6G RF Semiconductor Market Insights

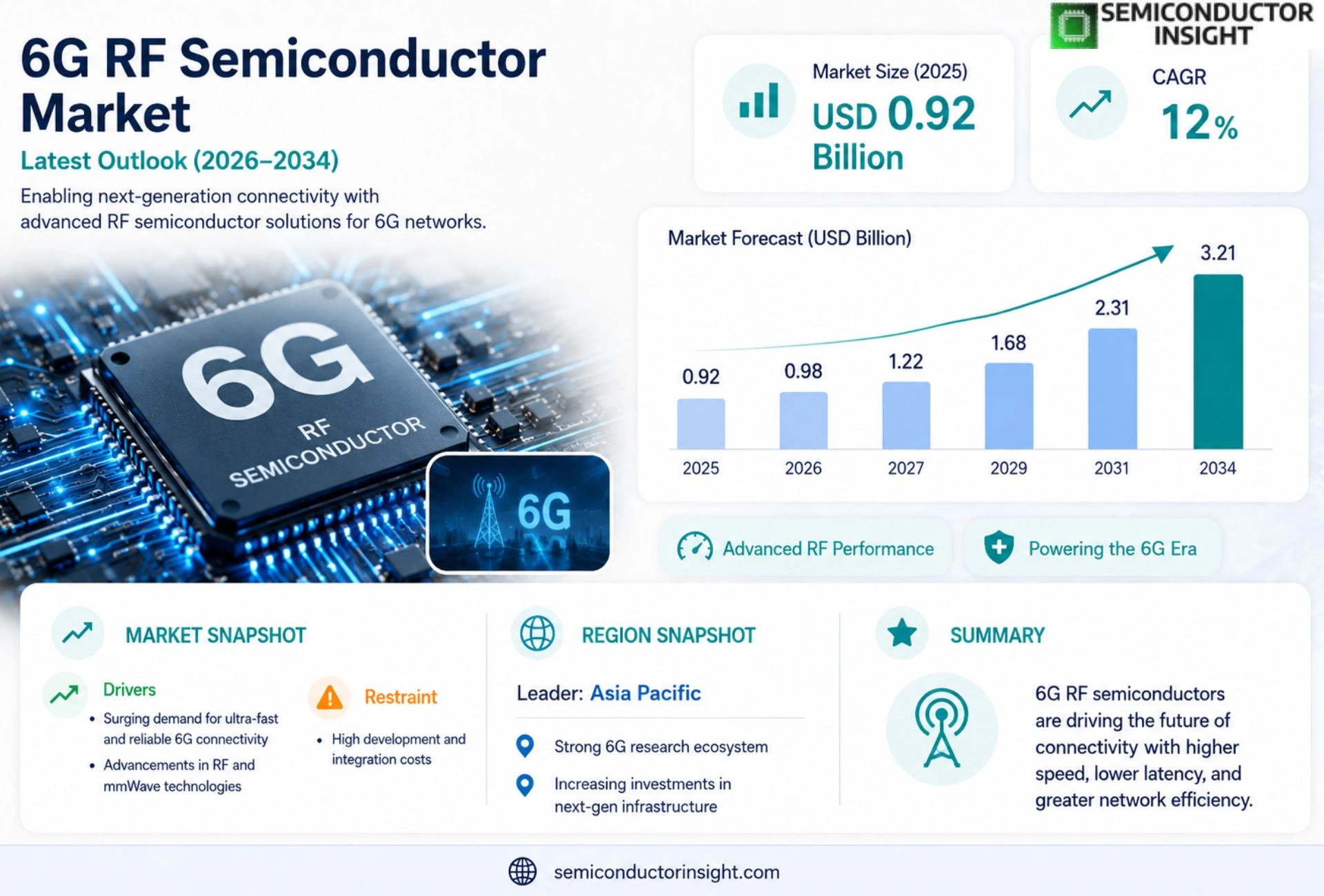

Global 6G RF Semiconductor Market size was valued at USD 0.92 billion in 2025. The market is projected to grow from USD 0.98 billion in 2026 to USD 3.21 billion by 2034, exhibiting a CAGR of 12% during the forecast period.

6G RF semiconductors are advanced radio‑frequency components that enable ultra‑high‑frequency signal generation, modulation, and reception required for next‑generation wireless communication beyond the capabilities of existing 5G infrastructure. These devices include power amplifiers, low‑noise amplifiers, switches, and phased‑array transceiver ICs built on silicon‑germanium (SiGe), gallium nitride (GaN), and other compound semiconductor technologies.

The market is experiencing rapid growth because telecom operators are investing heavily in research trials for terahertz bands, while device manufacturers accelerate development of high‑performance mmWave modules to meet anticipated bandwidth demands of several terabits per second. Furthermore, governmental initiatives such as the U.S.–EU collaborative roadmap for next‑generation connectivity and strategic funding from Asian economies are driving ecosystem expansion. Key players,including Qualcomm, NXP Semiconductors, Infineon Technologies, Qorvo, and Skyworks Solutions,are launching new GaN‑based power amplifiers and integrating AI‑optimized design tools to shorten time‑to‑market.

