8.5-generation Substrate Glass Market Insights

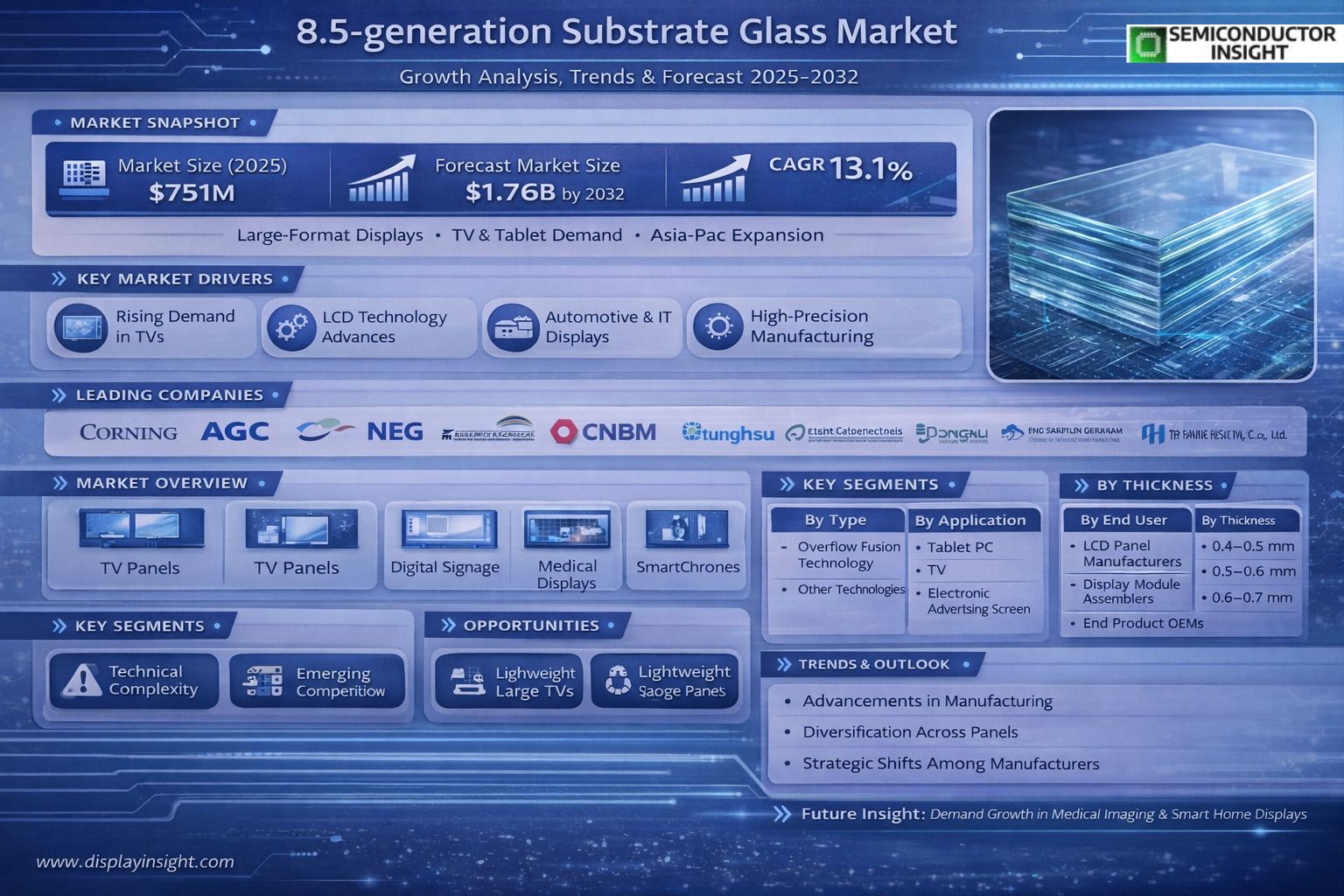

Global 8.5-generation Substrate Glass market size was valued at USD 757 million in 2025. The market is projected to reach USD 1757 million by 2032, exhibiting a CAGR of 13.1% during the forecast period.

