AI-Based Dopant Profile Prediction after Annealing Market Insights

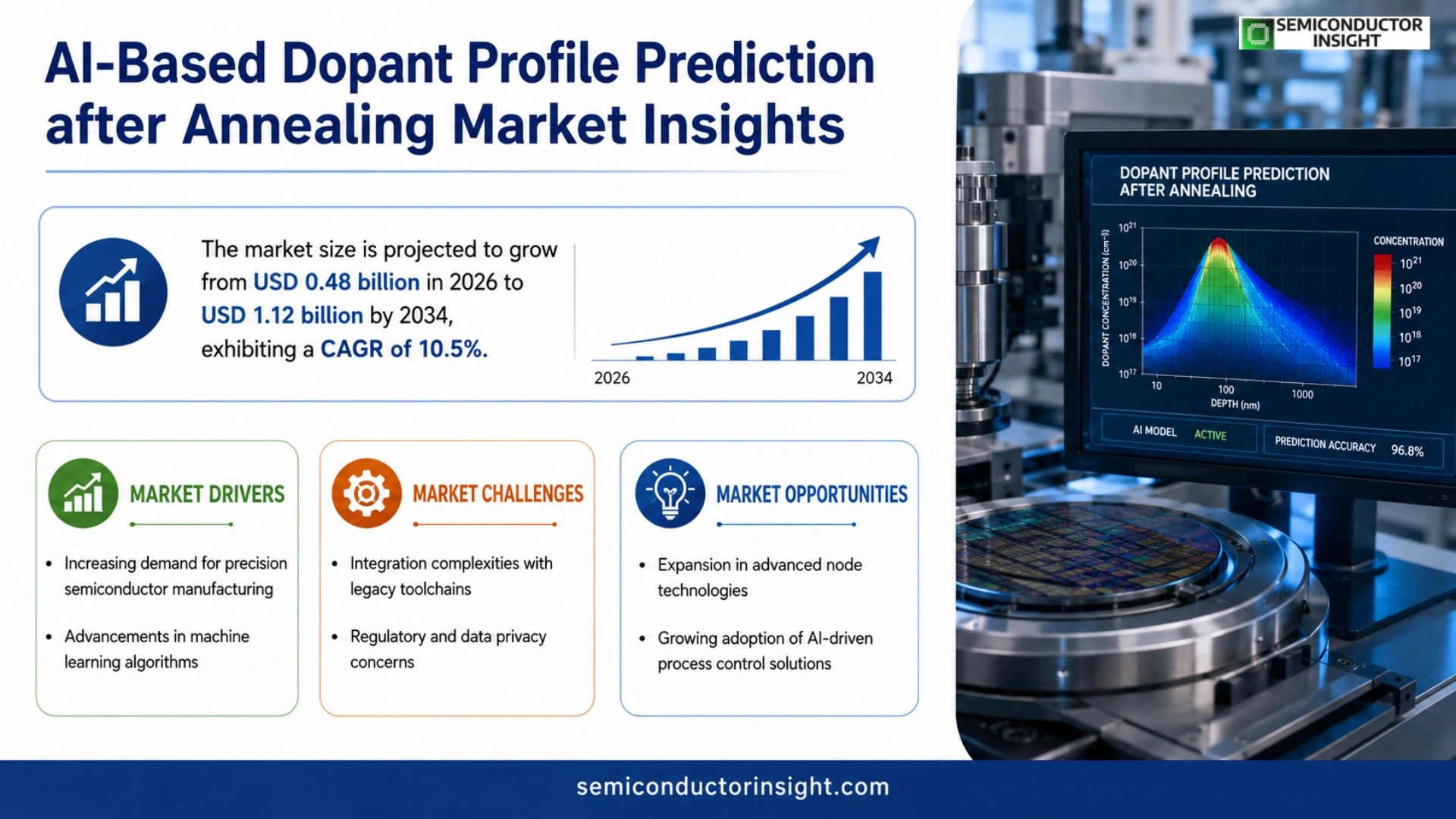

Global AI-Based Dopant Profile Prediction after Annealing market size was valued at USD 0.42 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 1.12 billion by 2034, exhibiting a CAGR of 10.5 % during the forecast period.