MARKET DRIVERS

Rapid Adoption of 6G Infrastructure

The rollout of 6G networks is accelerating across major economies, prompting telecom operators to invest heavily in high‑frequency front‑ends. This creates a strong demand for advanced RF semiconductor solutions that can support bandwidths exceeding 1 THz.

Growth of Edge Computing and AI‑Driven Devices

Edge‑enabled AI applications require ultra‑low latency and high‑speed data transfer, driving manufacturers to adopt semiconductor technologies with superior linearity and power efficiency. As a result, 6G RF Semiconductor Market is projected to expand at a double‑digit CAGR through the next decade.

➤ “The emergence of terahertz‑band communication will push RF component design toward new material systems such as GaN and SiC.”

Investment in research and development by leading silicon vendors is also boosting the ecosystem, ensuring a steady pipeline of next‑generation components that meet the stringent performance criteria of future wireless standards.

MARKET CHALLENGES

Complexity of Terahertz Signal Processing

Designing RF paths that operate reliably at terahertz frequencies involves intricate electromagnetic modeling and precise manufacturing tolerances, which can increase time‑to‑market and cost.

Other Challenges

Supply Chain Constraints

The reliance on rare‑earth materials and specialized foundries creates bottlenecks, especially when demand spikes across multiple high‑tech sectors.

MARKET RESTRAINTS

Regulatory and Standardization Uncertainty

Global regulatory bodies have yet to finalize spectrum allocations for 6G, leaving manufacturers hesitant to commit large capital expenditures without clear guidelines.

Moreover, the lack of unified testing standards for terahertz components hampers cross‑border certification, slowing adoption in regions with strict compliance requirements.

These uncertainties can deter smaller players from entering the market, consolidating activity among a few well‑funded incumbents.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and Healthcare

Automotive radar systems and high‑resolution medical imaging are exploring terahertz frequencies for enhanced perception and diagnostic capabilities. This creates a niche yet rapidly growing demand segment for 6G RF Semiconductor Market.

Additionally, the push toward satellite mega‑constellations that rely on inter‑satellite links at millimeter‑wave and terahertz bands presents a sizeable opportunity for vendors that can deliver radiation‑hard, space‑qualified RF solutions.

Strategic partnerships between semiconductor firms and system integrators are expected to accelerate technology transfer, unlocking new revenue streams and expanding market reach.

6G RF Semiconductor Market Trends

Terahertz Band Expansion

6G RF Semiconductor Market is experiencing a decisive shift toward terahertz‑band deployments. Telecom operators worldwide are allocating substantial R&D budgets to validate ultra‑high‑frequency signal pathways, which promise bandwidths far beyond current 5G capabilities. This momentum is reinforced by the emergence of power amplifiers and low‑noise amplifiers that can operate reliably in the terahertz spectrum, enabling data rates measured in multiple terabits per second. As equipment manufacturers accelerate the rollout of mmWave modules, the ecosystem surrounding 6G RF Semiconductor Market becomes increasingly robust, driving a virtuous cycle of technology adoption and component innovation.

Other Trends

AI‑Optimized Design Tools

Leading suppliers such as Qualcomm, NXP Semiconductors, Infineon Technologies, Qorvo, and Skyworks Solutions are embedding artificial‑intelligence workflows into the semiconductor design process. These AI‑driven platforms analyze vast libraries of silicon‑germanium and gallium‑nitride device parameters to suggest optimal layout configurations, thereby shortening time‑to‑market and reducing prototyping costs. The integration of machine‑learning algorithms with electromagnetic simulation tools is also improving yield predictability for phased‑array transceiver ICs, a critical factor for the high‑performance demands of 6G networks. This trend not only enhances product quality but also aligns with the broader industry push toward digital twins and automated verification.

Strategic Government Funding

Governmental initiatives are playing a pivotal role in shaping the trajectory of 6G RF Semiconductor Market. Coordinated roadmaps between the United States and the European Union outline joint research programs targeting terahertz communication standards, while Asian economies are channeling strategic funding toward domestic semiconductor fabrication capabilities. These policy‑driven investments are creating a favorable environment for cross‑border collaboration, encouraging the establishment of shared testbeds, and accelerating the standardization of high‑frequency interfaces. As a result, the market benefits from a steady influx of capital, talent, and regulatory support that collectively underpin the rapid commercialization of next‑generation RF solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of 6G RF Semiconductor Market

6G RF Semiconductor Market is currently anchored by a handful of globally recognized firms that dominate high‑power GaN and SiGe device portfolios. Qualcomm leverages its extensive RF front‑end IP to co‑develop GaN‑based power amplifiers that target terahertz bands, while NXP Semiconductors adds silicon‑germanium transceiver ICs to address massive‑MIMO requirements. Infineon Technologies contributes a broad spectrum of low‑noise amplifiers and switch modules, reinforcing its position in automotive and industrial segments. Qorvo and Skyworks Solutions round out the core group by supplying integrated front‑end modules that combine power amplification, filtering, and beam‑steering capabilities, enabling tier‑1 equipment manufacturers to accelerate 6G prototype deployments. Collectively, these leaders shape a market structure where advanced material technology, design‑automation tools, and strategic OEM partnerships create high entry barriers for newcomers.

