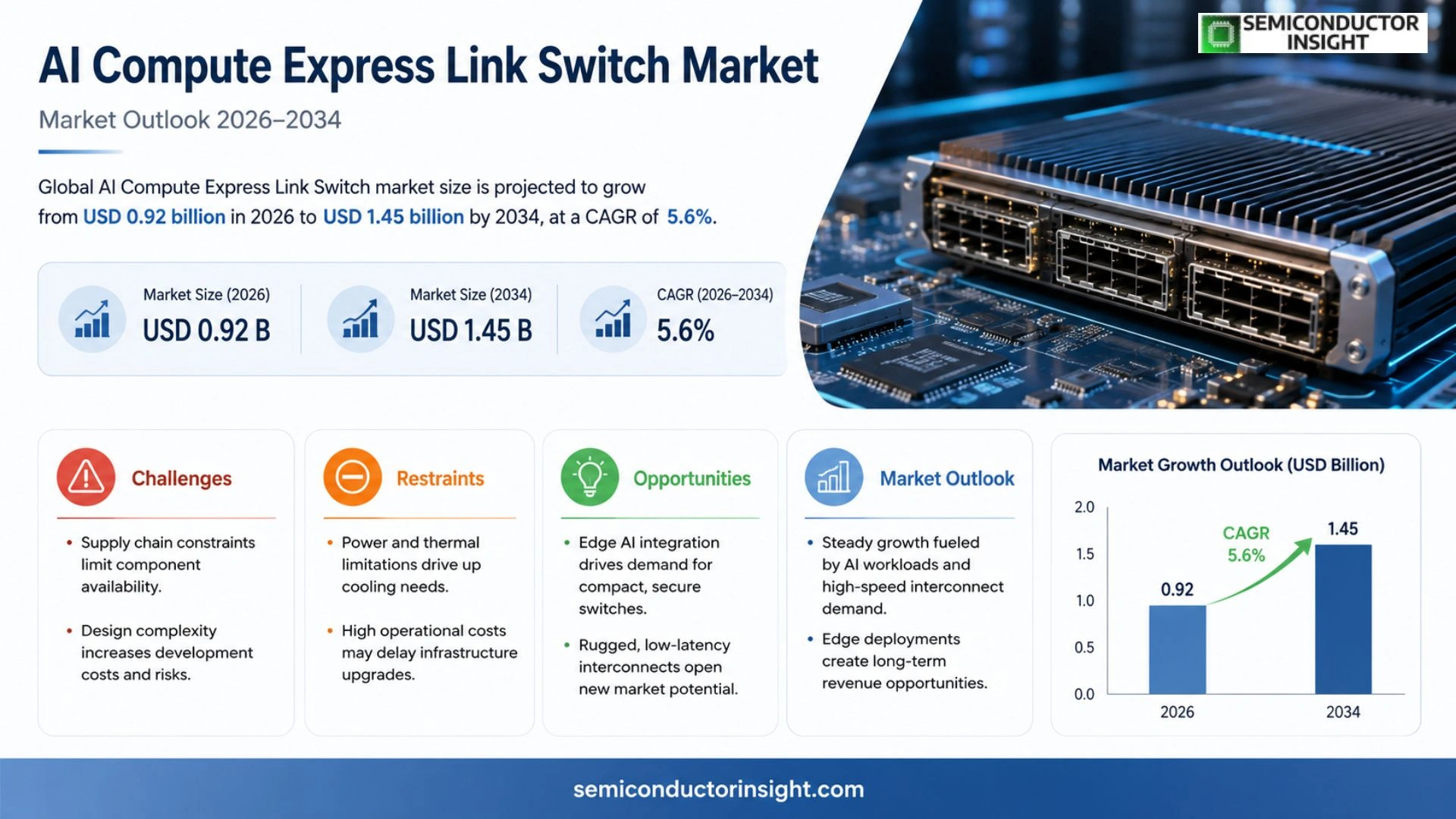

Global AI Compute Express Link Switch market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period.

AI Compute Express Link (CXL) switches are high‑speed interconnect devices that enable coherent memory sharing between CPUs, GPUs, accelerators and memory buffers within data‑center servers.