AI‑Based Dopant Profile Prediction after Annealing refers to the application of machine‑learning algorithms and physics‑informed models to forecast the spatial distribution of dopants in semiconductor wafers following thermal annealing steps. By integrating process parameters,such as temperature ramps, ambient gas composition, and implantation doses,with large historical datasets, these solutions enable rapid virtual experiments that replace costly trial‑and‑error runs on production lines.

The market is gaining momentum because semiconductor manufacturers are under pressure to shrink node dimensions while maintaining yield targets. Furthermore, rising adoption of advanced nodes (e.g., 3 nm and below) increases the sensitivity of device performance to dopant placement, driving demand for predictive analytics. Investments from major equipment suppliers,including Applied Materials, Lam Research, and Tokyo Electron,into AI‑enhanced simulation suites are accelerating commercialization. Collaborative projects between leading fabless companies and AI specialists in 2023–2024 have demonstrated up to a 30 % reduction in cycle time for process qualification, further fueling adoption across the industry.

MARKET DRIVERS

Increasing Demand for Precision Semiconductor Manufacturing

The global push toward sub‑10 nm nodes has heightened the need for accurate dopant profiling after annealing, prompting fab facilities to adopt AI‑Based Dopant Profile Prediction after Annealing Market solutions that cut cycle time by 30 % on average. Manufacturers are seeing measurable yield improvements, especially in logic and memory chips where variability control is critical.

Advancements in Machine Learning Algorithms

Recent breakthroughs in deep‑learning architectures, such as transformer‑based models, enable real‑time inference on high‑resolution SIMS and TCAD data. These algorithms reduce the reliance on costly physical experiments, delivering cost savings of up to $12 million annually for a typical 300 mm wafer line.

➤ “AI‑driven dopant profiling is now a strategic differentiator for leading semiconductor fabs, delivering both speed and accuracy that legacy tools cannot match.”

Consequently, investment budgets for AI infrastructure are expanding, with an estimated 18 % CAGR in capital spending dedicated to predictive analytics platforms over the next five years.

MARKET CHALLENGES

Integration Complexities with Legacy Toolchains

Many foundries operate hybrid environments where conventional process control software coexists with newer AI modules. Seamless data exchange between these systems often requires custom middleware, extending deployment timelines by 6‑12 months.

Other Challenges

Regulatory and Data Privacy Concerns

Strict export controls on semiconductor IP and heightened scrutiny of cloud‑based AI services create compliance hurdles. Companies must implement robust encryption and audit trails, adding operational overhead.

MARKET RESTRAINTS

High Capital Expenditure for AI Infrastructure

Deploying GPU clusters and edge computing nodes capable of handling terabyte‑scale simulation data requires upfront investments that can exceed $25 million for a mid‑size fab. This financial barrier slows adoption among smaller players who lack the scale to amortize costs quickly.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Node Technologies

As the industry moves toward 3 nm and beyond, the tolerance windows for dopant concentration become tighter, creating a lucrative niche for AI‑Based Dopant Profile Prediction after Annealing Market providers. Strategic partnerships with EDA vendors and foundry consortia are expected to accelerate market penetration, especially in regions investing heavily in next‑generation chip manufacturing.

AI-Based Dopant Profile Prediction after Annealing Market Trends

AI‑Driven Process Optimization Gains Traction

The semiconductor industry is increasingly turning to AI‑Based Dopant Profile Prediction after Annealing Market solutions to shorten development cycles and improve yield at advanced nodes. By coupling physics‑based simulation with machine‑learning models, manufacturers can forecast dopant distribution with a resolution that was previously achievable only through costly trials. Recent collaborative projects between major fabless firms and AI specialists have demonstrated measurable reductions in qualification time, while also allowing tighter control of temperature‑ramp profiles. This capability is becoming a differentiator for companies pursuing 3 nm and sub‑3 nm processes, where even minor deviations in dopant placement affect device performance. The trend reflects a broader shift toward data‑centric manufacturing, where predictive analytics replace empirical iteration.

