AI Chiplet Integration Platform Market Insights

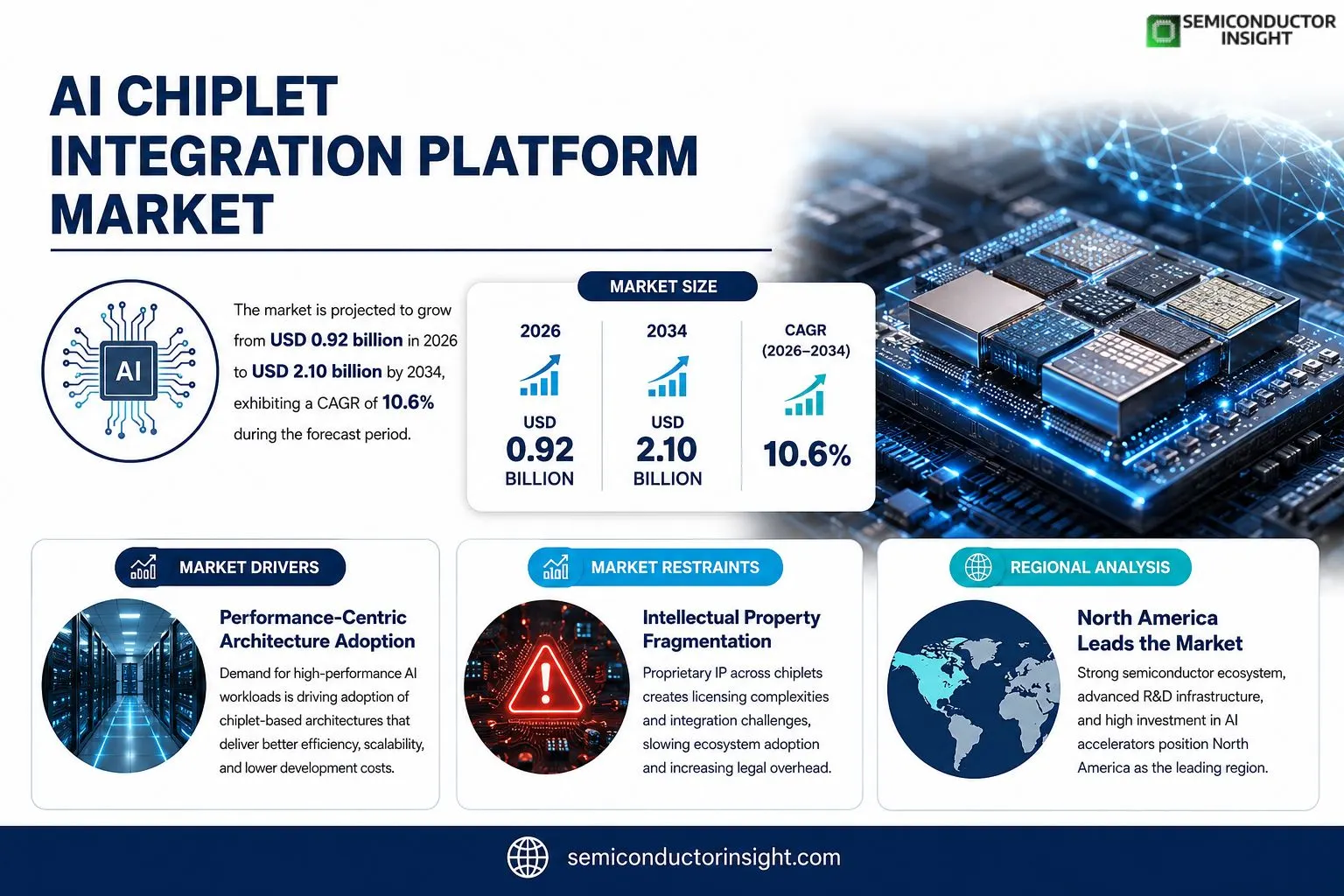

AI Chiplet Integration Platform market size was valued at USD 0.85 billion in 2025. The market is forecasted to expand from USD 0.92 billion in 2026 to USD 2.10 billion by 2034, delivering a CAGR of approximately 10.6 % over the period.

