6G RF Front-End Market Insights

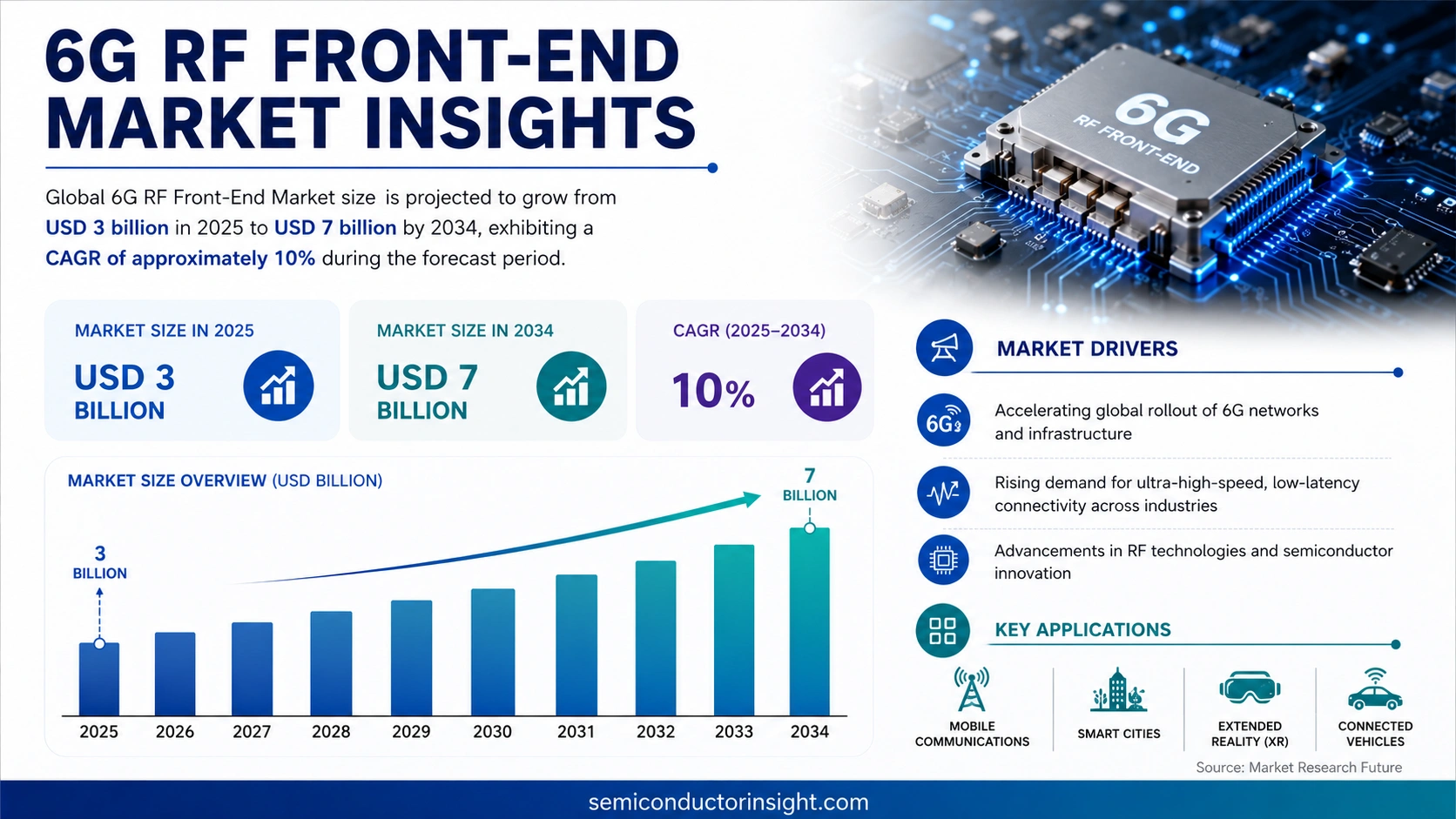

Global 6G RF Front‑End Market size was valued at USD 3 billion in 2025. The market is projected to grow from USD 3 billion in 2025 to USD 7 billion by 2034, exhibiting a CAGR of approximately 10% during the forecast period.

