AI Adaptive Headlight Beam Control MCU Market Insights

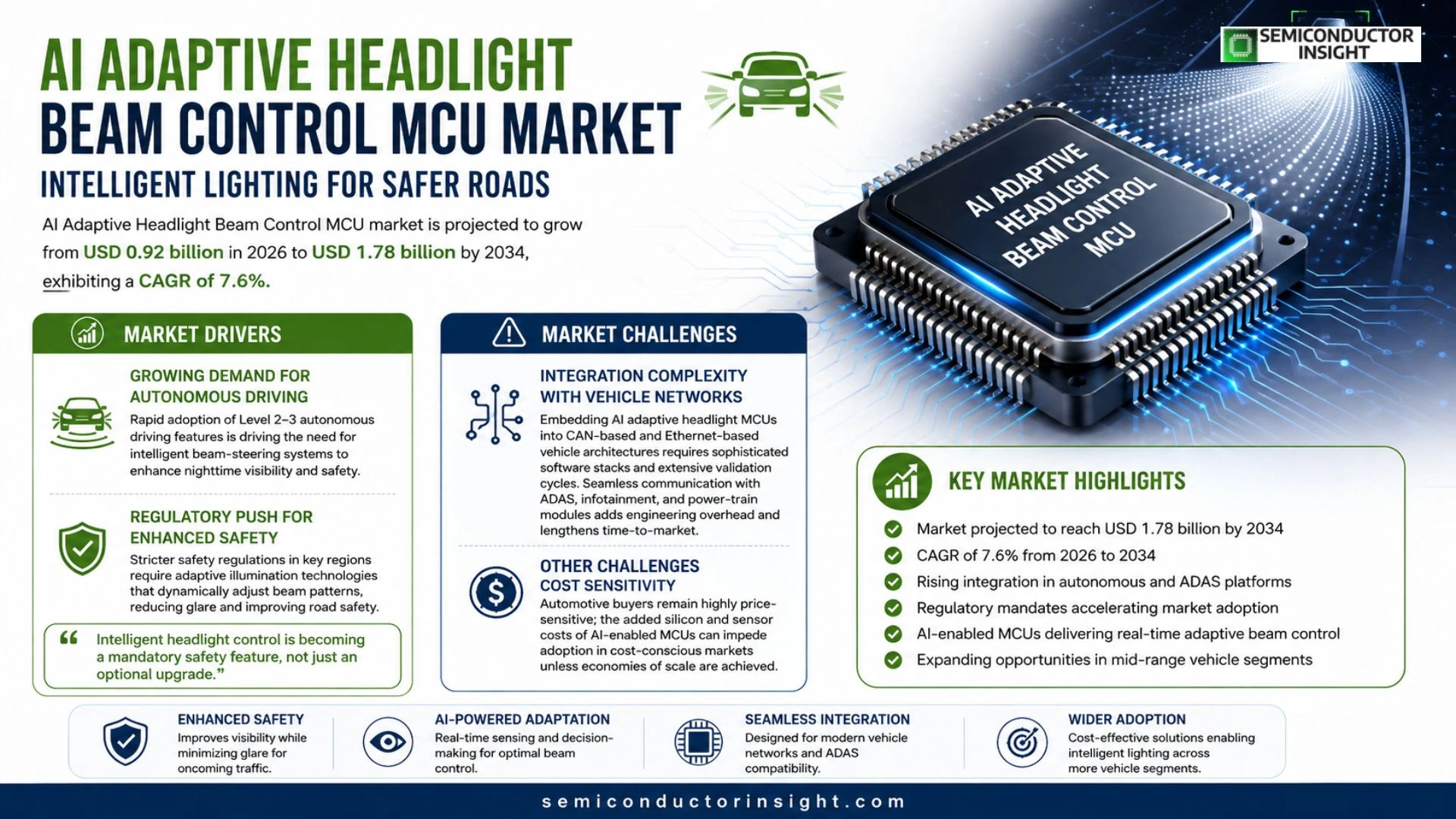

Global AI Adaptive Headlight Beam Control MCU market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.78 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period.