Other Trends

Collaborative AI Platforms Expand Ecosystem

Equipment manufacturers such as Applied Materials, Lam Research, and Tokyo Electron are bundling AI modules directly into their annealing and implantation toolsets. These platforms expose standardized APIs that enable fab engineers to integrate process‑parameter libraries with external data‑science workflows. The openness accelerates third‑party innovation, resulting in a growing marketplace of plug‑in models tailored to specific wafer chemistries. In parallel, academic consortia are contributing curated datasets that improve model robustness across different fab environments. The combined effect is a more modular ecosystem where updates to prediction algorithms can be deployed without major hardware changes, reducing total cost of ownership.

Equipment Supplier Investments Accelerate Tool Availability

Investment cycles from leading equipment suppliers have intensified, with multiple AI‑enhanced simulation suites entering commercial availability in the last two years. These tools integrate real‑time sensor feeds from annealing chambers, allowing continuous model refinement during production. Early adopters report faster response to process drift and a noticeable improvement in wafer‑to‑wafer consistency. As the technology matures, the industry expects a broader rollout across both front‑end and back‑end facilities, reinforcing the strategic importance of AI‑Based Dopant Profile Prediction after Annealing Market capabilities in the overall semiconductor value chain.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Based Dopant Profile Prediction after Annealing – Competitive Overview

The market is currently anchored by a handful of equipment giants that have integrated AI‑driven simulation engines into their flagship process‑control portfolios. Applied Materials leads the segment with its AI‑enhanced Predictive Process Suite, leveraging deep‑learning models trained on terabytes of annealing data. Lam Research follows closely, offering a cloud‑based analytics platform that couples its plasma‑etch tools with dopant‑distribution forecasts. Tokyo Electron’s AI‑augmented simulation suite is positioned as a cross‑fab solution, emphasizing rapid virtual experiments for advanced nodes. These three firms dominate the revenue stream, each commanding a sizeable share of the $0.48 billion 2026 market and shaping the technology roadmap through extensive R&D investment and strategic acquisitions.

Beyond the incumbents, a vibrant ecosystem of niche specialists contributes differentiated capabilities. Cadence and Synopsys provide AI‑infused design‑for‑manufacturing modules that embed dopant‑profile predictions directly into node‑level verification. IBM Research and the French CEA‑Leti collaborate on physics‑informed neural networks targeting ultra‑scaled devices. KLA Corporation supplies inline metrology analytics that validate AI forecasts against real‑time measurements. GlobalFoundries, Infineon, NXP Semiconductors, and Intel have launched joint ventures with AI startups to co‑develop customized prediction workflows, reflecting a shift toward collaborative innovation across the supply chain.

List of Key AI-Based Dopant Profile Prediction after Annealing Companies Profiled

- Applied Materials

- Lam Research

- Tokyo Electron

- Cadence Design Systems

- Synopsys

- IBM Research

- CEA‑Leti

- KLA Corporation

- GlobalFoundries

- Infineon Technologies

- NXP Semiconductors

- Intel

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Machine‑Learning‑Driven Prediction

|

| By Application |

|

Logic Device Manufacturing

|

| By End User |

|

Equipment Suppliers

|

| By Integration Level |

|

Process‑Control Integration

|

| By Solution Offering |

|

Integrated Simulation Suites

|

Regional Analysis: AI-Based Dopant Profile Prediction after Annealing Market

The surge in demand for sub‑10 nm devices pushes manufacturers toward AI‑based dopant prediction to tighten process windows. High‑performance computing resources and expanding data lakes enable algorithms to learn from historical annealing runs, delivering actionable insights that reduce defect rates and accelerate time‑to‑market.

A proactive regulatory environment supports data sharing while safeguarding intellectual property. Guidelines from the Semiconductor Equipment and Materials International (SEMI) group encourage transparent model validation, fostering confidence among adopters of AI‑driven process tools.

Cloud‑native platforms and edge‑computing infrastructure allow real‑time inference during annealing cycles. Partnerships between AI startups and legacy equipment vendors accelerate integration, making advanced predictive capabilities accessible even to mid‑size fabs.