Generation 8.5 Glass Substrate is the core key material for manufacturing high-generation liquid crystal display panels. It has the characteristics of large size, excellent thermal stability, high mechanical strength, excellent chemical resistance, and extremely low surface and internal defect rates. Its quality and performance play a decisive role in key quality indicators such as resolution, transmittance, refresh rate and viewing angle of display panels. During the production process, its control accuracy is comparable to that of the semiconductor industry, demonstrating the pinnacle level of modern glass scale manufacturing technology in the world.

The market is experiencing rapid growth driven by surging demand for large-format displays in TVs, tablets, and electronic advertising screens. Advancements in panel fabrication technologies and capacity expansions by major manufacturers in Asia further accelerate this momentum. Key players including Corning, AGC, NEG, and China National Building Material lead the industry, leveraging innovations like Overflow Fusion Technology to maintain competitive edges. These companies collectively command a substantial revenue share, supported by ongoing investments in production precision and defect reduction.

MARKET DRIVERS

Rising Demand for Large-Screen Displays

8.5-generation Substrate Glass Market is propelled by surging consumer preference for ultra-high-definition televisions and monitors exceeding 75 inches. With global TV shipments reaching approximately 220 million units in 2023, manufacturers are scaling production lines optimized for Gen 8.5 glass sheets measuring 2200mm x 2500mm, enabling efficient cutting yields for 65-85 inch panels.

Advancements in LCD Technology

Innovations in **quantum dot** and **mini-LED backlighting** integrated with Gen 8.5 substrates enhance picture quality, driving adoption in premium segments. Market data indicates a 6.2% CAGR through 2028, fueled by replacement cycles in commercial displays like digital signage, where durability of alkali-free glass proves essential for high-volume output.

➤ Key Driver: Expansion in Automotive and IT Displays – Gen 8.5 substrates support curved and flexible panel designs, capturing 15% of new automotive HUD markets.

Overall, strategic investments by leading suppliers like Corning and AGC in capacity expansions underscore robust momentum in 8.5-generation Substrate Glass Market.

MARKET CHALLENGES

Technical Manufacturing Hurdles

8.5-generation Substrate Glass Market faces complexities in float process scaling, where thermal uniformity across larger sheets leads to defect rates up to 2-3% higher than Gen 8. Precise polishing and chemical strengthening demand advanced cleanroom protocols to mitigate contamination risks.

Other Challenges

Supply chain disruptions, including raw material silica purity fluctuations, exacerbate yield inconsistencies, with production downtime averaging 5% annually in Asia-Pacific facilities.

Cost Pressures and Yield Optimization

Elevated capital expenditures for Gen 8.5 lines, often exceeding $2 billion per fab, strain profitability amid volatile panel prices, necessitating continuous process refinements for over 90% material utilization.

MARKET RESTRAINTS

Shift Toward OLED Alternatives

Intensifying competition from organic light-emitting diode (OLED) panels, which bypass rigid substrate needs, caps growth in 8.5-generation Substrate Glass Market. OLED TV market share climbed to 12% in 2023, diverting demand from LCD-reliant Gen 8.5 applications.

Regulatory pressures on energy efficiency further challenge LCD substrates, as stricter standards favor self-emissive technologies, potentially reducing Gen 8.5 demand by 4-5% over the next quinquennium.

Geopolitical tensions disrupt key supply hubs in Japan and South Korea, imposing tariffs and export controls that elevate costs by up to 10% for global integrators.

Maturing LCD technology limits pricing power, with average substrate costs declining 3% yearly, compressing margins for producers in 8.5-generation Substrate Glass Market.

MARKET OPPORTUNITIES

Expansion into Emerging Display Applications

8.5-generation Substrate Glass Market holds potential in **medical imaging** and **industrial HMI panels**, where high-resolution requirements align with Gen 8.5 yields, projecting a 7% uptake in non-consumer segments by 2027.

Development of thinner, high-TTV substrates enables lightweight large-format TVs, capturing premium smart home markets valued at $50 billion globally.

Sustainability initiatives favor recyclable Gen 8.5 glass over plastics, opening avenues in e-sports arenas and public venues with projected installations doubling to 1.2 million units by 2026.

