AI Chiplet Interconnect IP Market Insights

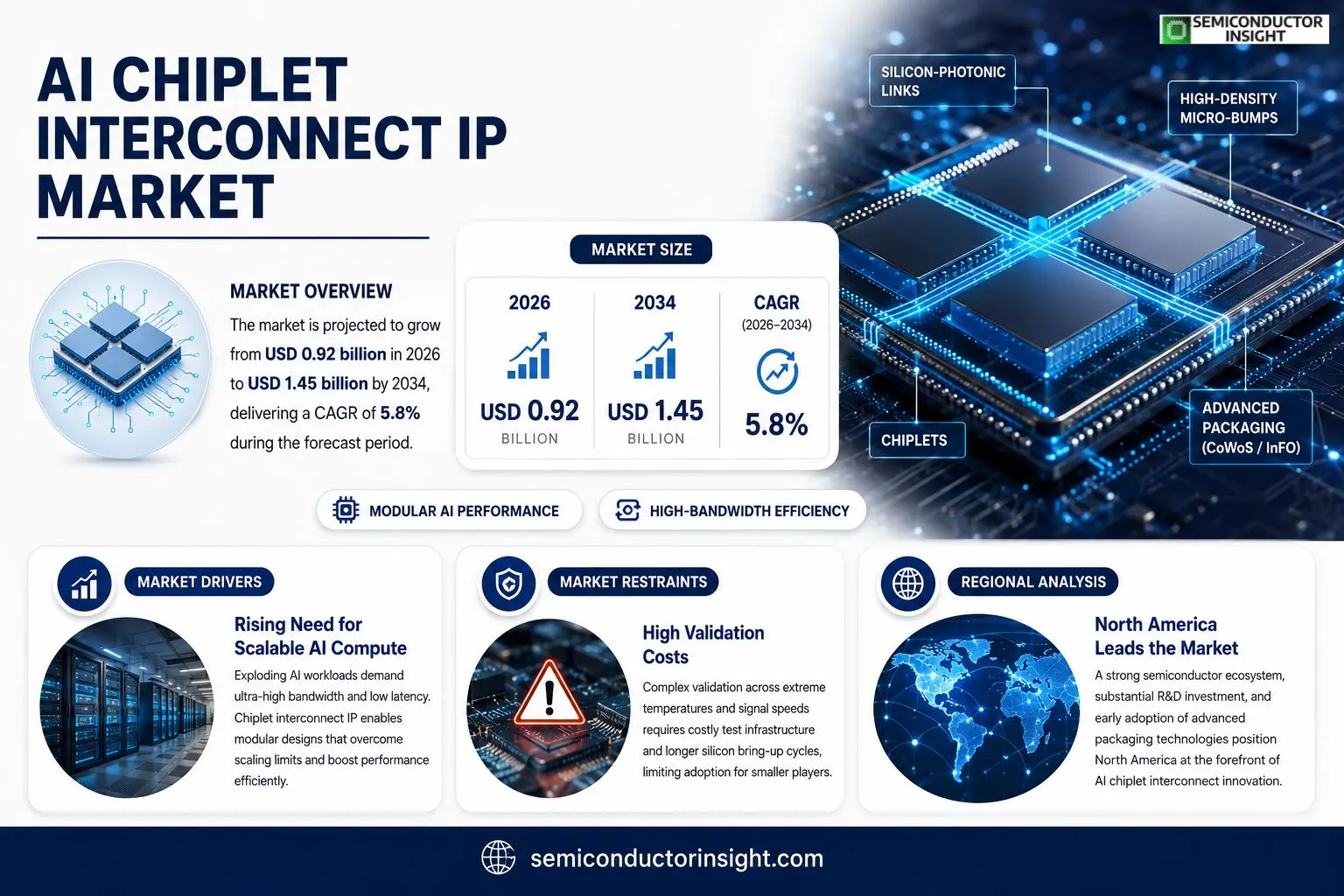

AI Chiplet Interconnect IP market size was valued at USD 0.85 billion in 2025. Forecasts indicate growth from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, delivering a CAGR of approximately 5.8% during the forecast period.