The expansion is fueled by rising demand for heterogeneous computing workloads, especially in artificial‑intelligence training and inference where low‑latency bandwidth is critical.

Furthermore, increased capital spending on next‑generation data centers and broader adoption of CXL standards by major silicon vendors accelerate uptake.

Key suppliers such as Nvidia Corporation, Intel Corporation, and Advanced Micro Devices, together with emerging players like Marvell Technology, are delivering modular switch portfolios that address evolving performance requirements.

MARKET DRIVERS

Growing Demand for Low‑Latency Interconnects

The surge in AI model sizes has forced data‑center operators to replace traditional Ethernet fabrics with solutions that can move terabytes of data in microseconds. AI Compute Express Link Switch Market players that deliver sub‑microsecond round‑trip times are witnessing contracts that outpace legacy vendors, because latency directly translates into inference throughput for cloud providers.

Shift Toward Heterogeneous Computing

Enterprises are assembling clusters that combine GPUs, FPGAs, and ASICs to optimise specific workloads. The interconnect layer must understand divergent memory architectures and expose coherent access across devices. Switch manufacturers that embed protocol translation and memory‑side caching gain a competitive edge, as system architects seek to avoid bottlenecks when scaling mixed‑precision training.

➤ “The ability to sustain 400 GB/s per lane while preserving cache coherency is becoming the de‑facto benchmark for next‑gen AI data centers.”

Finally, the rollout of 5G and private‑network slices creates a new class of edge installations where AI inference must happen locally. Deployments that pair compact switches with AI accelerators reduce backhaul demand and open revenue streams beyond the traditional cloud segment.

MARKET CHALLENGES

Supply Chain Constraints

Semiconductor fab capacity is still recovering from recent disruptions, and high‑performance transceiver wafers are allocated to a limited set of OEMs. This scarcity drives lead times upward, forcing system builders to hold larger inventories or accept lower‑spec alternatives, which in turn slows adoption of the latest switch topologies.

Other Challenges

Design Complexity

Engineers must navigate a growing matrix of standards,CXL, PCIe 6.0, and proprietary memory protocols. The learning curve inflates development budgets and raises the risk that early‑stage projects miss performance targets, discouraging risk‑averse enterprises.

MARKET RESTRAINTS

Power and Thermal Limitations

High‑density AI racks push power budgets toward 30 kW per cabinet. Switches that deliver multi‑terabit throughput often require sophisticated cooling solutions, adding capital expense and operational overhead. Operators reluctant to overhaul facility HVAC systems may postpone upgrades, thereby tempering market expansion.

MARKET OPPORTUNITIES

Edge AI Integration Boosts Prospects

Manufacturers that package AI‑ready switches with embedded security modules are positioned to capture the burgeoning edge market. As automotive, manufacturing, and healthcare sectors deploy on‑premise analytics, the need for compact, low‑latency interconnects that can operate in rugged environments creates a revenue corridor that remains largely untapped.

AI Compute Express Link Switch Market Trends

Rising Adoption of CXL Switches in Heterogeneous AI Workloads

AI Compute Express Link Switch Market is witnessing a shift as enterprises restructure server architectures to accommodate mixed‑precision AI models. By linking CPUs, GPUs, and specialized accelerators through a coherent memory fabric, CXL switches eliminate bottlenecks that traditionally forced designers to over‑provision discrete memory pools. This architectural efficiency translates into lower total cost of ownership for data‑center operators, especially those running large‑scale training cycles where latency directly influences time‑to‑insight. Consequently, procurement teams are prioritizing switch solutions that deliver the highest bandwidth per watt, a metric that now outweighs raw port count in many RFPs. The trend reshapes vendor negotiations, pushing suppliers to certify interoperability across multiple silicon families and to offer firmware that can be tuned for specific inference workloads.

Other Trends

Capital Investment in Next‑Generation Data Centers

Investment cycles for hyperscale facilities have accelerated, with operators channeling a larger share of capex toward platforms that natively support the CXL protocol. The rationale is twofold: first, the protocol’s ability to share memory buffers reduces the number of physical DIMM slots required, freeing rack space for additional compute cards; second, the modular nature of CXL switches enables incremental upgrades without wholesale server replacement. This financial model appeals to firms that must balance rapid AI deployment against long‑term asset depreciation. As a result, procurement roadmaps now embed CXL‑ready switch racks as a baseline component, prompting system integrators to redesign cooling and power distribution schemes around the denser, yet more efficient, interconnect topology.

