5G Dielectrics Market Insights

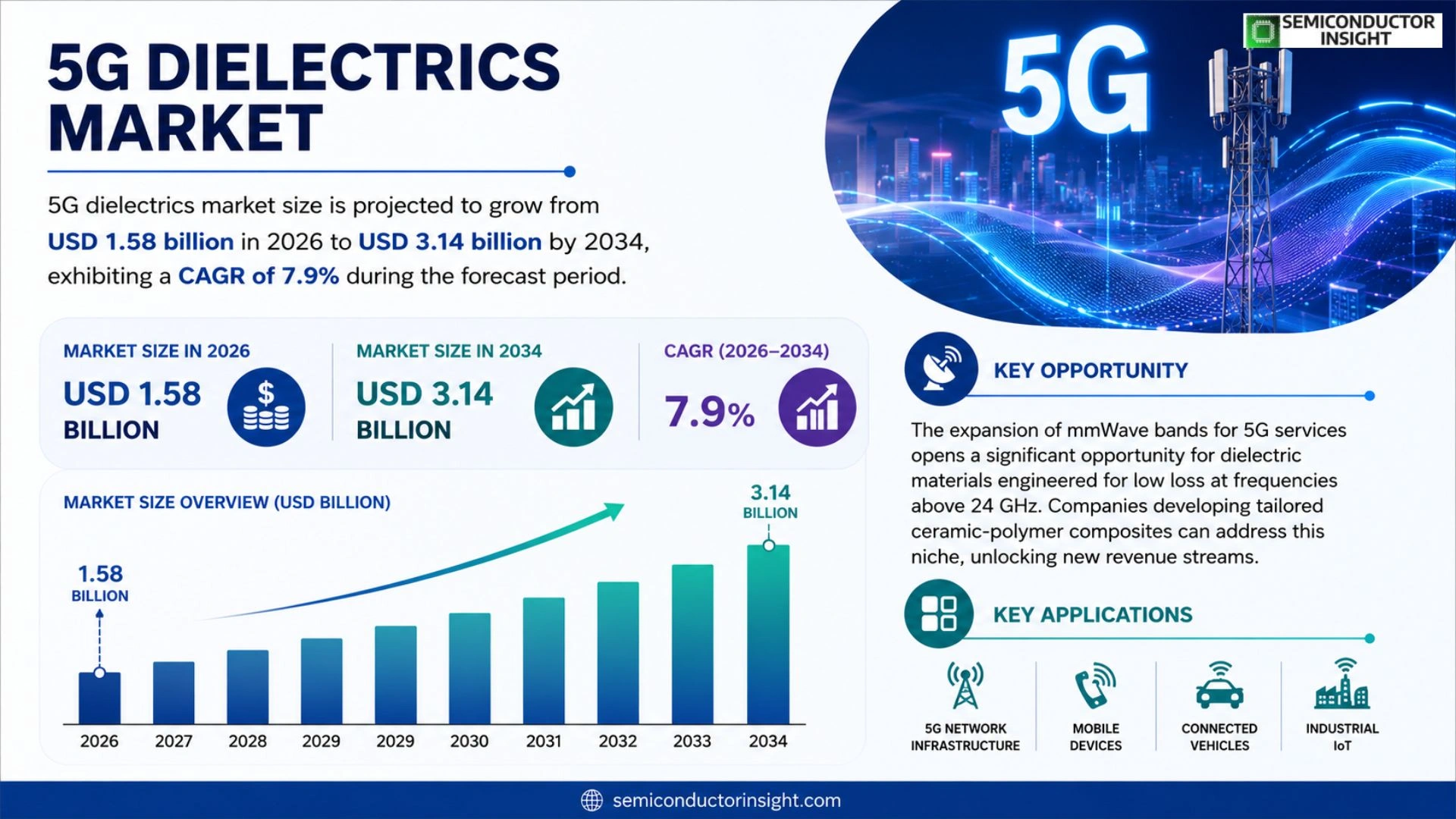

Global 5G Dielectrics market size was valued at USD 1.48 billion in 2025. The market is projected to grow from USD 1.58 billion in 2026 to USD 3.14 billion by 2034, exhibiting a CAGR of 7.9% during the forecast period.

