MARKET INSIGHTS

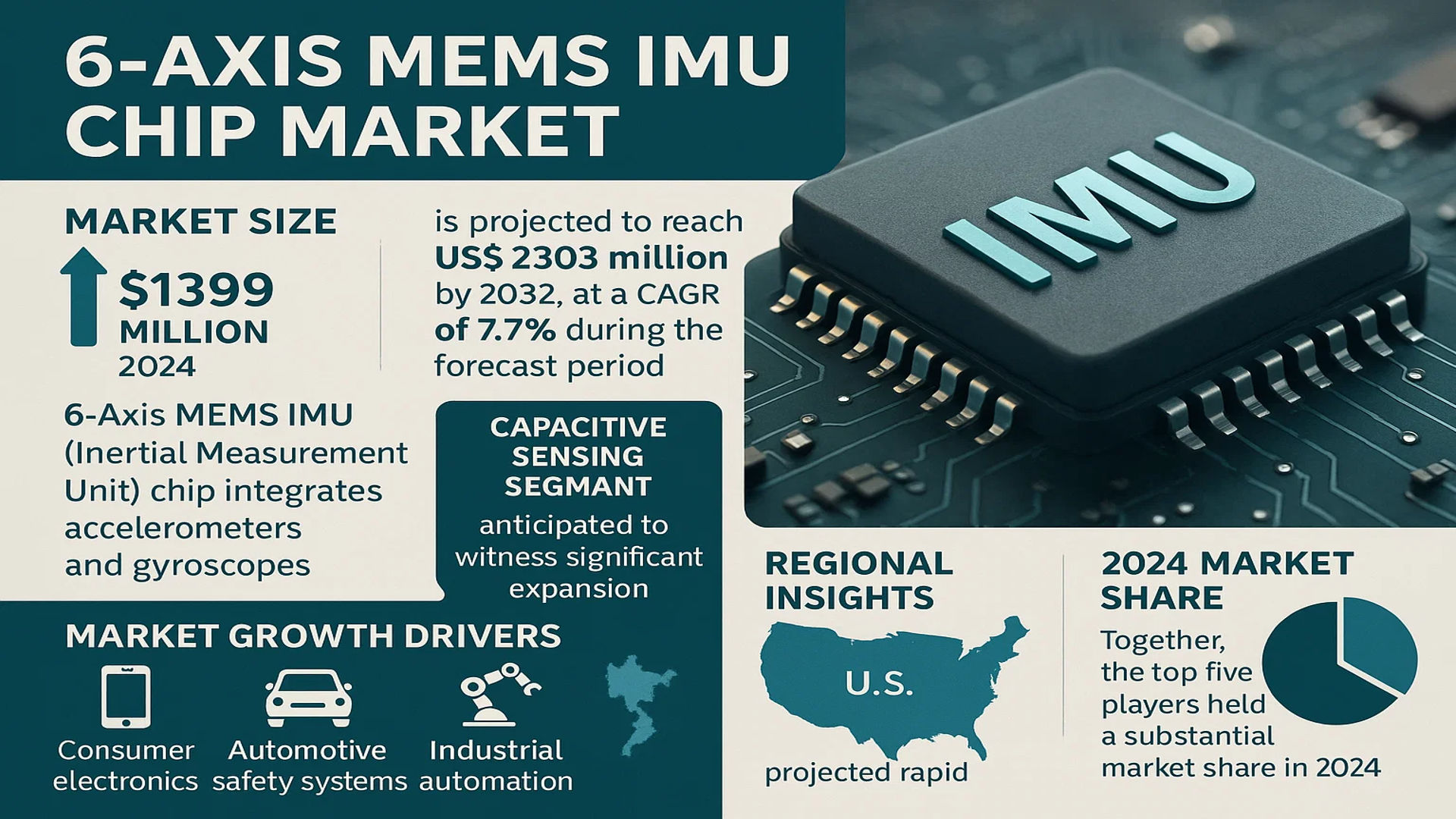

The global 6-Axis MEMS IMU Chip market was valued at 1399 million in 2024 and is projected to reach US$ 2303 million by 2032, at a CAGR of 7.7% during the forecast period.

A 6-Axis MEMS IMU (Inertial Measurement Unit) chip is a microelectromechanical systems (MEMS) device that integrates accelerometers and gyroscopes to measure both linear acceleration and angular velocity along three orthogonal axes each. This enables precise motion tracking and orientation detection, making it indispensable in applications requiring real-time spatial awareness.