Beyond the primary tier, several niche yet strategically important players are expanding the competitive landscape. Broadcom is extending its RF front‑end line with silicon‑based millimeter‑wave solutions that complement GaN offerings. Analog Devices focuses on precision low‑noise amplifiers for back‑haul links, while Murata Manufacturing supplies compact RF modules for consumer‑grade devices. STMicroelectronics, Nexperia, and Renesas Electronics contribute specialty silicon‑based transceivers and power devices that address cost‑sensitive segments. MACOM and Qorvo’s spin‑off, Qorvo GaN, target ultra‑high‑frequency power amplification for test‑and‑measure equipment. Taiwan Semiconductor Manufacturing Company (TSMC) serves as a critical foundry partner, offering advanced process nodes for GaN and SiGe that enable rapid scaling of design cycles. These companies collectively enrich the ecosystem, fostering innovation and diversification across performance, cost, and application niches.

List of Key 6G RF Semiconductor Companies Profiled

- Qualcomm

- NXP Semiconductors

- Infineon Technologies

- Qorvo

- Skyworks Solutions

- Broadcom

- Analog Devices

- Murata Manufacturing

- STMicroelectronics

- Nexperia

- Renesas Electronics

- MACOM

- TSMC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Power Amplifiers

|

| By Application |

|

Mobile Backhaul

|

| By End User |

|

Telecom Operators

|

| By Frequency Band |

|

Terahertz

|

| By Integration Architecture |

|

Heterogeneous Integration

|

Regional Analysis: Asia-Pacific

China’s significant investments in 6G research and development, coupled with its ambitious plans for widespread 6G network deployment, are driving substantial demand for advanced RF semiconductors. The government’s emphasis on technological self-sufficiency is fostering innovation and supporting domestic manufacturers in this sector.

South Korea has established itself as a global leader in telecommunications technology and is actively involved in the development of 6G RF semiconductors. The country’s strong semiconductor manufacturing capabilities and collaborative ecosystem with leading technology companies position it as a key player in the regional market.

Japan is focusing on developing innovative RF semiconductor solutions for 6G applications, emphasizing miniaturization, energy efficiency, and high performance. The country’s strong research institutions and established electronics industry contribute to its competitive advantage in this space.

India presents a significant growth opportunity for 6G RF Semiconductor Market, driven by a large and expanding population, increasing data consumption, and government initiatives to enhance digital infrastructure. The country’s rising demand for affordable and high-speed connectivity is expected to fuel the adoption of 6G technologies and the associated semiconductor requirements.

North America

North America is expected to witness steady growth in 6G RF Semiconductor Market, fueled by investments in advanced wireless technologies and research activities. The region’s strong presence of leading semiconductor manufacturers and technology companies fosters innovation and drives the development of sophisticated RF solutions. While adoption may lag slightly behind Asia-Pacific, the demand for high-performance RF semiconductors in applications such as 5G, and early 6G trials will sustain market activity.

Europe

Europe is actively involved in the research and development of 6G technologies and RF semiconductors, with a focus on energy efficiency and sustainable solutions. Government initiatives and collaborations between industry and academia are supporting the growth of this sector. The European Union’s commitment to technological leadership positions the region as a key player in the development and deployment of 6G RF semiconductors.

South America

South America is in the early stages of exploring the potential of 6G RF Semiconductors. The region’s growing telecommunications infrastructure and increasing demand for high-speed data are expected to drive future growth. However, the market’s development will depend on investments in infrastructure upgrades and the availability of affordable 6G technologies.

Middle East & Africa

The Middle East and Africa represent a promising market for 6G RF Semiconductors, with increasing investments in telecommunications infrastructure and a growing demand for advanced wireless services. The region’s rapid urbanization and economic development are expected to fuel the adoption of 6G technologies and the associated semiconductor requirements.

Report Scope

This market research report provides a comprehensive analysis of the 6G RF Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 6G RF Semiconductor Market?

-> 6G RF Semiconductor Market was valued at USD 0.92 billion in 2025 and is expected to reach USD 3.21 billion by 2034, growing at a CAGR of 12% during the forecast period.

Which key companies operate in 6G RF Semiconductor Market?

-> Key players include Qualcomm, NXP Semiconductors, Infineon Technologies, Qorvo, and Skyworks Solutions, among others.

What are the key growth drivers?

-> Key growth drivers include heavy telecom investment in terahertz research, accelerated development of high‑performance mmWave modules, and strategic governmental funding programs in Asia and Europe.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains the largest market by revenue.

What are the emerging trends?

-> Emerging trends include GaN‑based power amplifiers, AI‑optimized semiconductor design tools, and integration of AI/ML for adaptive RF performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...