5G dielectrics are high‑performance insulating materials used in antenna substrates, RF filters, and printed circuit boards that enable low‑loss transmission of millimeter‑wave signals essential for next‑generation mobile networks.

The market is experiencing rapid expansion because telecom operators worldwide are accelerating 5G network rollouts, which drives demand for low‑loss dielectric substrates capable of supporting higher frequencies up to 100 GHz. Furthermore, advancements in material science,such as low‑temperature co‑fire ceramics and polymer composites,are reducing production costs while improving thermal stability. Key players including Rogers Corporation, TDK Corporation, and Murata Manufacturing are investing heavily in R&D and forming strategic partnerships to capture emerging opportunities.

MARKET DRIVERS

Rising Mobile Data Consumption

5G Dielectrics Market is being propelled by exponential growth in mobile data traffic, with global traffic projected to exceed 200 EB per month by 2028. This surge demands materials that can sustain higher frequencies while minimizing signal loss, positioning advanced dielectric compounds as essential components in next‑generation base stations.

Advances in Antenna Miniaturization

Innovations in antenna design, especially for compact massive MIMO arrays, require dielectric substrates with low permittivity and high thermal stability. Manufacturers are therefore investing heavily in research to develop polymers that meet these specifications, directly fuelling demand for specialized 5G dielectric solutions.

➤ Industry analysts estimate a compound annual growth rate of roughly 12 % for dielectric materials tailored to 5G applications through 2027.

Overall, the convergence of higher bandwidth requirements and tighter integration constraints creates a robust growth engine for 5G Dielectrics Market, encouraging sustained capital allocation across the supply chain.

MARKET CHALLENGES

Manufacturing Complexity and Yield Management

Producing high‑purity dielectric films at the nanometer scale involves sophisticated deposition techniques such as atomic layer deposition (ALD) and chemical vapor deposition (CVD). These processes are capital‑intensive and sensitive to contaminant levels, leading to lower yields and higher unit costs.

Other Challenges

Supply Chain Constraints

Critical raw materials like high‑frequency polymers and rare‑earth oxides face limited global availability, creating bottlenecks that can delay product launches and increase pricing pressure.

Moreover, stringent environmental regulations in major manufacturing hubs impose additional compliance costs, further complicating the scaling of production for 5G Dielectrics Market.

MARKET RESTRAINTS

Cost Sensitivity in Telecom Deployments

Telecom operators are under pressure to contain capital expenditures while rolling out dense 5G networks. The premium pricing of high‑performance dielectrics can deter adoption, especially in price‑sensitive emerging markets.

In addition, the rapid evolution of competing technologies such as photonic interconnects may divert investment away from traditional dielectric solutions, creating a strategic restraint for manufacturers.

Consequently, firms that can balance performance with cost efficiency are better positioned to mitigate these market restraints and capture share.

MARKET OPPORTUNITIES

Growth in Millimeter‑Wave (mmWave) Deployments

The expansion of mmWave bands for 5G services opens a significant opportunity for dielectric materials engineered for low loss at frequencies above 24 GHz. Companies developing tailored ceramic‑polymer composites can address this niche, unlocking new revenue streams.

Furthermore, the rise of edge computing and private 5G networks in industrial settings creates demand for rugged, temperature‑stable dielectrics that can operate reliably in harsh environments.

By leveraging these emerging application corridors, 5G Dielectrics Market can achieve differentiated growth beyond traditional macro‑cell deployments.

5G Dielectrics Market Trends

Rapid Expansion of Low‑Loss Dielectric Substrates

The ongoing rollout of next‑generation mobile networks is driving a pronounced surge in demand for low‑loss dielectric substrates that can operate reliably at millimeter‑wave frequencies up to 100 GHz. Telecom operators are prioritizing components that minimize signal attenuation, and this requirement directly fuels the expansion of 5G Dielectrics Market. Manufacturers are responding by scaling production of high‑performance insulating materials used in antenna substrates, RF filters, and printed circuit boards. The shift toward higher frequency bands has elevated the importance of material purity and dielectric‑constant stability, prompting suppliers to adopt tighter quality controls and advanced testing protocols. As a result, the overall market trajectory reflects a rapid increase in volume shipments while maintaining stringent performance specifications.

