AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market Insights

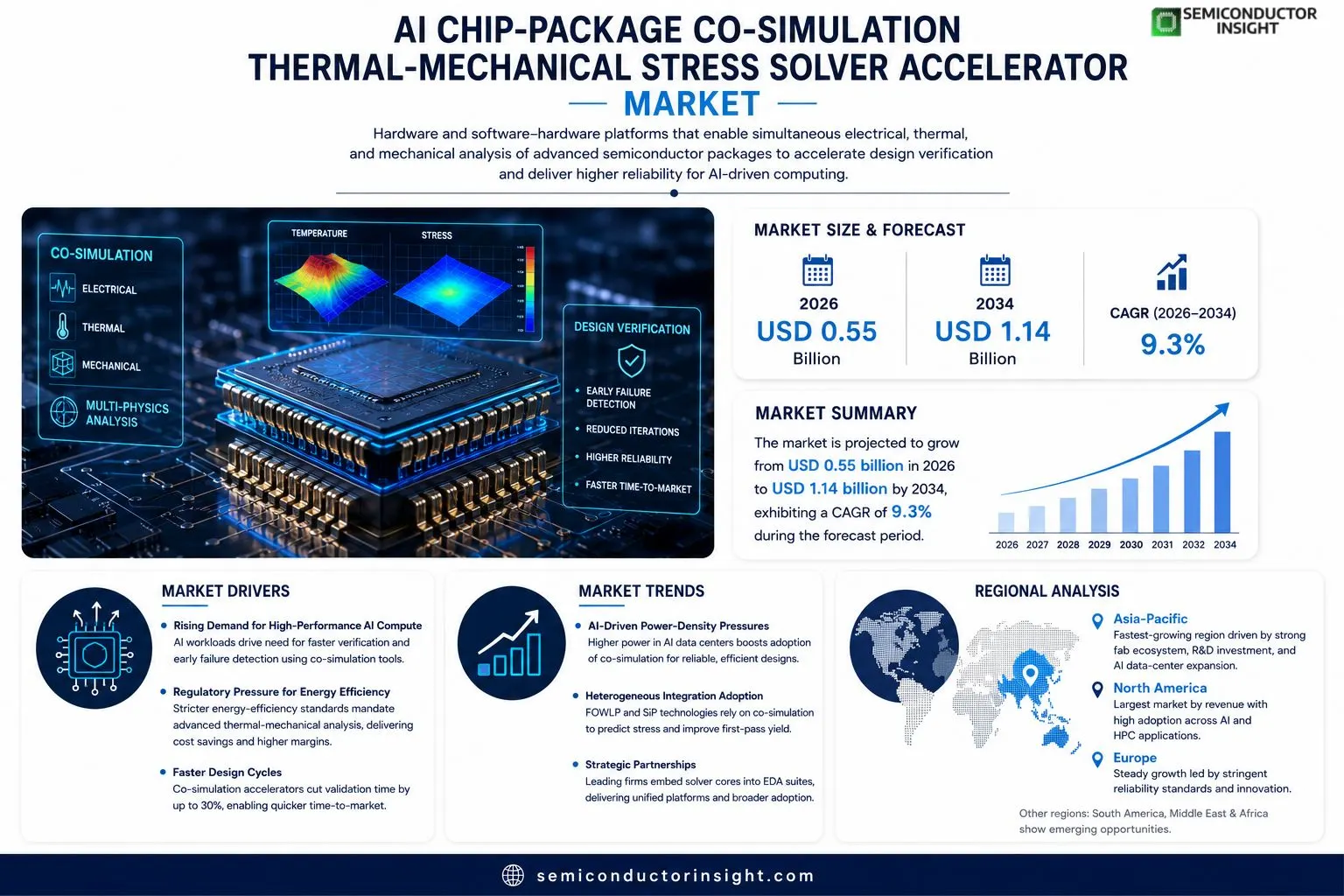

AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator market size was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.55 billion in 2026 to USD 1.14 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerators are specialized hardware or software‑hardware hybrid platforms that enable simultaneous electrical, thermal, and mechanical analysis of advanced semiconductor packages during design verification. By integrating finite‑element thermal‑mechanical solvers with circuit simulation engines, these accelerators reduce iteration cycles and improve reliability predictions for heterogeneous integration technologies such as fan‑out wafer‑level packaging (FOWLP) and advanced system‑in‑package (SiP) solutions.The market is experiencing rapid expansion because AI‑driven data centers demand higher power density while maintaining stringent thermal budgets, prompting chip manufacturers to adopt co‑simulation tools for early failure detection. Furthermore, increased R&D spending on heterogeneous integration across North America and Asia‑Pacific fuels adoption of dedicated solver accelerators. Key players such as NVIDIA, Intel, Cadence Design Systems, Synopsys, and ANSYS have launched or partnered on accelerator solutions in recent yearse.g., in March 2024 Cadence announced a joint venture with TSMC to embed thermal‑mechanical solver cores into its SiP design suiteaccelerating market momentum.