6G RF front‑end comprises critical components such as power amplifiers, low‑noise amplifiers, duplexers, switches and filters that enable transmission and reception of ultra‑high‑frequency signals required for next‑generation mobile networks operating above 100 GHz.

The market is accelerating because telecom operators are investing heavily in dense small‑cell deployments and AI‑driven services that demand higher bandwidth and lower latency; however, challenges remain around thermal management and integration complexity. Furthermore, advances in silicon‑based MMIC technology are reducing costs while key players,including Qualcomm Technologies Inc., Qorvo Inc., Skyworks Solutions Inc., and NXP Semiconductors,are forming strategic partnerships to fast‑track commercial rollouts of 6G front‑end solutions.

MARKET DRIVERS

Emerging 6G Use Cases

Rollout of 6G services is expected to unlock ultra‑high‑capacity applications such as holographic telepresence, tactile internet, and massive machine‑type communications. These scenarios demand front‑end modules that can operate across wider frequency bands while maintaining linearity and low noise, directly fueling growth in 6G RF Front-End Market.

Advances in Semiconductor Technology

Breakthroughs in silicon‑based MMICs and compound semiconductor processes are reducing power consumption and improving integration density. Manufacturers can now embed multiple front‑end functions on a single chip, lowering bill‑of‑materials and accelerating time‑to‑market for 6G devices.

➤ “By 2030, front‑end solutions will account for over 35% of total 6G device cost, making efficiency gains a decisive competitive factor.”

In parallel, the rise of edge‑computing architectures is encouraging modular designs that can be upgraded as new spectrum allocations become available, reinforcing the long‑term attractiveness of the market.

MARKET CHALLENGES

Regulatory and Spectrum Allocation

Global regulators are still defining the exact frequency blocks for 6G, leading to uncertainty for designers who must accommodate multiple potential bands. This regulatory lag can delay product launches and increase R&D expenditure.

Other Challenges

Technology Integration

Integrating high‑gain antennas, beamforming networks, and power‑amplifier arrays in a compact form factor poses thermal management and reliability hurdles, especially for handheld and IoT devices.

MARKET RESTRAINTS

High Development Costs

Designing front‑end solutions that meet the stringent performance metrics of 6G requires multi‑disciplinary expertise and expensive prototyping facilities, which can deter smaller players.

Additionally, the need for extensive validation across diverse climate and usage scenarios inflates testing budgets, limiting rapid iteration cycles.

Finally, supply‑chain constraints for high‑purity substrate materials further elevate component pricing, slowing broader market adoption.

MARKET OPPORTUNITIES

Integration with AI‑Driven Networks

AI algorithms that dynamically reconfigure RF parameters can extract additional efficiency from front‑end hardware, creating a niche for adaptive modules that respond to real‑time traffic patterns.

Moreover, emerging use cases in autonomous transport and smart cities require resilient, low‑latency connectivity, positioning advanced 6G front‑end designs as critical enablers for future infrastructure.

Strategic partnerships between semiconductor foundries and telecom OEMs are also opening co‑development programs that lower entry barriers and accelerate time‑to‑revenue for innovative solutions.

6G RF Front-End Market Trends

Increasing Small‑Cell Density and AI‑Driven Services

Telecom operators are accelerating investments in ultra‑dense small‑cell deployments to meet the capacity demands of next‑generation mobile networks. The shift toward AI‑enabled services requires higher bandwidth, lower latency, and more reliable front‑end performance, prompting a rapid redesign of power amplifiers, low‑noise amplifiers, duplexers, switches and filters. As spectrum moves above 100 GHz, manufacturers are focusing on thermal efficiency and integration simplicity to sustain operational stability. These pressures are reshaping 6G RF Front-End Market, driving a competitive landscape where speed of rollout and component reliability become decisive factors for service providers seeking to differentiate their offerings.

Other Trends

Advances in Silicon MMIC Technology

Silicon‑based monolithic microwave integrated circuit (MMIC) technology is gaining traction as a cost‑effective alternative to compound semiconductor solutions. Recent process improvements have lowered insertion loss and increased power density, enabling more compact front‑end modules that align with the space constraints of handheld and edge‑computing devices. The reduction in material costs, combined with improved yield rates, allows manufacturers to price solutions more competitively while maintaining the performance required for high‑frequency operation. This technical progression supports broader adoption across the ecosystem and reinforces the strategic importance of silicon MMICs within the overall market evolution.