AI Adaptive Headlight Beam Control MCUs are specialized microcontroller units that integrate sensor‑fusion algorithms, real‑time image processing and power‑efficient actuation to dynamically adjust headlamp beam patterns according to traffic conditions, weather and driver intent. These devices combine high‑performance CPUs, dedicated vision accelerators and automotive‑grade safety features such as functional safety (ISO 26262) compliance.

The market is experiencing rapid growth because vehicle electrification and advanced driver‑assistance systems (ADAS) are driving demand for smarter lighting solutions. Furthermore, regulatory trends in Europe and North America mandating adaptive beam standards are accelerating adoption. Key players such as NXP Semiconductors, Infineon Technologies, Renesas Electronics and Texas Instruments are expanding their portfolios through strategic partnerships,for example, in March 2024 NXP announced a collaboration with a leading OEM to integrate its next‑generation adaptive headlamp MCU into premium models.

MARKET DRIVERS

Growing Demand for Autonomous Driving

AI Adaptive Headlight Beam Control MCU Market is being propelled by the rapid adoption of Level 2‑3 autonomous driving features. Vehicle manufacturers are integrating intelligent beam‑steering systems to improve nighttime visibility and reduce road‑traffic accidents, leading to a projected compound annual growth rate above 12% through 2032.

Regulatory Push for Enhanced Safety

Stringent safety regulations in Europe, North America, and China now require adaptive illumination technologies that can dynamically adjust beam patterns. Compliance pressures are prompting OEMs to adopt AI‑driven MCU solutions, which offer real‑time decision‑making and reduced glare for oncoming traffic.

➤ “Intelligent headlight control is becoming a mandatory safety feature, not just an optional upgrade.”

In addition, the convergence of AI processors with automotive‑grade MCUs enables cost‑effective integration, allowing mid‑range vehicle segments to benefit from advanced headlight functionalities without a significant price premium.

MARKET CHALLENGES

Integration Complexity with Vehicle Networks

Embedding AI adaptive headlight MCUs into CAN‑based and Ethernet‑based vehicle architectures requires sophisticated software stacks and extensive validation cycles. The need for seamless communication with ADAS, infotainment, and power‑train modules adds engineering overhead and lengthens time‑to‑market.

Other Challenges

Cost Sensitivity

Automotive buyers remain highly price‑sensitive; the added silicon and sensor costs of AI‑enabled MCUs can impede adoption in cost‑conscious markets unless economies of scale are achieved.

MARKET RESTRAINTS

High Component and Development Costs

Developing AI algorithms that meet automotive safety integrity levels (ASIL) demands significant investment in verification and functional safety certification, driving up overall project budgets.

Supply‑chain constraints for advanced sensors, such as LiDAR‑grade photodiodes and high‑resolution cameras, further restrict volume scalability, especially during periods of semiconductor shortages.

Moreover, consumers’ limited awareness of adaptive headlight benefits can delay premium pricing acceptance, restraining market momentum.

MARKET OPPORTUNITIES

Electrification and Premium Vehicle Segments

The surge in electric vehicle (EV) production creates a fertile environment for AI adaptive headlight MCUs, as EV platforms often feature flexible electronics architectures that accommodate advanced MCU integration without legacy constraints.

Luxury and premium brands are differentiating their offerings through customizable illumination experiences, such as dynamic beam patterns that synchronize with driver preferences, unlocking a high‑margin niche for AI‑powered solutions.

Finally, emerging markets in Southeast Asia and Latin America are upgrading safety standards, presenting a growth runway for cost‑optimized AI headlight systems tailored to regional vehicle fleets.

AI Adaptive Headlight Beam Control MCU Market Trends

Growth Driven by Vehicle Electrification and ADAS Integration

AI Adaptive Headlight Beam Control MCU Market expanded from a valuation of USD 0.85 billion in 2025 to USD 0.92 billion in 2026, and is projected to reach USD 1.78 billion by 2034, reflecting a steady compound annual growth of 7.6 % over the forecast horizon. This upward trajectory is anchored in the broader shift toward vehicle electrification, which creates space for higher‑performance microcontrollers that can manage complex lighting functions while preserving battery efficiency. Simultaneously, the proliferation of advanced driver‑assistance systems demands real‑time sensor fusion and image processing,capabilities that modern adaptive headlamp MCUs deliver through integrated vision accelerators and safety‑grade CPU cores.