Broadening Supplier Ecosystem and Modular Switch Portfolios

The competitive landscape around AI Compute Express Link Switch Market is expanding beyond the traditional trio of Nvidia, Intel, and AMD. New entrants such as Marvell are introducing modular switch families that can be daisy‑chained to scale bandwidth on demand. This diversification gives data‑center managers the leverage to negotiate pricing based on performance per port rather than vendor lock‑in. Moreover, the emergence of open‑source firmware initiatives encourages faster adoption of feature updates, reducing time between silicon release and production deployment. For OEMs, the ability to source switches from multiple suppliers mitigates supply‑chain risk and supports regional compliance requirements. The net effect is a more resilient market where innovation is driven by direct feedback from AI workload engineers, accelerating the evolution of interconnect standards.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Compute Express Link Switch Market – Competitive Overview

The market’s leadership is anchored by a small group of silicon giants that have integrated CXL switch capability into their broader portfolio of data‑center products. Nvidia’s acquisition of Mellanox gave it a decisive edge in high‑bandwidth, low‑latency interconnects, allowing the firm to bundle GPU accelerators with native CXL support. Intel leverages its long‑standing relationships with server OEMs, embedding CXL switch logic directly into its Xeon processor line and offering a modular architecture that scales from rack‑level to hyperscale deployments. AMD, following the Xilinx integration, provides a programmable approach that appeals to customers seeking flexibility across training, inference and emerging workloads. Together these three dictate pricing trends and set reference designs that shape downstream adoption.

Beyond the tier‑1 cohort, a second wave of competitors is enriching the ecosystem with differentiated form factors and niche performance attributes. Marvell Technology supplies silicon‑based switch ASICs that prioritize power efficiency for edge‑centric AI clusters. Broadcom’s portfolio emphasizes dense port counts suitable for hyperscale operators. Samsung Electronics contributes memory‑centric CXL solutions that capitalize on its expertise in high‑bandwidth DRAM packaging. Qualcomm is positioning its compute‑offload chips with integrated CXL interfaces to capture the mobile‑AI crossover market. Smaller innovators such as Esperanto Technologies and Graphcore are experimenting with custom datapaths that could reshape the performance‑per‑watt calculus. The presence of Cisco, Dell Technologies and Google as solution integrators further blurs the line between pure component suppliers and end‑to‑end system providers, compelling incumbents to broaden their go‑to‑market strategies.

List of Key AI Compute Express Link Switch Companies Profiled

- Nvidia Corporation

- Intel Corporation

- Advanced Micro Devices, Inc. (AMD)

- Marvell Technology Group Ltd.

- Broadcom Inc.

- Samsung Electronics Co., Ltd.

- Qualcomm Incorporated

- Cisco Systems, Inc.

- Dell Technologies Inc.

- Google (Alphabet Inc.)

- Esperanto Technologies

- Graphcore Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Programmable Switches are favored for their adaptability to evolving AI workloads, enabling dynamic reconfiguration of bandwidth pathways; they support a broader ecosystem of accelerators and foster rapid integration of new CXL revisions; designers appreciate the flexibility to fine‑tune latency and resource allocation without hardware redesign. |

| By Application |

|

AI Training Accelerators drive the demand for ultra‑low latency interconnects, requiring coherent memory sharing across multiple GPUs; the need for seamless scaling of compute nodes pushes vendors to emphasize switch architectures that minimize data movement overhead; solution providers value the ability to maintain deterministic performance as model sizes grow. |

| By End User |

|

Cloud Service Providers prioritize modular switch designs that simplify fleet upgrades and support multitenant isolation; they value the ability to auto‑scale interconnect capacity as customer workloads fluctuate; emphasis is placed on energy‑efficient operation to align with large‑scale sustainability goals. |

| By Performance Tier |

|

High‑End offerings command attention for mission‑critical AI workloads where deterministic latency and maximum bandwidth are non‑negotiable; customers appreciate integrated diagnostics and firmware that evolve with AI software stacks; the tier is also associated with robust thermal design to sustain peak performance under intensive compute cycles. |

| By Integration Mode |

|

On‑Board Integrated solutions are prized for minimizing physical footprint and reducing signal latency by embedding the switch within the server motherboard; this approach simplifies cabling and enhances power efficiency; designers also note the advantage of tighter coexistence with CPU and GPU memory controllers, fostering smoother coherent operations. |

