Advanced FPGA Market Insights

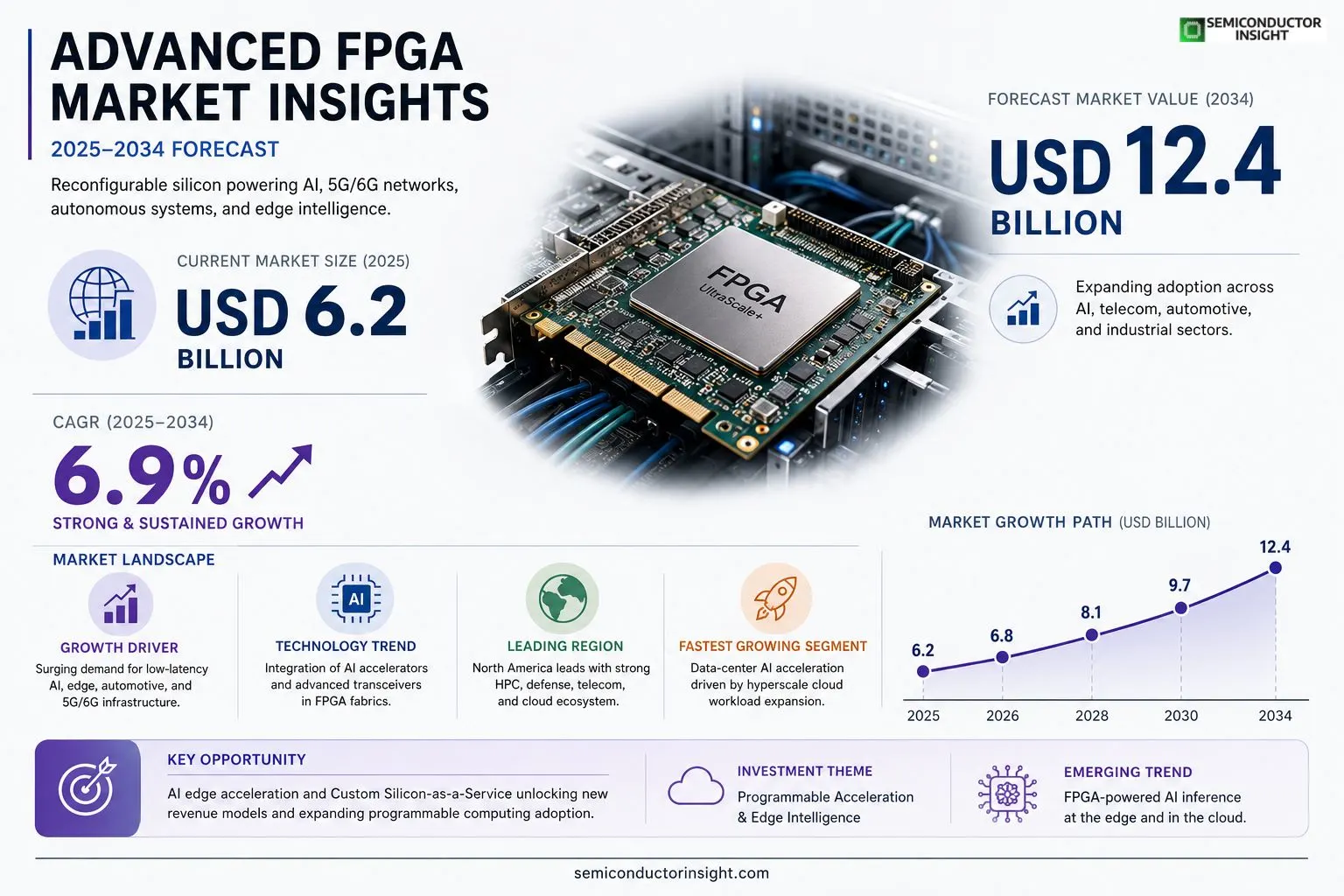

Advanced FPGA market size was valued at USD 6.2 billion in 2025. The market is projected to grow from USD 6.8 billion in 2025 to USD 12.4 billion by 2034, exhibiting a CAGR of 6.9%.

Advanced field‑programmable gate arrays (FPGAs) are high‑performance reconfigurable silicon devices that combine logic fabric, high‑speed transceivers, embedded processors and specialized IP blocks such as DSP slices and AI accelerators.