An AI chiplet integration platform consists of hardware interconnects and software toolchains that allow heterogeneous chipletssuch as CPUs, GPUs, memory dies and specialized acceleratorsto be assembled into a single package while keeping latency low and power consumption efficient. The platform manages physical bonding methods (e.g., silicon interposers) together with design‑time verification suites that automate placement, routing and thermal analysis.The sector gains momentum because semiconductor firms seek faster time‑to‑market for customized AI solutions without undertaking full‑die redesigns. Recent collaborations illustrate this shift: Intel announced a partnership with TSMC in March 2024 on advanced packaging for chiplets, while Cadence released an integrated verification suite tailored for heterogeneous integration, both lowering barriers for broader adoption.

MARKET DRIVERS

Performance‑Centric Architecture Adoption

The surge in data‑intensive workloads has compelled semiconductor firms to move beyond monolithic dies. By partitioning compute, memory, and interconnect functions into dedicated chiplets, designers achieve higher performance per watt while keeping die costs manageable. This architectural shift underpins the rapid uptake of AI chiplet integration solutions across hyperscale datacenters.

Standardized Interconnect Ecosystem

Consortia such as OIF and the Open Compute Project have converged on high‑density, low‑latency interconnect standards (e.g., silicon photonics, EMIB). The emergence of a common signaling language reduces integration risk, encouraging OEMs to invest in platform‑level tooling rather than bespoke designs. Consequently, AI Chiplet Integration Platform Market benefits from a growing pool of reusable IP blocks.

➤ “Design cycles have shrunk by roughly 30% for projects that leverage validated chiplet ecosystems.”

These efficiencies translate directly into faster time‑to‑market for AI accelerators. Verticals that demand rapid innovationsuch as autonomous systems and edge inferenceare now able to prototype and scale with a fraction of the capital previously required, fueling sustained platform demand.

MARKET CHALLENGES

Thermal Management Complexity

Integrating multiple heterogeneous chiplets raises hotspot density, especially when high‑bandwidth memory and AI cores are stacked in close proximity. Engineers must balance thermal envelope constraints against performance goals, a trade‑off that can delay design finalization and inflate tooling costs.

Other Challenges

Supply Chain Fragmentation

The reliance on specialized packaging facilities and discrete wafer sources creates a bottleneck for volume production. When a single fab experiences downtime, the downstream assembly line for chiplet platforms can be crippled, jeopardizing delivery schedules.

MARKET RESTRAINTS

Intellectual Property Fragmentation

Each chiplet often carries proprietary IP from different vendors. Negotiating cross‑licensing agreements can be protracted, and the legal overhead may deter smaller players from participating in the ecosystem. This fragmentation slows the consolidation of a truly open platform.

MARKET OPPORTUNITIES

Customization for Edge AI Deployments

Edge devices demand low‑power, high‑efficiency compute that can be tailored to specific inference models. AI Chiplet Integration Platform Market is uniquely positioned to offer modular, application‑specific configurations, enabling OEMs to differentiate products without incurring full‑silicon design costs. This opens a lucrative niche for vendors that can supply vetted chiplet libraries and rapid integration services.

AI Chiplet Integration Platform Market Trends

Accelerating Heterogeneous Integration

AI Chiplet Integration Platform Market is seeing a shift toward broader adoption of heterogeneous packaging as manufacturers prioritize modularity over monolithic die designs. By leveraging silicon interposers and advanced bonding techniques, chiplets can be combined while preserving low‑latency communication and efficient power envelopes. This architectural flexibility enables silicon vendors to respond to rapidly changing AI workload requirements without incurring the cost of full‑chip redesigns. As a result, development cycles contract, and product differentiation accelerates, allowing companies to capture niche segments that demand specialized accelerator mixes. Customers ranging from hyperscale cloud operators to autonomous vehicle developers are beginning to request modular AI accelerators that can be tailored post‑silicon, prompting foundries to incorporate chiplet support into their standard process design kits. This shift is prompting OEMs to reevaluate their supply strategies, favoring vendors that provide validated integration platforms.