8.5-generation Substrate Glass Market Trends

Advancements in High-Precision Manufacturing

8.5-generation Substrate Glass Market continues to evolve driven by its critical role as the core material in producing high-generation liquid crystal display panels. Renowned for large size dimensions, excellent thermal stability, high mechanical strength, superior chemical resistance, and extremely low defect rates on surfaces and internals, this glass substrate directly influences key display performance metrics including resolution, transmittance, refresh rate, and viewing angles. Production processes mirror the precision of the semiconductor industry, positioning it at the forefront of modern glass manufacturing technology.

Other Trends

Diversification Across Display Applications

Demand in 8.5-generation Substrate Glass Market is propelled by expanding applications in Tablet PCs, TVs, and electronic advertising screens. These sectors benefit from the substrate’s ability to support larger panels with consistent quality, enabling manufacturers to meet rising consumer expectations for immersive viewing experiences. Industry surveys highlight steady growth in these areas, with suppliers focusing on customization to address specific performance needs in each segment.

Strategic Shifts Among Key Manufacturers

Leading players such as Corning, AGC, NEG, and China National Building Material dominate 8.5-generation Substrate Glass Market, emphasizing innovations in Overflow Fusion Technology alongside other methods. Competitive dynamics reveal efforts to enhance supply chain resilience, with regional expansions in Asia—particularly China, Japan, and South Korea—strengthening production capacities. Distributors and experts note increasing focus on reducing defects and improving scalability to counter challenges like raw material fluctuations and technological barriers. This positions the market for sustained development as display technologies advance toward higher generations.

COMPETITIVE LANDSCAPE

Key Industry Players

Top Manufacturers Driving 8.5-generation Substrate Glass Market

8.5-generation Substrate Glass Market exhibits an oligopolistic structure dominated by a handful of global leaders, primarily Corning, AGC Inc., and Nippon Electric Glass (NEG). These top-tier manufacturers collectively hold a substantial revenue share, with the global top five players accounting for the majority of the market as of 2025. Corning leads with its advanced EAGLE XG glass produced via proprietary Overflow Fusion Technology, offering superior thermal stability, mechanical strength, and low defect rates critical for high-resolution LCD panels in TVs, tablets, and electronic advertising screens. High entry barriers, including massive capital investments in precision manufacturing facilities comparable to semiconductor fabs, reinforce this concentrated landscape, where production control accuracy determines panel quality metrics like transmittance and refresh rates.

Beyond the frontrunners, niche and emerging players, particularly from China, are intensifying competition through aggressive capacity expansions and cost efficiencies. Companies like China National Building Material (CNBM) and Tunghsu Optoelectronic are ramping up Gen 8.5 production to capture regional demand in Asia, driven by the booming display panel industry. These challengers focus on localized supply chains and incremental innovations, gradually eroding the dominance of Japanese and U.S. incumbents. Other significant participants include specialized suppliers addressing specific applications or regional needs, fostering a dynamic environment with ongoing mergers, capacity announcements, and technology adaptations amid a projected market CAGR of 13.1% through 2032.

List of Key 8.5-generation Substrate Glass Companies Profiled

- Corning Incorporated

- AGC Inc.

- Nippon Electric Glass Co., Ltd. (NEG)

- China National Building Material Company Limited (CNBM)

- Tunghsu Optoelectronic Technology Co., Ltd.

- AVIC Sanxin Co., Ltd.

- Hengshui Xinhua Optoelectronic Materials Co., Ltd.

- Dongxu Optoelectronic Technology Co., Ltd.

- CAIHONG (Group) Co., Ltd.

- Electric Glass Technology Co., Ltd.

- Nippon Sheet Glass Co., Ltd. (NSG)

- SCHOTT AG

- Asahi Kasei Corporation

- Sumitomo Chemical Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Overflow Fusion Technology

|

| By Application |

|

TV

|

| By End User |

|

LCD Panel Manufacturers

|

| By Thickness |

|

0.4-0.5 mm

|

| By Panel Resolution |

|

4K UHD

|

Regional Analysis: 8.5-generation Substrate Glass Market

Asia-Pacific

China’s expansive industrial parks specialize in 8.5-generation Substrate Glass Market production, leveraging economies of scale. Proximity to display giants streamlines logistics, minimizing lead times. Local policies promote technological upgrades, enhancing yield rates and surface quality for superior display performance.