They enable designers to implement complex algorithms directly in hardware while retaining post‑silicon flexibility.The market is accelerating because demand for low‑latency processing in data‑center AI workloads, autonomous‑vehicle computing and edge intelligence is surging.

Furthermore, increased capital spending on next‑generation telecommunications infrastructure,particularly Open RAN and emerging 6G research,drives adoption of programmable silicon that can be updated without full redesigns.Key players such as AMD (Xilinx), Intel (Altera), Lattice Semiconductor and Microchip Technology are expanding their portfolios through new silicon nodes and strategic partnerships; for example, in March 2024 AMD announced a joint development agreement with a leading cloud provider to integrate its UltraScale+ series into hyperscale AI servers.

MARKET DRIVERS

Rising Demand for High‑Performance Computing

Advanced FPGA Market is being propelled by the exponential growth of data‑center workloads that require low‑latency, high‑throughput processing. Enterprises are adopting reconfigurable architectures to accelerate AI inference, which delivers up to 4× better performance per watt compared to traditional ASIC solutions.

Expansion of 5G Infrastructure

Telecommunications operators are deploying massive‑MIMO and beam‑forming technologies that rely on the flexibility of advanced FPGAs. This shift is expected to boost market revenue by an estimated 12% annually as network equipment manufacturers integrate these programmable devices into base‑station hardware.

➤ Strategic partnerships between FPGA vendors and cloud providers are accelerating time‑to‑market for customized compute solutions, driving broader adoption across multiple verticals.

Furthermore, the convergence of edge computing and IoT is creating new use cases where power‑efficient, reconfigurable logic is essential, reinforcing the overall growth trajectory of the sector.

MARKET CHALLENGES

Complex Design Toolchains

Designing for Advanced FPGA Market requires sophisticated software ecosystems that many engineering teams find daunting. The steep learning curve can delay product launches and increase development costs, especially for small‑to‑mid‑size enterprises.

Other Challenges

Talent Shortage

A limited pool of engineers proficient in hardware description languages and high‑level synthesis hampers rapid deployment, forcing companies to invest heavily in training programs.

Supply Chain Volatility

Geopolitical tensions and semiconductor fab capacity constraints have introduced lead‑time uncertainties, making it difficult for manufacturers to forecast inventory and maintain steady production schedules.

MARKET RESTRAINTS

High Initial Capital Expenditure

The upfront cost of acquiring advanced FPGA platforms, combined with licensing fees for proprietary IP cores, can be prohibitive for cost‑sensitive projects, limiting market penetration in certain regions.

Regulatory Compliance

Stringent safety and security certifications required in aerospace, defense, and automotive sectors add layers of testing and documentation, extending time‑to‑market and increasing overall project budgets.

MARKET OPPORTUNITIES

AI Edge Acceleration

Deploying AI models directly on edge devices using Advanced FPGA Market enables real‑time analytics while preserving data privacy. This approach is attracting investments from consumer electronics firms seeking to differentiate their product lines.

Custom Silicon‑as‑a‑Service

Emerging business models that offer FPGA resources on a subscription basis are lowering entry barriers and creating recurring revenue streams, positioning vendors to capture a larger share of the growing programmable logic ecosystem.

Advanced FPGA Market Trends

Rising Demand for Low‑Latency AI Compute

Designers are turning to high‑performance, reconfigurable silicon to meet the accelerating need for sub‑microsecond response times in modern AI workloads. Data‑center operators, especially those supporting large‑scale generative‑AI models, are integrating advanced field‑programmable gate arrays to offload inference kernels, reduce power per operation, and retain the ability to update algorithms after silicon deployment. This flexibility is crucial as AI model architectures evolve faster than traditional ASIC design cycles, allowing hyperscale providers to stay competitive without costly redesigns. The trend underscores a broader industry shift toward programmable acceleration that balances performance, cost, and upgradeability.

Other Trends

Edge and Autonomous Vehicle Expansion

Edge intelligence and autonomous‑vehicle platforms benefit from the same combination of high‑speed transceivers, embedded processors, and DSP slices that define the advanced FPGA family. By placing compute close to the sensor stack, manufacturers achieve deterministic latency essential for real‑time perception and decision‑making. Recent vehicle prototypes demonstrate lane‑keeping and obstacle‑avoidance functions implemented directly in reconfigurable fabric, enabling OTA updates that improve safety algorithms without hardware replacement. Similarly, edge devices in industrial IoT settings use these devices to perform on‑site analytics, reducing reliance on cloud connectivity and minimizing bandwidth costs.