Strategic Partnerships Accelerating Commercial Rollout

Key industry players such as Qualcomm Technologies, Qorvo, Skyworks Solutions and NXP Semiconductors are forming strategic alliances to fast‑track the commercialization of next‑generation front‑end components. Collaborative R&D programs focus on co‑optimizing device architectures, sharing intellectual property, and aligning product roadmaps with operator timelines. These partnerships reduce time‑to‑market and mitigate integration risks by pooling expertise across the supply chain. Consequently, 6G RF Front-End Market is witnessing a more coordinated rollout strategy that blends advanced silicon technologies with proven system design practices, fostering a robust pipeline of ready‑to‑deploy solutions for the upcoming decade.

COMPETITIVE LANDSCAPE

Key Industry Players

6G RF Front‑End Market Competitive Overview

6G RF front‑end segment is currently anchored by a small cohort of technology powerhouses that command the majority of design wins and volume production. Qualcomm Technologies Inc., Qorvo Inc., Skyworks Solutions Inc., and NXP Semiconductors dominate the high‑frequency power‑amplifier, low‑noise amplifier, and duplexer portfolios, leveraging advanced silicon‑based MMIC processes to meet the sub‑millimeter‑wave specifications above 100 GHz. Their strategic alliances with major telecom operators and foundry partners accelerate integration of AI‑driven antenna modules, enabling the projected market expansion from USD 3 billion in 2025 to USD 7 billion by 2034. These incumbents benefit from extensive IP libraries, robust supply‑chain networks, and deep R&D investments that create high entry barriers for new entrants.

Beyond the tier‑one giants, a diverse set of niche innovators and diversified semiconductor firms are expanding the competitive landscape. Broadcom Inc., Murata Manufacturing Co., Ltd., Analog Devices, Inc., and STMicroelectronics N.V. focus on specialized filters, switches, and reconfigurable antennas that address thermal‑management and integration challenges. Infineon Technologies AG and Renesas Electronics Corporation contribute silicon‑carbide and gallium‑nitride solutions aimed at power‑efficient amplification. MediaTek Inc. and Samsung Electronics Co., Ltd. are leveraging their mobile chipset expertise to develop integrated front‑end modules for dense small‑cell deployments. Intel Corporation and Taiwan Semiconductor Manufacturing Company (TSMC) provide cutting‑edge foundry services that underpin the fabrication of next‑generation RF MMICs, further democratizing access to 6G front‑end capabilities.

List of Key 6G RF Front‑End Companies Profiled

- Qualcomm Technologies Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- NXP Semiconductors

- Broadcom Inc.

- Murata Manufacturing Co., Ltd.

- Analog Devices, Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Renesas Electronics Corporation

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Power Amplifier Modules are pivotal for delivering the high output power required at millimeter‑wave frequencies. – Enable compact, high‑gain front‑end architectures that support ultra‑high data rates. – Drive system‑level efficiency improvements by reducing loss pathways. – Align with silicon‑based MMIC advances, simplifying integration across devices. |

| By Application |

|

Immersive XR Experiences demand extremely low latency and massive bandwidth, shaping front‑end design priorities. – Pushes developers toward highly linear amplifiers that maintain signal fidelity. – Necessitates reconfigurable filters to adapt to varying spectrum allocations. – Encourages integration of AI‑assisted calibration to manage thermal constraints. |

| By End User |

|

Telecom Service Providers are the primary force steering market direction. – Their rollout of dense small‑cell networks fuels demand for highly integrated front‑ends. – Strategic partnerships with semiconductor leaders accelerate technology standardization. – Emphasis on thermal management solutions to maintain reliability in continuous‑operation environments. |

| By Technology |

|

Silicon‑Based MMIC is reshaping cost structures while preserving performance. – Enables mass‑production of broadband amplifiers with consistent quality. – Facilitates tighter integration with digital control logic, reducing board space. – Supports co‑design approaches that address thermal and linearity challenges early in the design cycle. |

| By Deployment Scenario |

|

Urban Small‑Cell Grids create the most intensive design pressures. – Require front‑ends that operate efficiently across a broad frequency span to support dense bandwidth reuse. – Promote modular solutions that can be quickly deployed and upgraded. – Drive adoption of advanced thermal‑dissipation materials to sustain performance under high traffic loads. |

Regional Analysis: North America

United States

The development and deployment of advanced antenna systems are critical for realizing the full potential of 6G RF Front-End technology. This includes massive MIMO and beamforming capabilities to support higher data rates and improved spectral efficiency.