Other Trends

Design‑Time Automation Gains Advantage

The integration toolchain is becoming a decisive competitive advantage. Cadence’s recent verification suite automates placement, routing, and thermal profiling across disparate die stacks, reducing manual engineering effort by an estimated 30 percent. Such automation mitigates the risk of signal integrity failures that traditionally plagued multi‑chip assemblies. For design houses, this translates into shorter validation windows and more predictable yield rates, fostering confidence in investing in chiplet‑centric roadmaps. Consequently, smaller fabless players can contemplate complex AI solutions that were previously reserved for large integrated device manufacturers. The reduced manual effort also lowers engineering headcount, enabling organizations to allocate resources toward algorithmic innovation rather than layout optimization. Moreover, the standardized verification flow improves cross‑vendor compatibility, making it feasible for designers to source chiplets from multiple suppliers within a single package. Within AI Chiplet Integration Platform Market, the emergence of automated verification tools marks a turning point for supply‑chain efficiency.

Strategic Partnerships Reduce Entry Barriers

Strategic alliances are reshaping the supply chain, as illustrated by Intel’s March 2024 partnership with TSMC on advanced packaging for chiplet assemblies. The collaboration blends Intel’s architecture expertise with TSMC’s process leadership, shortening the time required to qualify interposer technologies for volume production. This joint effort signals to ecosystem participants that entry barriers are receding, encouraging broader investment in AI‑focused chiplet ecosystems. For vendors, the implication is a clearer path to monetize differentiated AI workloads while sharing development risk, which should accelerate the rollout of next‑generation compute blocks across data‑center and edge segments. In parallel, the joint roadmap established by the partners includes a technology preview program that invites early adopters to co‑develop reference designs, effectively shortening the validation loop for new AI workloads. This collaborative model not only spreads R&D expenses but also creates a de‑facto standard that can be leveraged by downstream system integrators, reinforcing the market’s shift toward modular compute architectures.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Chiplet Integration Platform Market Competitive Overview

Intel remains the de‑facto benchmark for large‑scale chiplet integration, leveraging its extensive IP portfolio and deep ties with advanced‑packaging partners such as TSMC. The company’s silicon‑interposer expertise, combined with an end‑to‑end design‑for‑manufacturing flow, gives it a commanding position in both data‑center and edge AI solutions. Cadence Design Systems complements the hardware side by delivering a verification suite that automates placement, routing, and thermal analysis across heterogeneous die stacks, effectively lowering the engineering effort required for each new AI offering. This dualityfoundry‑level interconnects paired with sophisticated EDA toolscreates a market structure where a handful of integrated hardware‑software providers dominate the high‑volume segment, while niche players negotiate specialized contracts around specific accelerator technologies.Beyond the incumbents, a cluster of firms is carving out distinct niches that enrich the overall ecosystem. AMD (through its Xilinx acquisition) focuses on programmable logic chiplets that accelerate inference pipelines, whereas Qualcomm targets mobile‑centric AI accelerators that must coexist with communication modules. Samsung Electronics and Foundries invest heavily in advanced interposer processes to support memory‑intensive workloads, while Marvell Technology supplies networking‑oriented chiplets that enable distributed AI inference at the edge. Arm Holdings supplies the architectural backbone for many CPU‑based chiplets, and Broadcom contributes high‑speed I/O fabrics. Applied Materials and ASE Technology Holding provide critical packaging and testing services that ensure yield and reliability in large‑scale production. Collectively, these companies diversify the supply chain, offering customers a menu of integration options tailored to performance, power, and cost constraints.

List of Key AI Chiplet Integration Platform Companies Profiled

- Intel Corporation

- Cadence Design Systems

- Advanced Micro Devices (AMD) – includes Xilinx

- Qualcomm Incorporated

- Samsung Electronics Co., Ltd.

- Foundries Inc.

- Marvell Technology Group Ltd.