The market growth is driven by increasing adoption in consumer electronics, automotive safety systems, and industrial automation. The capacitive sensing segment, known for its high precision, is anticipated to witness significant expansion. Geographically, China’s market is projected to grow rapidly due to local manufacturing advancements, while the U.S. remains a key innovator with companies like Bosch and STMicroelectronics leading R&D efforts. Together, the top five players held a substantial market share in 2024, underscoring the industry’s consolidated nature.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT and Smart Devices to Accelerate Demand for 6-Axis MEMS IMU Chips

The rapid adoption of Internet of Things (IoT) applications and smart consumer electronics has significantly amplified the need for compact, high-precision motion sensors. The 6-axis MEMS IMU chip, combining accelerometers and gyroscopes, is pivotal in enabling advanced functionalities such as gesture recognition, navigation, and stabilization in devices ranging from wearables to industrial robots. With IoT connections projected to exceed 29 billion globally by 2030, manufacturers increasingly integrate these chips to enhance efficiency in automation and real-time data processing. Leading smartphone brands have already incorporated 6-axis IMUs in over 80% of flagship models for augmented reality (AR) and gaming applications.

Advancements in Autonomous Vehicle Technology Fuel Adoption

Autonomous vehicles demand absolute accuracy in motion tracking, making 6-axis MEMS IMUs indispensable for inertial navigation systems. These chips provide critical data for vehicle stability control, rollover detection, and dead reckoning in GPS-denied environments. The automotive sector accounts for nearly 30% of current IMU demand, with Level 4 autonomous vehicles requiring multiple high-performance units per vehicle. Recent developments in AI-driven sensor fusion further optimize IMU outputs by compensating for drift errors, thereby elevating reliability. Regulatory mandates for electronic stability control (ESC) across North America and Europe continue to solidify this growth trajectory.

Robotics and Industry 4.0 Deployments Propel Market Expansion

Industrial automation relies heavily on 6-axis IMUs for robotic arm positioning, drone stabilization, and predictive maintenance in manufacturing lines. The rise of collaborative robots (cobots) necessitates miniaturized sensors capable of sub-degree tilt measurement accuracy. Warehouse automation alone is estimated to deploy over 1.2 million IMU-equipped mobile robots annually by 2026. Meanwhile, digital twin technologies in Industry 4.0 leverage these chips to synchronize physical and virtual environments with real-time motion data. Such diversification across sectors ensures sustained demand growth.

➤ For instance, in Q2 2024, STMicroelectronics unveiled a next-gen 6-axis IMU with 40% lower power consumption—directly addressing energy efficiency needs in battery-operated industrial IoT devices.

MARKET RESTRAINTS

High Production Costs and Complex Calibration Requirements Curtail Profit Margins

While MEMS technology enables mass production, 6-axis IMUs face cost pressures from intricate calibration processes needed to minimize cross-axis interference. Temperature compensation algorithms and factory-tuning procedures add 15-20% to unit costs—making them prohibitive for price-sensitive applications. Automotive-grade IMUs must endure rigorous reliability testing, further inflating R&D expenditures. Although wafer-level packaging has reduced sizes, achieving sub-10nm alignment tolerances between gyroscopic and accelerometric components remains a yield-limiting challenge for foundries.

Competition from Alternative Sensor Technologies Impedes Market Penetration

Emerging optical-based inertial sensors threaten to displace MEMS IMUs in high-end applications where precision outweighs cost considerations. Fiber-optic gyroscopes (FOGs) already dominate aerospace applications due to their 0.01°/hr bias stability—far surpassing MEMS capabilities. Meanwhile, consumer electronics manufacturers increasingly adopt redundant 9-axis systems (combining IMUs with magnetometers), eroding standalone 6-axis chip demand. Such alternatives compel MEMS suppliers to accelerate innovation cycles while maintaining aggressive pricing—a balancing act challenging for mid-tier players.

Other Constraints

Supply Chain Vulnerabilities

Geopolitical tensions have exposed dependencies on specialized semiconductor materials like silicon-on-insulator (SOI) wafers, with single-source suppliers causing bottleneck risks.

Regulatory Compliance

Evolving standards for automotive functional safety (ISO 26262) and industrial certifications require continuous design iterations, delaying time-to-market for new IMU variants.

MARKET OPPORTUNITIES

Healthcare Wearables and Surgical Robotics Present Untapped Potential

The medical sector represents a high-growth niche for 6-axis MEMS IMUs, particularly in surgical navigation systems requiring sub-millimeter tool tracking accuracy. Recent trials have demonstrated IMU-assisted orthopedic procedures reducing operation times by 25%. Concurrently, next-gen wearable ECG patches integrate motion sensors to filter out noise during patient movement—a market poised to exceed $12 billion by 2028. Startups specializing in fall-detection elderly care devices further amplify demand. Strategic partnerships between MEMS manufacturers and MedTech firms could unlock this potential.