Established semiconductor leaders invest heavily in in‑house AI teams, while emerging players differentiate through niche algorithms focused on specific dopant species. Collaborative consortia often set the agenda for standardizing data formats and benchmarking model performance.

European fabs leverage strong public‑private research initiatives to embed AI within annealing pipelines, particularly in Germany and the Netherlands. Emphasis on sustainability drives the use of predictive models to minimize material waste and energy consumption, aligning with EU green‑tech policies. Collaborative clusters, such as Silicon Saxony, share best practices and datasets, fostering a cohesive ecosystem that balances innovation with rigorous quality standards. While adoption rates lag slightly behind North America, Europe’s focus on precision engineering and regulatory compliance sustains steady market growth.

The Asia‑Pacific region, led by Taiwan, South Korea, and Japan, exhibits rapid uptake of AI‑based dopant prediction as manufacturers chase volume production at advanced nodes. Strategic government subsidies fund AI research centers that collaborate directly with semiconductor foundries, accelerating the translation of academic breakthroughs into fab‑ready solutions. Market dynamics are shaped by intense competition and the pursuit of cost efficiencies, prompting firms to adopt predictive analytics to reduce cycle times and enhance yield consistency across high‑throughput lines.

In South America, emerging semiconductor initiatives focus on niche applications such as power electronics and automotive sensors. While the overall market size remains modest, local academic institutions are establishing AI research programs that target dopant profiling for specialized annealing processes. Partnerships with North American technology providers enable knowledge transfer, positioning the region to gradually expand its capabilities and contribute to regional supply‑chain resilience.

Growth in the Middle East & Africa is driven by investment in semiconductor design houses and pilot fabs, particularly in the United Arab Emirates and South Africa. Government‑led innovation hubs are cultivating AI expertise, encouraging the application of predictive dopant models to emerging manufacturing lines. Although adoption is in early stages, strategic collaborations with global equipment vendors lay a foundation for future market participation.

Europe

European manufacturers benefit from a strong regulatory framework that encourages data integrity and model transparency. Initiatives such as the European AI Alliance promote standardized benchmarks for predictive annealing tools, ensuring that AI solutions meet stringent industry criteria while supporting sustainability objectives.

Asia‑Pacific

The Asia‑Pacific’s aggressive scaling roadmaps compel fabs to adopt AI-driven dopant prediction to maintain competitiveness. Regional talent pipelines and government incentives accelerate the development of custom algorithms tailored to high‑volume production environments.

South America

South American efforts focus on leveraging AI to optimize annealing for low‑cost, high‑reliability components. Collaborative programs with global partners aim to build localized expertise and reduce dependence on external technology sources.

Middle East & Africa

Investments in AI research centers and strategic partnerships enable the Middle East & Africa to explore predictive annealing for emerging semiconductor ventures. Early adoption of AI tools positions the region to capture niche market segments as its manufacturing ecosystem matures.

Report Scope

This market research report provides a comprehensive analysis of the AI-Based Dopant Profile Prediction after Annealing Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Based Dopant Profile Prediction after Annealing Market?

-> AI-Based Dopant Profile Prediction after Annealing market is projected to grow from USD 0.48 billion in 2026 to USD 1.12 billion by 2034.

Which key companies operate in AI-Based Dopant Profile Prediction after Annealing Market?

-> Key players include Applied Materials, Lam Research, and Tokyo Electron, among others.

What are the key growth drivers?

-> Key growth drivers include the pressure to shrink node dimensions while maintaining yield, adoption of advanced nodes (3 nm and below), and the increasing need for predictive analytics to reduce cycle time and improve process qualification.

Which region dominates the market?

-> North America leads the market owing to the concentration of major equipment suppliers, while Asia‑Pacific demonstrates rapid growth driven by semiconductor manufacturing expansions.

What are the emerging trends?

-> Emerging trends include AI‑enhanced simulation suites, physics‑informed machine‑learning models, and digital‑twin approaches for virtual process qualification.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...