Telecommunications Shift Toward Open RAN and 6G

Next‑generation telecom infrastructure is another catalyst. Open RAN deployments require programmable radio units that can adapt to evolving standards, a need met by advanced FPGA solutions with multi‑gigabit transceivers and built‑in AI accelerators. Emerging 6G research further amplifies this demand, as future air‑interface designs anticipate dynamic spectrum sharing and AI‑driven beamforming. Leading silicon vendors have announced joint development agreements with cloud and network operators to integrate new FPGA families into hyperscale server racks and base‑station platforms. These collaborations aim to reduce time‑to‑market for novel services while preserving hardware longevity through software‑defined updates.

COMPETITIVE LANDSCAPEKey Industry Players

Advanced FPGA Market – Competitive Overview

Advanced FPGA Market is currently dominated by a few large silicon vendors that leverage deep R&D budgets and advanced process nodes to deliver high‑performance, low‑latency devices. AMD (through its Xilinx UltraScale+ family) and Intel (with Stratix and Agilex families) collectively command the majority of revenue, owing to their ability to integrate high‑speed transceivers, hardened AI accelerators, and heterogeneous CPU cores on a single die. Their strategic partnerships with hyperscale cloud providers and telecom operators reinforce a market structure that favors scale, ecosystem support, and rapid technology refresh cycles. Both companies are aggressively expanding into 3‑nm and 5‑nm nodes, which further squeezes the competitive space for smaller players.Beyond the two tier‑1 leaders, a vibrant set of niche innovators sustains differentiation through specialized IP blocks, low‑power form factors, and rapid time‑to‑market solutions. Lattice Semiconductor focuses on ultra‑low‑power and edge‑centric FPGAs, while Microchip Technology (including the former Microsemi portfolio) targets security‑hardened and automotive‑grade devices. Achronix delivers high‑bandwidth, high‑capacity solutions for data‑center acceleration, and QuickLogic emphasizes AI‑enabled edge processors. Additional contributors such as Xilinx’s legacy product lines (now under AMD), Intel’s former Altera assets, and emerging players like Flex Logix and PolarFire continue to enrich the ecosystem with unique silicon architectures and software toolchains.

List of Key Advanced FPGA Companies Profiled

- AMD (Xilinx)

- Intel (Altera)

- Lattice Semiconductor

- Microchip Technology

- Achronix Semiconductor

- QuickLogic Corporation

- Flex Logix Technologies

- PolarFire (Microsemi)

- SiFive (RISC‑V FPGA hybrids)

- Broadcom Inc.

- Cadence Design Systems

- Xilinx (legacy)

- Atmel Corporation

- Infineon Technologies

- Renesas Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High‑Performance drives the market because it offers the compute density required for modern AI algorithms, enables rapid iteration of hardware pipelines, and supports seamless post‑silicon updates. • Designers prioritize flexibility to meet evolving workloads without redesign. • Integration of AI‑specific IP blocks accelerates time‑to‑market for data‑center solutions. • Ecosystem support from leading toolchains reinforces adoption. |

| By Application |

|

Data‑Center AI Acceleration is the leading application as hyperscale operators seek reconfigurable silicon to meet surging low‑latency AI inference demand. • Advanced transceivers and high‑speed memory interfaces enable seamless scaling of neural‑network models. • The ability to update logic after deployment reduces capital cycle times. • Partnerships between FPGA vendors and cloud providers reinforce a feedback loop of innovation. |

| By End User |

|

Cloud Service Providers dominate end‑user demand because they require scalable, upgradable compute fabrics to support diverse AI workloads across shared infrastructure. • Reconfigurability aligns with multi‑tenant service models. • Integration of DSP slices and AI accelerators meets both inference and training needs. • Continuous firmware upgrades prolong hardware relevance, driving cost efficiency. |

| By Architecture |

|

UltraScale+ Series emerges as the preferred architecture for cutting‑edge AI and 6G research due to its dense logic resources, high‑throughput transceivers, and integrated AI engines. • Multi‑die interconnects enable massive parallelism. • Built‑in security features address emerging data‑protection concerns. • Roadmap alignment with next‑generation process nodes ensures sustained performance gains. |

| By Deployment Scenario |

|

Hyperscale Servers lead deployment because they capitalize on the FPGA’s ability to offload latency‑critical tasks while preserving a unified hardware base across diverse workloads. • Consolidation of AI, networking, and storage functions simplifies system design. • Rapid re‑programming supports evolving service portfolios. • Close collaboration with silicon vendors drives co‑optimization of firmware and hardware stacks. |