South Korean firms excel in precision engineering for 8.5-generation substrates, integrating advanced polishing and coating methods. Strategic partnerships drive process innovations, supporting premium OLED-LCD hybrids. Export-oriented strategies bolster global market penetration.

Japan’s expertise in ultra-thin glass composition advances 8.5-generation Substrate Glass Market. R&D focuses on durability enhancements for curved displays. Collaborative ecosystems ensure rapid commercialization of breakthroughs.

Asia-Pacific’s integrated supply chains mitigate risks in 8.5-generation Substrate Glass Market. Diversified sourcing and digital tracking optimize inventory. Sustainability efforts, like low-emission furnaces, align with regulatory trends.

North America

North America exhibits steady growth in 8.5-generation Substrate Glass Market, fueled by demand from high-end consumer electronics and automotive displays. U.S.-based firms prioritize customization for specialized applications like medical imaging panels. Strategic alliances with Asian suppliers ensure access to cutting-edge substrates while fostering local assembly. Investments in automation enhance processing capabilities, reducing dependency on imports. Business strategies focus on premium segments, leveraging brand strength in North American markets. Emerging trends toward flexible displays prompt R&D in adaptable glass formulations. Regulatory emphasis on energy efficiency drives adoption of advanced coatings. Despite import reliance, North America’s innovation hubs contribute to global standards, positioning it for expansion through 2034 as display integration in smart devices accelerates.

Europe

Europe’s 8.5-generation Substrate Glass Market thrives on stringent quality standards and diversified applications in industrial and commercial displays. Germany and the Netherlands lead with precision manufacturing tailored for European automotive sectors. Collaborative EU-funded projects advance eco-friendly production methods, aligning with green directives. Firms emphasize modular designs for versatile panel sizes, supporting growth in digital signage. Supply chain diversification mitigates geopolitical risks, enhancing resilience. Business strategies integrate circular economy principles, promoting glass reuse. As consumer demand for sustainable products rises, Europe’s focus on high-value innovations sustains competitive edges. Through 2034, regulatory frameworks will propel advancements in lightweight substrates for next-gen displays.

South America

South America is an emerging player in 8.5-generation Substrate Glass Market, with Brazil spearheading localization efforts for consumer displays. Rising middle-class consumption drives demand for affordable large-screen TVs, prompting imports and nascent domestic processing. Partnerships with Asian leaders transfer technology, building local expertise. Infrastructure investments improve logistics, easing substrate distribution. Business strategies target cost optimization and volume growth amid economic recovery. Sustainability initiatives adapt to regional challenges like resource scarcity. As urbanization accelerates, opportunities in public displays expand. By 2034, strategic capacity builds will elevate South America’s role in global supply dynamics.

Middle East & Africa

The Middle East & Africa region shows promising potential in 8.5-generation Substrate Glass Market, centered on Gulf states’ diversification from oil. Investments in entertainment hubs boost demand for premium display substrates in commercial venues. Africa’s growing tech adoption fuels entry-level applications. Collaborations with international suppliers establish assembly lines, creating jobs. Business strategies emphasize infrastructure development and skill-building. Adaptation to harsh climates drives durable glass innovations. Through 2034, rising digital transformation will amplify market traction, integrating 8.5-generation substrates into smart city projects.

Report Scope

This market research report provides a comprehensive analysis of 8.5-generation Substrate Glass Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of 8.5-generation substrate glass in powering advancements across industries such as consumer electronics, televisions, tablet PCs, and electronic advertising screens.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 8.5-generation Substrate Glass Market?

-> 8.5-generation Substrate Glass Market was valued at USD 757 million in 2025 and is expected to reach USD 1757 million by 2032 at a CAGR of 13.1% during the forecast period.

Which key companies operate in 8.5-generation Substrate Glass Market?

-> Key players include Corning, AGC, NEG, China National Building Material, among others.

What are the key growth drivers?

-> Key growth drivers include demand for high-generation liquid crystal display panels, excellent thermal stability, high mechanical strength, and low defect rates.

Which region dominates the market?

-> Asia is the fastest-growing region, while China holds significant market share.

What are the emerging trends?

-> Emerging trends include Overflow Fusion Technology, applications in Tablet PC, TV, and Electronic Advertising Screens.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...