- Arm Holdings

- Broadcom Inc.

- Applied Materials, Inc.

- ASE Technology Holding Co., Ltd.

- Synopsys, Inc.

- Taiwan Semiconductor Manufacturing Company (TSMC)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Heterogeneous Integration

|

| By Application |

|

Data Center Accelerators

|

| By End User |

|

System Integrators

|

| By Integration Approach |

|

2.5D Interposer

|

| By Solution Ecosystem |

|

Full‑stack verification suites

|

Regional Analysis: AI Chiplet Integration Platform Market

North America

Silicon Valley labs, Toronto research hubs, and Boston’s AI centers funnel skilled engineers into chiplet ecosystems, feeding platform developers with innovative design practices and rapid prototyping capabilities.

Venture firms specialize in early‑stage AI silicon projects, offering not only financing but also strategic guidance that aligns integration platforms with emerging market niches.

Proximity to leading fabs in Arizona and Texas enables rapid iteration cycles, allowing platform providers to test and qualify modules under real‑world production conditions.

Recent incentives for domestic chip production coupled with export‑control guidelines push firms toward modular designs that can be re‑configured without breaching compliance thresholds.

Europe

European initiatives such as the European Chips Act have galvanized cross‑border collaboration, encouraging platform vendors to adopt standards that ease integration across diverse foundries. Engineers in Germany and France are emphasizing power‑efficient AI chiplets to meet the continent’s sustainability goals, prompting providers to embed adaptive power‑management modules. The region’s fragmented market, however, demands flexible licensing models that can accommodate a variety of industrial customers, from automotive OEMs to telecom operators. Platform players that tailor their offerings to these regulatory and environmental nuances will capture growth across the EU’s heterogeneous landscape.

Asia‑Pacific

The Asia‑Pacific cluster, led by China, Taiwan, and South Korea, is distinguished by massive production capacity and aggressive cost targets. Manufacturers are leveraging chiplet integration to achieve economies of scale while preserving performance differentiation for AI accelerators. Yet, geopolitical tensions introduce supply‑chain uncertainty, motivating platform developers to design interfaces that can seamlessly switch between domestic and overseas fab services. The region’s rapid adoption of edge AI in smart cities also fuels demand for modular solutions that can be deployed at scale with minimal redesign effort.

South America

South America remains a nascent arena for AI chiplet platforms, with Brazil’s emerging semiconductor ecosystem offering early‑stage opportunities. Local startups are focusing on niche applications such as agricultural AI and mining analytics, requiring compact, low‑power chiplet configurations. Partnerships with North American design houses are helping bridge technology gaps, but limited domestic fabrication means platform providers must emphasize robust testing and validation frameworks that mitigate latency in overseas production cycles.

Middle East & Africa

In the Middle East & Africa, interest in AI chiplet integration is driven by sovereign wealth funds investing in digital infrastructure and by defense contractors seeking customized compute blocks. The United Arab Emirates and Saudi Arabia are establishing pilot fabs that demand platforms able to support rapid technology transfer. Meanwhile, Africa’s growing mobile broadband footprint creates a modest market for energy‑efficient AI modules. Vendors that can offer turnkey integration kits with localized support stand to gain footholds in these developing markets.

Report Scope

This market research report provides a comprehensive analysis of the AI Chiplet Integration Platform Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Chiplet Integration Platform Market?

-> AI Chiplet Integration Platform Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 2.10 billion by 2034, growing at a CAGR of 10.6 % over the forecast period.

Which key companies operate in AI Chiplet Integration Platform Market?

-> Key players include Intel, TSMC, Cadence, and other semiconductor and EDA firms, among others.

What are the key growth drivers?

-> Key growth drivers include accelerated time‑to‑market for AI solutions, demand for heterogeneous integration, and strategic collaborations that lower packaging barriers.

Which region dominates the market?

-> North America leads in market share due to a mature semiconductor ecosystem, while Asia‑Pacific shows rapid growth.

What are the emerging trends?

-> Emerging trends include advanced silicon interposers, AI‑driven design automation, and modular chiplet ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...