Regional Analysis: AI Compute Express Link Switch Market

Major cloud providers are allocating capital toward modular data‑center designs that embed express‑link switches at the rack level, enabling seamless GPU scaling without re‑architecting the underlying fabric.

Universities and research labs in the region churn out specialists in high‑speed signaling and AI‑optimized silicon, feeding a pipeline of engineers who can accelerate product development cycles.

Industry consortia are finalizing specifications that ensure cross‑vendor compatibility, reducing integration risk for enterprises adopting express‑link based topologies.

Traditional networking firms are partnering with AI chipset manufacturers, creating joint offerings that bundle switch hardware with optimized firmware for AI workloads.

Europe

European players are leveraging strong policy support for digital sovereignty to nurture local AI compute ecosystems. Governments are offering incentives for building edge‑focused data centers that rely on low‑latency interconnects, positioning express‑link switches as a strategic asset for national AI initiatives. Vendor strategies emphasize open‑source firmware, catering to a market that values transparency and long‑term support contracts. The region’s fragmented regulatory environment, however, requires vendors to navigate divergent certification requirements, a factor that can slow time‑to‑market for newer switch generations. Companies that can adapt software stacks to meet multiple compliance frameworks will gain a decisive foothold.

Asia‑Pacific

Asia‑Pacific’s rapid expansion of AI research hubs is driving a surge in demand for high‑bandwidth interconnect solutions. Nations such as China, Japan, and South Korea are investing heavily in AI‑focused supercomputing clusters where express‑link technology can mitigate bottlenecks between accelerator arrays. Local manufacturers are quick to iterate on silicon designs, often tailoring products to the specific thermal and power constraints of regional data‑center layouts. While price sensitivity remains high, the willingness to adopt cutting‑edge architectures creates a fertile testing ground for innovative switch form factors that balance performance with cost efficiency.

South America

In South America, AI Compute Express Link Switch Market is emerging alongside broader digital transformation efforts. Emerging cloud providers are constructing Tier‑2 data centers that prioritize modularity, allowing them to scale compute resources as AI adoption grows. The region’s relatively lower average data‑center density encourages solutions that maximize throughput per rack, making express‑link switches attractive for both public and private sector projects. Nonetheless, supply‑chain constraints and limited local design expertise pose challenges; partnerships with North American OEMs are becoming a common strategy to bridge these gaps.

Middle East & Africa

The Middle East & Africa are positioning themselves as future AI hubs by investing in sovereign cloud initiatives that require state‑of‑the‑art interconnects. Visionary projects in the United Arab Emirates and Saudi Arabia are building green‑powered AI clusters, where power‑efficient express‑link switches align with sustainability goals. African markets, still in early adoption phases, are focusing on cost‑effective solutions that can be retrofitted into existing infrastructure. For vendors, the key is to offer scalable licensing models and robust remote support, enabling customers to overcome limited on‑site expertise while still extracting performance gains from AI workloads.

Report Scope

This market research report provides a comprehensive analysis of the AI Compute Express Link Switch Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Compute Express Link Switch Market?

-> AI Compute Express Link Switch market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 5.6%

Which key companies operate in AI Compute Express Link Switch Market?

-> Key players include Nvidia Corporation, Intel Corporation, Advanced Micro Devices, Marvell Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for heterogeneous computing workloads, AI training and inference requirements, increased capital spending on next‑generation data centers, and broader adoption of CXL standards.

Which region dominates the market?

-> Regional dominance information is not disclosed in the provided reference.

What are the emerging trends?

-> Emerging trends include adoption of CXL standards, development of modular switch portfolios, and increasing integration of high‑speed interconnects in data‑center architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...