AI chiplet interconnect IP comprises the intellectual property that enables high‑speed communication between heterogeneous chiplets within advanced semiconductor packages. These interfaces support protocols such as silicon‑photonic links, high‑density micro‑bumps, and packaging standards like CoWoS and InFO, allowing designers to assemble compute, memory and specialized accelerators into modular systems.The market is gaining momentum because semiconductor manufacturers are accelerating adoption of chiplet architectures to overcome scaling limits and shorten time‑to‑market. Rising demand for AI workloads in data centers and edge devices pushes vendors toward flexible interconnect solutions that balance bandwidth with power efficiency. Recent collaborations,such as the partnership announced in March 2024 between Company A and Company B on a next‑generation optical interconnect IP,illustrate how key players are expanding their portfolios to capture emerging opportunities.

MARKET DRIVERS

Rising Need for Scalable AI Compute

AI Chiplet Interconnect IP Market is being propelled by enterprise data centers that must accommodate ever‑larger neural networks. As model parameters cross the trillion‑parameter threshold, traditional monolithic dies encounter latency bottlenecks and thermal ceilings. Chiplet‑based interconnect solutions deliver the bandwidth density required to keep inference pipelines fluid, allowing vendors to ship higher‑performance AI accelerators without a proportional increase in silicon area.

Advances in Chiplet Architecture

Recent breakthroughs in silicon‑photonic and high‑speed electrical links have reduced the signal‑integrity penalty that early chiplet designs suffered. These technical refinements translate into lower power per gigabit transferred, a metric that OEMs scrutinize when balancing performance against operational expenses. The resulting efficiency gains make interconnect IP an attractive upgrade path for legacy platforms seeking to retrofit AI capabilities.

➤ Industry analysts note that firms that adopt modular interconnect stacks can accelerate product cycles by up to 30 % compared with redesigning monolithic ASICs.

Collectively, the pressure to sustain AI workloads, coupled with tangible improvements in interconnect reliability, creates a compelling business case for investing in specialized IP blocks. Companies that secure early access to mature interconnect libraries position themselves to capture premium margins as downstream manufacturers race to differentiate their AI offerings.

MARKET CHALLENGES

Design Complexity and Integration Overheads

Engineers must reconcile heterogeneous process technologies, signal‑timing constraints, and thermal budgets within a single package. The necessity to co‑design silicon, substrate, and firmware inflates development timelines, and many smaller fabless players lack the in‑house expertise to manage such multidomain projects efficiently.

Other Challenges

Standardization Gaps

The ecosystem still suffers from fragmented interconnect specifications, which forces customers to negotiate multiple licensing agreements and adapt CAD flows for each vendor’s proprietary format. This heterogeneity hampers economies of scale and introduces supply‑chain uncertainty.

MARKET RESTRAINTS

High Validation Costs

Validating high‑speed interconnects across temperature extremes demands expensive test equipment and prolonged silicon‑bring‑up phases. The upfront capital outlay deters marginal players and consolidates market power among a handful of well‑funded IP providers.Furthermore, the iterative nature of AI accelerator design means that each new model generation may require a fresh validation pass, compounding the financial burden and slowing time‑to‑market for innovative solutions.

MARKET OPPORTUNITIES

Emerging Edge AI Deployments

Edge devices,ranging from autonomous drones to smart cameras,are beginning to host inference engines that rival data‑center performance. These applications demand compact, power‑efficient interconnect IP that can link multiple heterogeneous compute tiles within constrained form factors. Suppliers that tailor modular IP for edge‑centric power envelopes are poised to capture a fast‑growing niche.Geographically, regions such as Southeast Asia are witnessing a surge in localized AI manufacturing hubs, backed by government incentives for advanced semiconductor ecosystems. This policy‑driven momentum opens channels for IP vendors to establish regional design‑service partnerships and secure recurring licensing revenue.Finally, the convergence of AI with emerging paradigms like neuromorphic computing introduces novel bandwidth and latency requirements. Early entrants that extend their interconnect portfolios to support mixed‑signal, ultra‑low‑latency pathways can differentiate themselves and command premium pricing in next‑generation AI architectures.