Millimeter-wave (mmWave) frequencies are expected to play a significant role in 6G RF Front-End systems, offering vast amounts of spectrum for high-bandwidth applications. Challenges remain in terms of signal propagation and device design.

Intelligent reflecting surfaces (IRS) are an emerging technology that can dynamically shape radio waves, enhancing coverage and capacity in 6G networks. They represent a significant innovation in RF Front-End architecture.

The integration of network virtualization and cloudification with 6G RF Front-End systems will be crucial for enabling flexible and scalable network deployments, optimizing resource utilization, and reducing operational costs.

Europe

Europe is anticipated to witness steady growth in 6G RF Front-End Market, driven by strong government support for technological advancement and a focus on developing innovative communication solutions. The region’s emphasis on sustainable technologies aligns well with the energy efficiency requirements of next-generation RF Front-End components. Key market trends include a focus on private 6G networks for industrial applications and the development of advanced semiconductor materials. Business strategies in Europe involve collaborations between research institutions, telecom operators, and equipment manufacturers to accelerate 6G technology development and adoption. 6G RF Front-End market in Europe will also be shaped by the evolving regulatory landscape concerning spectrum allocation and data privacy.

Asia-Pacific

Asia-Pacific represents a significant growth opportunity for 6G RF Front-End Market, primarily driven by rapid urbanization, increasing mobile data consumption, and government initiatives to lead in next-generation communication technologies. Countries like China, Japan, and South Korea are heavily investing in 6G research and development, creating a competitive landscape for RF Front-End solution providers. The focus in this region is on developing cost-effective and energy-efficient RF Front-End components for mass deployment. Business strategies in Asia-Pacific emphasize building strong supply chains and fostering partnerships with local manufacturers to cater to the region’s unique requirements.

South America

South America is expected to experience moderate growth in 6G RF Front-End Market, spurred by increasing internet penetration and the expanding adoption of mobile broadband services. The region’s telecommunications infrastructure is undergoing modernization, creating demand for advanced RF Front-End solutions. Key trends include a focus on improving network coverage in underserved areas and the deployment of 6G-enabled private networks for various industrial sectors. Business strategies in South America emphasize providing tailored solutions to address specific regional challenges and building long-term relationships with telecom operators.

Middle East & Africa

The Middle East & Africa region presents a promising market for 6G RF Front-End Market, driven by rapid economic growth, increasing disposable incomes, and a growing demand for advanced communication services. Governments in the region are investing in infrastructure development to support 6G deployments. Key trends include a focus on deploying 6G networks for smart city initiatives and supporting the growth of e-commerce and digital services. Business strategies in this region emphasize cost-effective solutions and partnerships with local stakeholders to navigate the diverse regulatory and economic landscapes.

Report Scope

This market research report provides a comprehensive analysis of the 6G RF Front-End Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 6G RF Front-End Market?

-> 6G RF Front-End Market was valued at USD 3 billion in 2025 and is expected to reach USD 7 billion by 2034, representing a CAGR of approximately 10% over the forecast period.

Which key companies operate in 6G RF Front-End Market?

-> Key players include Qualcomm Technologies Inc., Qorvo Inc., Skyworks Solutions Inc., and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include dense small‑cell deployments, AI‑driven services, increased bandwidth demand, and advancements in silicon‑based MMIC technology.

Which region dominates the market?

-> Asia-Pacific is emerging as a fast‑growing region due to strong telecom infrastructure investments, while North America and Europe remain significant markets.

What are the emerging trends?

-> Emerging trends include integration of AI/IoT with RF front‑end modules, development of ultra‑high‑frequency components above 100 GHz, and cost‑reduction through silicon‑based MMICs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...