Other Trends

Regulatory Momentum in Europe and North America

Legislative frameworks in key regions are accelerating market adoption. Europe’s mandatory adaptive beam standards for new passenger cars, combined with North American guidelines that prioritize glare reduction, compel OEMs to source compliant MCUs. These regulations push manufacturers to integrate functional safety features such as ISO 26262 compliance directly into the microcontroller architecture, reducing the need for separate safety modules and shortening development cycles.

Strategic Partnerships Expanding MCU Portfolios

Leading semiconductor firms are consolidating their position through collaborations and product extensions. In March 2024, NXP Semiconductors announced a partnership with a major OEM to embed its next‑generation adaptive headlamp MCU in premium vehicle lines, while Infineon Technologies and Renesas Electronics have launched joint development programs targeting power‑efficient vision pipelines. Texas Instruments continues to augment its offering with scalable MCU families that support both legacy and future ADAS lighting architectures, ensuring a broad addressable base across market segments.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Adaptive Headlight Beam Control MCU Market Competitive Overview

AI Adaptive Headlight Beam Control MCU market is dominated by a handful of semiconductor powerhouses that have leveraged deep expertise in automotive microcontrollers, vision accelerators, and functional‑safety compliance. NXP Semiconductors leads the segment with a robust portfolio that integrates sensor‑fusion algorithms and has recently announced a strategic collaboration with a premium OEM to embed its next‑generation MCU in high‑end models. Infineon Technologies follows closely, capitalising on its strong automotive safety pedigree and expanding its beam‑control IP through partnerships with Tier‑1 system integrators. Renesas Electronics and Texas Instruments round out the core quartet, each delivering high‑performance CPUs combined with low‑power vision cores that satisfy ISO 26262 requirements. The market structure reflects a classic oligopoly where the top four capture the majority of revenue, while intensive R&D investment and regulatory mandates in Europe and North America continue to raise entry barriers for new entrants.

Beyond the leading quartet, several niche and emerging players contribute specialized capabilities that enrich the competitive ecosystem. STMicroelectronics offers cost‑effective MCUs with integrated LiDAR sensor interfaces, while ON Semiconductor focuses on power‑efficient actuation circuits for adaptive headlamp arrays. Bosch and Continental bring systems‑level integration expertise, embedding MCU functionality within broader ADAS lighting modules. Denso and Melexis target OEM collaborations with compact, automotive‑grade solutions tailored for electric vehicle platforms. Microchip Technology and ROHM Semiconductor supply flexible development kits that accelerate time‑to‑market for mid‑tier manufacturers. Samsung Electronics, though primarily known for consumer chips, is advancing its automotive‑grade silicon, and Magna International leverages its global supply chain to deliver customised MCU variants for niche market segments.

List of Key AI Adaptive Headlight Beam Control MCU Companies Profiled

- NXP Semiconductors

- Infineon Technologies

- Renesas Electronics

- Texas Instruments

- STMicroelectronics

- ON Semiconductor

- Bosch

- Continental

- Denso

- Melexis

- Microchip Technology

- ROHM Semiconductor

- Samsung Electronics

- Magna International

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Sensor‑Fusion MCUs are increasingly favored because they seamlessly combine data from cameras, LiDAR and radar to generate a unified perception of road conditions. • They enable real‑time beam pattern adjustment that aligns with driver intent and external lighting regulations. • Their architecture supports functional safety compliance, making them attractive to OEMs seeking robust ADAS integration. |

| By Application |

|

Passenger Vehicles dominate adoption as manufacturers embed adaptive headlamp MCUs to meet tightening European and North American lighting standards. • The technology enhances night‑time visibility while reducing glare for oncoming traffic, aligning with safety‑first branding. • Integration with broader ADAS suites creates a seamless driver‑assist experience, encouraging OEMs to prioritize these MCUs in new model line‑ups. |

| By End User |

|

OEMs lead the demand curve as they embed AI‑driven headlamp MCUs directly into vehicle platforms to satisfy regulatory and consumer expectations. • Their design cycles increasingly require early‑stage MCU selection that balances processing power with automotive‑grade reliability. • Partnerships with silicon leaders such as NXP and Infineon accelerate technology transfer, fostering rapid feature rollout across model generations. |