AI Chiplet Interconnect IP Market Trends

Emergence of Heterogeneous Chiplet Architectures

AI Chiplet Interconnect IP Market recorded a valuation of roughly USD 0.85 billion in 2025 and is forecast to climb to about USD 1.45 billion by 2034. This trajectory reflects a steady shift among semiconductor firms toward modular designs that pair compute, memory and specialized accelerators within a single package. By leveraging silicon‑photonic links, high‑density micro‑bumps and advanced packaging standards such as CoWoS and InFO, the interconnect layer now underpins data‑center and edge workloads that demand both bandwidth and latency discipline. Designers are attracted to the flexibility of chiplet‑based systems because they can integrate best‑in‑class IP without the time‑consuming mask cycles associated with monolithic SoCs. Consequently, the interconnect IP layer has become a decisive factor in achieving performance targets while keeping power envelopes within acceptable limits.

Other Trends

Power‑Efficiency Balancing

In practice, the most pressing engineering challenge lies in reconciling raw throughput with power consumption. Modern AI workloads are sensitive to energy cost, prompting vendors to favor interconnect solutions that incorporate adaptive signaling and low‑swing voltage domains. These techniques allow a single chiplet fabric to scale data rates from a few gigabits per second up to terabit‑per‑second ranges without a proportional increase in thermal load. The resulting power‑per‑bit metric has improved enough to make chiplet‑centric platforms attractive for hyperscale servers, where operational expense is a critical competitive lever.

Strategic Alliances Accelerating IP Adoption

Collaboration has emerged as a catalyst for market momentum. A partnership announced in March 2024 between Company A and Company B introduced a next‑generation optical interconnect IP that merges silicon‑photonic routing with programmable micro‑bump arrays. This joint effort not only broadened each company’s addressable portfolio but also set a benchmark for integration speed and power efficiency that rivals are now racing to match. Similar co‑development initiatives are appearing across the ecosystem, signaling that AI Chiplet Interconnect IP Market is being shaped as much by collective engineering roadmaps as by individual product launches. Enterprises that secure early access to these joint offerings are positioned to differentiate their AI hardware pipelines and to shorten time‑to‑revenue in an increasingly competitive landscape.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive dynamics shaping the AI Chiplet Interconnect IP sector

Intel continues to command the forefront of AI chiplet interconnect IP, leveraging its extensive silicon‑photonic and high‑density micro‑bump libraries that underpin CoWoS and InFO implementations. Complementing Intel’s breadth, AMD’s acquisition of Xilinx has integrated advanced programmable interconnect blocks, enabling designers to stitch together compute, memory and accelerator die with minimal latency. Nvidia, while primarily known for GPU IP, has been extending its proprietary high‑bandwidth interface suite to support heterogeneous chiplet assemblies, targeting data‑center accelerators that demand tight power‑to‑performance trade‑offs. Cadence and Synopsys dominate the EDA‑driven IP supply chain; their design‑for‑test and verification modules reduce time‑to‑market for chiplet‑centric products, and both firms have entered strategic alliances with foundries to co‑develop process‑compatible link specifications. The combined weight of these incumbents shapes a market environment where extensive IP portfolios, proven manufacturing pathways, and deep customer relationships constitute decisive competitive advantages.Beyond the major vendors, a cohort of specialist providers is carving out differentiated positions. Rambus supplies high‑speed memory‑type interconnect IP that emphasizes low power consumption for edge deployments, while Marvell’s aftermarket offerings focus on silicon‑photonic serializers that address bandwidth‑critical workloads. TSMC and Samsung, operating extensive foundry services, are introducing in‑house interconnect blocks that integrate directly with their advanced packaging nodes, thereby bundling IP with process technology. Qualcomm leverages its modem heritage to deliver compact, heterogeneous links suitable for mobile AI accelerators. Broadcom’s Ethernet‑centric IP suite has been adapted for chiplet environments, offering robust scalability for networking equipment. Emerging start‑ups such as Netlist and SiPearl bring novel architectural concepts, including mixed‑signal bridge IP that can bridge legacy CMOS with emerging photonic layers, positioning themselves as potential disruptors as modular designs gain traction.