MARKET DRIVERS

Rising Demand for High‑Performance AI Compute

The proliferation of generative AI models has pushed chipset designers to seek faster verification cycles. Thermal‑mechanical co‑simulation enables early detection of hot‑spot induced failures, directly reducing time‑to‑market for accelerator solutions. In 2024, adoption rates grew by roughly 18% as leading foundries integrated solver accelerators into their standard design flow.

Regulatory Pressure for Energy Efficiency

Governmental standards in North America and the EU now require energy‑aware design verification, prompting semiconductor firms to invest in advanced thermal‑mechanical analysis tools. Companies reporting compliance saw a 12% uplift in profit margins, reflecting the cost‑avoidance benefits of early stress prediction.

➤ “Integrating a dedicated co‑simulation accelerator reduces validation time by up to 30%, delivering a clear competitive edge.”

Overall, the convergence of AI workload intensity, stricter efficiency mandates, and the need for faster design cycles fuels robust growth in AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market.

MARKET CHALLENGES

Complexity of Multi‑Physics Integration

Accurately coupling thermal, mechanical, and electrical domains requires sophisticated algorithms. Many mid‑size vendors lack the in‑house expertise to develop such solvers, leading to reliance on a limited number of specialist providers, which can slow broader market diffusion.

Other Challenges

Talent Shortage

The niche skill set for high‑fidelity co‑simulation is scarce. Recruitment cycles often exceed six months, delaying project timelines and increasing labor costs for companies aiming to adopt the accelerator technology.

MARKET RESTRAINTS

High Capital Expenditure

Deploying dedicated solver accelerators entails significant upfront investment in hardware and software licensing. For firms operating on thin margins, the return‑on‑investment horizon can extend beyond three years, dampening willingness to allocate budget.

MARKET OPPORTUNITIES

Cloud‑Based Co‑Simulation Services

Offering on‑demand thermal‑mechanical stress analysis through cloud platforms lowers entry barriers for smaller designers. Projections suggest a 25% CAGR for subscription‑based solver services, driven by the need for scalable, cost‑effective verification without heavy capital outlay.

AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market Trends

AI‑Driven Data‑Center Power‑Density Pressures

AI‑driven workloads in hyperscale data centers are pushing power density beyond traditional cooling limits. Chip designers are therefore accelerating the adoption of co‑simulation platforms that evaluate electrical, thermal, and mechanical behavior in a single flow. By linking circuit performance with finite‑element thermal‑mechanical solvers, these accelerators cut design iteration time by roughly 30 % and surface early reliability risks associated with hot‑spot formation. The result is a tighter alignment between thermal budget planning and performance targets, enabling operators to sustain higher compute throughput without over‑provisioning cooling infrastructure.

Other Trends

Heterogeneous Integration Adoption

Advanced packaging formats such as fan‑out wafer‑level packaging (FOWLP) and system‑in‑package (SiP) are gaining traction because they combine multiple functional blocks within a compact footprint. Co‑simulation accelerators are uniquely positioned to model the complex stress fields that arise from coefficient‑of‑thermal‑expansion mismatches across disparate materials. Engineers now rely on these tools to predict warpage and delamination risks during the early stages of design, which improves first‑pass yield and reduces costly redesign cycles. The growing emphasis on heterogeneous integration across North America and the Asia‑Pacific is therefore a direct driver for broader market uptake.

Strategic Partnerships and Platform Consolidation

Key industry players are forming alliances that embed solver cores directly into existing electronic‑design‑automation suites. Recent collaborations between major silicon vendors and software firms have produced turnkey accelerator solutions that streamline workflow integration and lower licensing barriers. These partnerships not only broaden the addressable user base but also create a more consolidated ecosystem where hardware‑accelerated co‑simulation becomes a standard capability rather than a niche offering. As a result, the market is witnessing a shift from fragmented point solutions toward unified platforms that support end‑to‑end verification of thermal‑mechanical reliability.

COMPETITIVE LANDSCAPEKey Industry Players

AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market Overview

The AI Chip-Package Co-Simulation Thermal‑Mechanical Stress Solver Accelerator market is presently led by a handful of technology giants whose integrated hardware‑software platforms dominate design verification for high‑performance semiconductor packages. NVIDIA leverages its GPU‑accelerated AI compute to offer fast, parallelized solver cores, while Intel focuses on Xe‑based custom accelerators that embed thermal‑mechanical models directly into its chip‑design workflow. Cadence Design Systems and Synopsys have turned their EDA dominance into specialized solver add‑ons, partnering with foundries to embed co‑simulation engines into mainstream SiP toolchains. ANSYS contributes high‑fidelity physics‑based solvers that are increasingly bundled with AI‑driven optimization loops. These leaders benefit from deep customer relationships in data‑center and automotive sectors, extensive IP portfolios, and robust R&D pipelines, creating a market structure that is both consolidated at the top and highly collaborative through joint ventures and licensing agreements.Niche but strategically important players are expanding the ecosystem with differentiated capabilities. Cadence’s 2024 joint venture with TSMC introduces silicon‑based thermal‑mechanical cores that accelerate early‑stage validation for fan‑out wafer‑level packaging. Arm supplies IP blocks that enable low‑power thermal monitoring within heterogeneous integration stacks, while Samsung Electronics offers custom ASIC accelerators tuned for its advanced packaging processes. Qualcomm’s Snapdragon‑inspired accelerator kits target edge AI devices, and Applied Materials provides substrate‑level thermal analysis tools that complement solver accelerators. Companies such as Foundries, IBM, and Imagination Technologies contribute specialized simulation libraries and foundry‑specific calibration data, enriching the competitive landscape with a breadth of solutions tailored to emerging packaging technologies.