Regional Analysis: North America

United States

The aerospace and defense sector represents a substantial portion of Advanced FPGA Market in the United States. FPGAs are utilized in radar systems, electronic warfare, and satellite communications, benefiting from increasing defense spending and the need for enhanced signal processing capabilities. Demand is driven by the growing complexity of modern defense systems and the requirement for real-time data analysis. Companies are focusing on developing FPGAs with enhanced security features to address the evolving threat landscape.

The telecommunications infrastructure sector is a key driver of advanced FPGA adoption. FPGAs are integral to 5G and future network infrastructure, enabling high-speed data transmission, network virtualization, and edge computing. The need for low-latency, high-bandwidth connectivity is propelling demand for FPGAs in base stations, core networks, and optical transport systems. Innovation in FPGA architectures is focused on improving power efficiency and scalability for these deployments.

The HPC market within the United States presents significant growth opportunities for advanced FPGAs. These are used in scientific research, data analytics, and AI/ML workloads, providing acceleration for computationally intensive tasks. The demand for FPGAs in HPC is driven by the need to reduce processing time and improve energy efficiency. The rise of exascale computing is further boosting the adoption of FPGA-based solutions.

Advanced FPGAs are finding increasing applications in automotive electronics, particularly in advanced driver-assistance systems (ADAS) and autonomous driving. They are used for sensor fusion, image processing, and real-time decision-making. The stringent safety and reliability requirements of the automotive industry are driving demand for FPGAs with high levels of functional safety certification.

Europe

The European advanced FPGA market is experiencing steady growth, driven by strong demand from the automotive, industrial, and aerospace & defense sectors. Government initiatives supporting technological innovation and manufacturing are contributing to market expansion. Integration of FPGAs in automotive ADAS and autonomous driving solutions presents a significant opportunity. The focus on energy efficiency and power management is a key trend in the European market. European companies are also investing in R&D to develop specialized FPGA solutions for industrial automation and data center applications.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in Advanced FPGA Market. Driven by rapid industrialization, increasing investments in infrastructure, and the proliferation of 5G networks, the region offers substantial growth potential. China is a major market, with significant demand from telecommunications, consumer electronics, and industrial automation sectors. The region’s strong manufacturing base and growing electronics industry are further boosting FPGA adoption. The focus on edge computing and AI/ML applications is driving demand for FPGAs in various industries.

South America

South America’s advanced FPGA market is nascent but poised for growth. The increasing adoption of 5G, growing industrialization, and rising demand for data analytics are creating opportunities for FPGA-based solutions. The telecommunications sector is expected to be a key driver of growth, with demand for FPGAs in network infrastructure and base stations. Government investments in infrastructure projects are also contributing to market expansion.

Middle East & Africa

The Middle East & Africa advanced FPGA market is characterized by growth driven by investments in infrastructure, defense, and industrial sectors. The expansion of 5G networks, particularly in countries like Saudi Arabia and the UAE, is creating demand for FPGAs in telecommunications infrastructure. Government initiatives promoting technological advancement and economic diversification are further supporting market growth.

Report Scope

This market research report provides a comprehensive analysis of the Advanced FPGA Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Advanced FPGA Market?

-> Advanced FPGA Market was valued at USD 6.2 billion in 2025 and is expected to reach USD 12.4 billion by 2034, representing a CAGR of 6.9%.

Which key companies operate in Advanced FPGA Market?

-> Key players include AMD (Xilinx), Intel (Altera), Lattice Semiconductor, and Microchip Technology.

What are the key growth drivers?

-> Key growth drivers include rising demand for low‑latency processing in data‑center AI workloads, autonomous‑vehicle computing, edge intelligence, and increased capital spending on next‑generation telecommunications infrastructure such as Open RAN and emerging 6G research.

Which region dominates the market?

-> The reference material does not specify a single dominant region for Advanced FPGA Market.

What are the emerging trends?

-> Emerging trends include integration of AI accelerators within FPGA fabrics, expanded use in data‑center AI, autonomous vehicles, edge computing, and programmable silicon solutions for Open RAN and future 6G networks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...