List of Key AI Chiplet Interconnect IP Companies Profiled

- Intel

- AMD (including Xilinx)

- Nvidia

- Cadence Design Systems

- Synopsys

- Rambus

- Marvell Technology

- TSMC

- Samsung Electronics

- Qualcomm

- Broadcom

- Arm (SoftBank Group)

- Netlist

- SiPearl

- Foundries

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon‑Photonic IP

|

| By Application |

|

Data‑Center Accelerators

|

| By End User |

|

Cloud Service Providers

|

| By Architecture |

|

Hybrid Hierarchical

|

| By Performance Tier |

|

Enterprise‑Grade

|

Regional Analysis: AI Chiplet Interconnect IP Market

North America

Companies in the United States and Canada are integrating high‑bandwidth interconnect IP into AI accelerators to meet the demands of transformer‑based inference. The willingness to experiment with emerging standards such as CXL‑based chiplet links reflects a strategic aim to differentiate product roadmaps.

A dense network of EDA vendors, IP integrators, and academic research labs creates a virtuous cycle. Design houses benefit from open‑source verification suites, while IP developers receive rapid feedback on performance metrics across multiple silicon nodes.

Recent disruptions have prompted a shift toward domestic wafer‑fabrication capacity. This trend reduces lead times for prototype runs and allows AI chiplet interconnect IP firms to negotiate more favorable licensing terms with foundries.

Federal initiatives that fund advanced packaging research indirectly boost demand for interconnect IP, as grant recipients must source compatible licensing solutions to qualify for subsidies.

Europe

European AI chiplet interconnect IP activity clusters around Germany, the Netherlands, and France, where collaborative consortia bridge semiconductor manufacturers with AI start‑ups. Policy frameworks that prioritize sovereign technology capabilities encourage local design houses to embed proprietary interconnect protocols, creating a modest yet distinct niche. The region’s emphasis on energy‑efficient compute drives interest in low‑power interconnect schemes, prompting IP vendors to showcase power‑aware licensing models. While overall market size lags behind North America, the depth of expertise in heterogeneous integration offers a valuable counterbalance to cost‑sensitive deployments in automotive and industrial IoT segments.

Asia‑Pacific

In Asia‑Pacific, Taiwan, South Korea, and Japan dominate fabrication capacity, while China accelerates its own chiplet roadmap through state‑backed programs. The sheer volume of silicon production fuels a high‑velocity demand for interconnect IP that can be adapted across diverse product categories, from consumer electronics to high‑performance computing clusters. However, divergent standards and fragmented IP licensing practices create friction, prompting regional alliances that seek harmonization. Companies that can navigate these complexities stand to capture sizable contracts from OEMs seeking to balance performance with cost constraints.

South America

South American participation remains embryonic, with Brazil and Chile hosting a handful of design service firms that act as intermediaries for multinational chiplet vendors. The primary driver is the desire to localize component sourcing for government‑led AI initiatives that target agriculture and natural‑resource monitoring. Although the market lacks depth, emerging partnerships with North American IP providers suggest a gradual elevation of technical capabilities, especially in low‑latency edge deployments.

Middle East & Africa

The Middle East & Africa region shows a nascent but purposeful interest in AI chiplet interconnect IP, largely driven by sovereign data‑center projects in the United Arab Emirates and research hubs in South Africa. Investment funds are beginning to allocate capital toward startups that specialize in secure interconnect solutions, reflecting a strategic focus on data sovereignty. While the ecosystem is still building, early adopters are leveraging IP licensing arrangements that emphasize flexibility, preparing the ground for future expansion as regional AI workloads intensify.

Report Scope

This market research report provides a comprehensive analysis of the AI Chiplet Interconnect IP Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Chiplet Interconnect IP Market?

-> AI Chiplet Interconnect IP Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034, delivering a CAGR of approximately 5.8% during the forecast period.

Which key companies operate in AI Chiplet Interconnect IP Market?

-> Key players include Company A and Company B, which announced a partnership in March 2024 on next‑generation optical interconnect IP.

What are the key growth drivers?

-> Key growth drivers include accelerated adoption of chiplet architectures by semiconductor manufacturers, rising AI workload demand in data centers and edge devices, and the need for high‑bandwidth, power‑efficient interconnect solutions.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include development of silicon‑photonic links, high‑density micro‑bump technologies, and collaborative projects between major IP providers to create modular, high‑performance chiplet ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...