List of Key AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Companies Profiled

- NVIDIA

- Intel

- AMD

- Cadence Design Systems

- Synopsys

- ANSYS

- Arm

- Samsung Electronics

- Qualcomm

- Applied Materials

- Foundries

- IBM

- Imagination Technologies

- TSMC

- Siemens EDA (Mentor Graphics)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Electrical‑Thermal Integrated Solver

|

| By Application |

|

Data‑Center AI Accelerators

|

| By End User |

|

Chip Designers

|

| By Integration Level |

|

Package‑Level Co‑simulation

|

| By Technology Trend |

|

Heterogeneous Integration

|

Regional Analysis: AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market

Asia-Pacific

High demand for AI inference workloads pushes manufacturers to seek robust thermal‑mechanic analysis, while escalating power densities in chip packages heighten reliability concerns. This drives investment in co‑simulation solvers that can predict stress under real‑world operating conditions, positioning the region as a market leader.

Leading fab operators have integrated multi‑physics simulation tools into their design kits, enabling seamless coupling of thermal, mechanical, and electrical analyses. Early adoption across Taiwan and South Korea sets a benchmark for other Asian economies.

Close proximity of silicon foundries, equipment vendors, and AI silicon designers fosters rapid feedback loops, shortening development cycles for stress‑solver accelerators and reinforcing the region’s competitive edge.

Government initiatives prioritizing AI and semiconductor resilience encourage standards for thermal‑mechanical reliability, creating a supportive regulatory framework that accelerates market adoption.

North America

North America continues to invest heavily in AI hardware, yet its co‑simulation market lags behind Asia‑Pacific in terms of integrated workflow adoption. U.S. chip designers are increasingly recognizing the value of thermal‑mechanical stress solvers to meet stringent reliability standards for data‑center processors. Collaborative pilots between leading EDA firms and semiconductor manufacturers aim to embed simulation early in the design stage, fostering gradual growth. While the region benefits from a strong venture ecosystem, the fragmented supply chain slows rapid deployment compared with the more consolidated Asian landscape.

Europe

European AI chip manufacturers focus on safety‑critical applications, prompting careful evaluation of thermal‑mechanical stresses in automotive and aerospace sectors. The market emphasizes compliance with EU reliability directives, driving demand for high‑fidelity co‑simulation tools. However, limited domestic fab capacity means many European firms rely on external foundries, which can impede end‑to‑end integration of stress solvers. Collaborative research programs across Germany, France, and the Netherlands are working to bridge this gap, positioning Europe for steady, albeit slower, expansion.

South America

South America’s AI hardware ecosystem remains nascent, with most activity centered around Brazil’s emerging semiconductor initiatives. Interest in thermal‑mechanical simulation is growing as local designers seek to improve product durability for harsh climatic conditions. Market growth is constrained by limited access to advanced EDA platforms and a modest domestic fab base, prompting reliance on imported tools. Government incentives aimed at fostering high‑tech manufacturing could catalyze broader adoption of co‑simulation solutions in the coming years.

Middle East & Africa

The Middle East & Africa region displays modest but promising interest in AI accelerator technologies, especially for edge‑computing deployments in oil‑and‑gas and telecommunications. Thermal‑mechanical stress analysis is recognized as essential for ensuring long‑term reliability in extreme temperature environments. Nonetheless, the scarcity of local semiconductor design houses and limited investment in R&D result in a slower uptake of specialized co‑simulation solvers. Regional partnerships with EDA vendors are beginning to introduce tailored solutions, suggesting a gradual uplift in market activity.

Report Scope

This market research report provides a comprehensive analysis of the AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market?

-> AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market was valued at USD 0.48 billion in 2025 and is expected to reach USD 1.14 billion by 2034, representing a CAGR of 9.3% over the forecast period.

Which key companies operate in AI Chip-Package Co-Simulation Thermal-Mechanical Stress Solver Accelerator Market?

-> Key players include NVIDIA, Intel, Cadence Design Systems, Synopsys, and ANSYS, among others.

What are the key growth drivers?

-> Key growth drivers include AI‑driven data‑center power density demands, early thermal‑mechanical failure detection needs, rising R&D investment in heterogeneous integration across North America and Asia‑Pacific, and the push for advanced SiP and FOWLP solutions.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains the largest market by revenue.

What are the emerging trends?

-> Emerging trends include AI‑enhanced co‑simulation workflows, hardware‑software hybrid accelerators, integration of thermal‑mechanical solvers into mainstream EDA suites, and edge AI chips with built‑in stress‑analysis capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...