Military Modernization Programs Drive Ruggedized IMU Development

Defense agencies globally are prioritizing MEMS-based inertial systems for guided munitions and unmanned platforms where GPS jamming resistance is critical. The U.S. Department of Defense’s investment in micro-PNT (Positioning, Navigation, Timing) technologies alone exceeds $500 million annually. These applications demand IMUs with MIL-STD-810 shock/vibration tolerance—a specification few commercial chips presently meet. Suppliers developing radiation-hardened variants stand to capture long-term contracts in this high-margin segment.

MARKET CHALLENGES

Thermal Drift and Long-Term Stability Issues Persist in Miniaturized Designs

While MEMS scaling enables smaller form factors, thermal sensitivity remains a fundamental limitation for 6-axis IMUs. Coefficient variances between integrated accelerometers and gyroscopes introduce measurement errors exceeding 5% across operating temperature ranges—unacceptable for aerospace/defense applications. Advanced compensation techniques leveraging on-chip heaters or AI algorithms add cost and power overheads. Chronic bias instability also plagues consumer-grade IMUs, with typical specifications allowing 1-2° orientation drift per hour—problematic for extended AR/VR sessions.

Other Challenges

Data Fusion Complexity

Integrating IMU outputs with other sensors (LiDAR, cameras) necessitates sophisticated sensor fusion algorithms, often requiring proprietary IP that smaller manufacturers lack.

Cybersecurity Risks

Connected IMUs in autonomous systems create attack vectors for spoofing inertial data—a vulnerability recently demonstrated in academic studies on drone hijacking.

6-AXIS MEMS IMU CHIP MARKET TRENDS

Miniaturization and IoT Integration Drive Market Expansion

The rapid advancements in miniaturization techniques and the proliferation of IoT devices are significantly accelerating the adoption of 6-axis MEMS IMU chips globally. By 2032, the market is projected to exceed $2.3 billion, growing at a CAGR of 7.7% from 2024. These chips, which integrate accelerometers and gyroscopes into a compact form factor, are critical for applications requiring precise motion tracking, such as drones, wearables, and augmented reality (AR) devices. Emerging technologies like 5G connectivity and edge computing are further enhancing their utility, enabling real-time data processing with lower latency.

Other Trends

Automotive Navigation and ADAS

The automotive sector is witnessing heightened demand for 6-axis MEMS IMU chips due to their role in advanced driver-assistance systems (ADAS) and autonomous vehicle navigation. These chips provide accurate orientation and motion data, essential for functions like electronic stability control (ESC) and lane-keeping assist. With automakers worldwide focusing on safety regulations and autonomous driving capabilities, the integration of MEMS IMUs in vehicles is expected to grow substantially. Europe and North America, with their stringent vehicle safety norms, are leading this adoption.

Consumer Electronics and Wearable Technology Boom

The surge in wearable devices, including smartwatches and fitness trackers, is another key driver for the 6-axis MEMS IMU chip market. These chips enable activity tracking, gesture recognition, and fall detection, which are critical features for health and wellness applications. The global consumer electronics segment accounted for over 45% of the market share in 2024, with continued growth expected due to increasing consumer demand for smart, connected devices. Innovations in low-power consumption designs are further broadening their application scope in battery-operated wearables.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in the 6-Axis MEMS IMU Chip Market

The global 6-Axis MEMS IMU Chip market is moderately consolidated, dominated by established semiconductor and sensor manufacturers with strong technological capabilities. Bosch Sensortec and STMicroelectronics lead the industry, collectively accounting for a substantial market share. Their dominance stems from extensive R&D investments, broad patent portfolios, and strategic partnerships with key end-users in automotive and consumer electronics.

TDK (InvenSense) and Murata have strengthened their positions through acquisitions and vertical integration strategies. These players excel in high-performance industrial-grade IMUs, capturing demand from robotics and aerospace applications. Meanwhile, Asian manufacturers like Silan Microelectronics and Senodia Technologies are gaining traction by offering cost-competitive solutions for mass-market consumer devices.

The competitive intensity is increasing as companies expand their MEMS foundry capacity and develop next-generation IMUs with improved power efficiency and sensor fusion capabilities. With the market projected to grow at 7.7% CAGR through 2032, manufacturers are differentiating through:

- Miniaturization breakthroughs for wearables and IoT devices

- Enhanced accuracy for autonomous vehicle navigation systems

- AI-accelerated sensor fusion algorithms

Recent developments include STMicroelectronics’ launch of automotive-qualified IMUs with ASIL-B compliance and Bosch’s new IMU series featuring integrated machine learning cores. These innovations reflect the industry’s shift toward smarter, application-specific solutions.

List of Leading 6-Axis MEMS IMU Chip Manufacturers

- Bosch Sensortec GmbH (Germany)

- STMicroelectronics (Switzerland)

- TDK Corporation (Japan) – InvenSense Division

- Murata Manufacturing Co., Ltd. (Japan)

- Panasonic Corporation (Japan)

- Senodia Technologies (China)

- QST Corporation (U.S.)