| By Vehicle Architecture |

|

Electric Vehicles are emerging as a pivotal segment because their higher voltage architectures enable power‑efficient actuation of adaptive beams. • The quiet cabin environment of EVs accentuates the perceived benefit of precise illumination, reinforcing brand differentiation. • MCU suppliers are tailoring low‑power vision accelerators to harmonize with EV power‑train constraints while maintaining high‑resolution processing. |

| By Functional Feature |

|

Functional Safety Certified MCUs command attention because automotive lighting systems must meet ISO 26262 standards. • These MCUs embed fault‑tolerant architectures that assure reliable beam modulation under adverse conditions. • Their safety‑centric design reduces validation effort for OEMs, streamlining the path to regulatory approval across global markets. |

Regional Analysis: AI Adaptive Headlight Beam Control MCU Market

North America

Accelerating vehicle electrification, heightened focus on night‑time safety, and federal guidelines that reward adaptive lighting all propel demand for sophisticated MCUs in the region.

A mix of legacy automotive chipmakers and agile startups compete, with collaborations across automotive OEMs, AI software firms, and silicon manufacturers shaping the ecosystem.

Federal safety standards increasingly mandate adaptive illumination, while state‑level incentive programs reward low‑glare, energy‑efficient headlight designs.

Integration of lidar‑grade vision sensors and machine‑learning‑based predictive lighting is expected to redefine driver‑assistance suites over the next decade.

Europe

Europe’s market is characterized by a strong regulatory framework that emphasizes low‑emission vehicle technologies and advanced driver‑assistance systems. German and French manufacturers lead the integration of AI‑enabled beam‑control MCUs, leveraging the region’s deep engineering talent pool. Collaborative research programs across the EU promote standardization of communication protocols, facilitating cross‑border component compatibility. While adoption rates are slightly slower than North America, the European emphasis on sustainability and precise illumination in urban environments sustains steady growth.

Asia‑Pacific

The Asia‑Pacific region benefits from rapid automotive production scaling in China, Japan, and South Korea. Government initiatives supporting smart‑city infrastructure and autonomous driving pilots encourage OEMs to embed adaptive headlight solutions. Market dynamics are shaped by cost‑focused manufacturing, yet rising consumer expectations for premium lighting in premium sedan segments drive incremental upgrades to MCU capabilities.

South America

South America presents emerging opportunities as local manufacturers modernize fleets to meet new safety mandates. Brazil’s regulatory push for adaptive lighting, coupled with increasing vehicle imports equipped with AI‑driven systems, creates a modest yet growing demand for specialized MCUs. Market development is tempered by price sensitivity, prompting partnerships that leverage cost‑effective silicon solutions.

Middle East & Africa

In the Middle East & Africa, luxury vehicle penetration fuels niche demand for advanced headlight technologies, particularly in wealthy Gulf markets. Meanwhile, African nations focus on improving road safety standards, gradually introducing adaptive illumination in newer vehicle segments. The region’s fragmented supply chain and reliance on imports shape a market that is poised for gradual expansion as awareness of AI‑based lighting benefits spreads.

Report Scope

This market research report provides a comprehensive analysis of the AI Adaptive Headlight Beam Control MCU Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Adaptive Headlight Beam Control MCU Market?

-> AI Adaptive Headlight Beam Control MCU market is projected to grow from USD 0.92 billion in 2026 to USD 1.78 billion by 2034, exhibiting a CAGR of 7.6%

Which key companies operate in AI Adaptive Headlight Beam Control MCU Market?

-> Key players include NXP Semiconductors, Infineon Technologies, Renesas Electronics, Texas Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include vehicle electrification, advanced driver‑assistance systems (ADAS) adoption, and regulatory standards for adaptive lighting.

Which region dominates the market?

-> Europe is a leading region due to stringent adaptive‑beam regulations, while North America also shows strong demand.

What are the emerging trends?

-> Emerging trends include AI‑driven sensor fusion, functional safety (ISO 26262) enhancements, and advanced vision accelerator integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...