- Silan Microelectronics (China)

- Analog Devices, Inc. (U.S.)

Segment Analysis:

By Technology

Capacitive Technology Dominates the Market Due to High Precision and Low Power Consumption

The market is segmented based on technology into:

- Capacitive

- Piezoelectric

- Others

By Application

Consumer Electronics Segment Leads Owing to Increasing Adoption in Smartphones and Wearables

The market is segmented based on application into:

- Consumer Electronics

- Smartphones

- Wearables

- Gaming Devices

- Others

- Automotive

- Industrial

- Aerospace & Defense

- Others

By Sensing Range

Standard Range Segment Represents Majority Share Due to Wide Application in General Purpose Devices

The market is segmented based on sensing range into:

- Standard Range

- High Range

- Ultra-High Range

By Price Range

Mid-Range IMUs Account for Significant Market Penetration

The market is segmented based on price range into:

- Economy

- Mid-Range

- Premium

Regional Analysis: 6-Axis MEMS IMU Chip Market

Asia-Pacific

The Asia-Pacific region dominates the 6-Axis MEMS IMU Chip market, driven by rapid technological adoption in consumer electronics and automotive applications. China leads the charge, with its robust semiconductor manufacturing ecosystem and government support for IoT and automation technologies. Major players like Panasonic, TDK, and Silan Microelectronics have established strong production bases here. Japan and South Korea follow closely, leveraging their advanced automotive and robotics industries to drive demand for high-precision motion sensing solutions. The region benefits from cost-effective manufacturing capabilities and a growing middle class that fuels demand for smart devices, though intellectual property protection remains a concern.

North America

North America represents the innovation hub for MEMS technology, with Silicon Valley startups and established players like Bosch Sensortec driving cutting-edge developments. The U.S. market benefits from strong defense and aerospace applications, where 6-Axis IMU chips are critical for navigation systems. Consumer electronics and wearable technology companies continue to push for smaller, more power-efficient designs. Canada’s growing industrial automation sector presents new opportunities, while Mexico serves as a manufacturing base for automotive-grade IMUs. The region faces challenges from supply chain dependencies but maintains leadership in research and high-value applications.

Europe

Europe’s market is characterized by stringent quality requirements and strong automotive OEM demand, particularly from Germany’s premium vehicle manufacturers. STMicroelectronics leads regional production with its automotive-qualified IMU solutions. The EU’s focus on industrial automation and smart manufacturing under Industry 4.0 initiatives creates sustained demand. While environmental regulations increase production costs, they also drive innovation in energy-efficient designs. The region faces growing competition from Asian manufacturers but maintains superiority in precision engineering for medical and aerospace applications where reliability is paramount.

Middle East & Africa

The MEA region shows emerging potential, particularly in Israel’s thriving tech startup ecosystem and the UAE’s smart city projects. Defense applications drive premium IMU demand in key markets, while oil & gas infrastructure monitoring presents niche opportunities. Limited local manufacturing capabilities result in reliance on imports, though regional players are beginning to establish assembly operations. Infrastructure challenges and lower technology penetration in some markets constrain growth, but long-term potential exists as regional economies diversify beyond traditional sectors.

South America

South America’s market remains in early development stages, with Brazil and Argentina showing the most activity. Automotive production and agricultural equipment manufacturing generate steady demand, though economic instability often disrupts supply chains. The lack of local semiconductor fabrication limits value addition, with most chips being imported from Asia or North America. While smartphone adoption drives some consumer-level demand, industrial applications remain limited by inconsistent investment in automation technologies. The region could see accelerated growth with improved economic conditions and technology transfer agreements.

Report Scope

This market research report provides a comprehensive analysis of the global 6-Axis MEMS IMU Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global 6-Axis MEMS IMU Chip market was valued at USD 1,399 million in 2024 and is projected to reach USD 2,303 million by 2032, growing at a CAGR of 7.7% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (capacitive and others), application (consumer electronics, automotive, industrial, and others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets, with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global 6-Axis MEMS IMU Chip Market?

-> 6-Axis MEMS IMU Chip market was valued at 1399 million in 2024 and is projected to reach US$ 2303 million by 2032, at a CAGR of 7.7% during the forecast period.

Which key companies operate in the Global 6-Axis MEMS IMU Chip Market?

-> Key players include Bosch, STMicroelectronics, Panasonic, TDK, Murata, Senodia, QST Corporation, and Silan Microelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for consumer electronics, advancements in automotive safety systems, and increasing adoption of industrial automation.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China and Japan, while North America remains a dominant market due to technological advancements.

What are the emerging trends?

-> Emerging trends include miniaturization of MEMS devices, integration with AI/ML for enhanced functionality, and increasing demand for high-precision IMUs in drones and robotics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...