Other Trends

Material Innovation and Cost Efficiency

Advancements in material science are reshaping cost structures and thermal performance across 5G Dielectrics Market. Low‑temperature co‑fire ceramic processes enable thinner substrates with reduced shrinkage, while polymer‑based composites deliver comparable dielectric loss tangents with lighter weight and lower manufacturing temperatures. These innovations improve thermal stability, extend device lifespans, and lower the capital outlay for fabs. Consequently, producers can offer competitive pricing without compromising the low‑loss characteristics essential for millimeter‑wave signal integrity, broadening the adoption base beyond flagship devices to mid‑range infrastructure equipment.

Strategic Partnerships and R&D Investment

Key players such as Rogers Corporation, TDK Corporation, and Murata Manufacturing are intensifying R&D expenditures and forming strategic alliances to capture emerging opportunities 5G Dielectrics Market. Collaborative efforts focus on co‑development of next‑generation polymer‑ceramic hybrids, joint validation of high‑frequency test platforms, and shared intellectual‑property frameworks that accelerate time‑to‑market. These partnerships not only spread development risk but also create standardized material specifications that simplify integration for equipment manufacturers. The cumulative effect is a more cohesive supply chain that can meet the accelerating rollout schedules set by telecom operators worldwide.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics in the Global 5G Dielectrics Market

5G Dielectrics Market, valued at USD 1.48 billion in 2025 and projected to reach USD 3.14 billion by 2034 with a CAGR of 7.9%, is dominated by a handful of technology‑focused manufacturers. Rogers Corporation leads the segment through its advanced low‑temperature co‑fire ceramic substrates that deliver loss tangents below 0.001 at frequencies up to 100 GHz. Rogers’ extensive R&D pipeline, coupled with strategic alliances with major telecom equipment makers, secures a premium market share and sets performance benchmarks for antenna substrates and millimeter‑wave filters. TDK Corporation follows closely, leveraging its polymer‑ceramic hybrid portfolio to address cost‑sensitive mass‑market deployments while maintaining thermal stability. Murata Manufacturing complements this tier with high‑Q ceramic resonators and multilayer substrates, reinforcing the concentration of market power among a few innovators who can meet the stringent loss and thermal requirements of next‑generation networks.

Beyond the top three, a diverse set of niche players enriches the competitive landscape. Taiyo Yuden and Samsung Electro‑Mechanics specialize in thin‑film polymer composites that enable flexible PCB integration. AVX Corporation supplies low‑loss dielectric inks for printed RF components, while Skyworks Solutions focuses on high‑frequency filter modules that incorporate proprietary dielectric blends. NXP Semiconductors and Keysight Technologies add depth with integrated RF front‑end solutions and measurement platforms respectively, driving co‑development with network operators. Additional contributors such as Vishay Intertechnology, Qorvo, and Amphenol Advanced Sensors expand the ecosystem by targeting specific sub‑segments like RF power handling, miniaturized antenna arrays, and sensor‑grade dielectric coatings, ensuring robust competition across the value chain.

List of Key 5G Dielectrics Companies Profiled

- Rogers Corporation

- TDK Corporation

- Murata Manufacturing

- Taiyo Yuden

- Samsung Electro‑Mechanics

- AVX Corporation

- Skyworks Solutions

- NXP Semiconductors

- Keysight Technologies

- Vishay Intertechnology

- Qorvo

- Amphenol Advanced Sensors

- Intel Corporation

- Broadcom Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ceramic Dielectrics dominate the high‑frequency segment because they deliver exceptional thermal stability and low dielectric loss, which are critical for millimeter‑wave antenna performance. • Their intrinsic rigidity supports precise substrate fabrication, enabling consistent signal propagation. • Ongoing material‑science research is driving formulations that tolerate higher power densities while maintaining insulation integrity. • Manufacturers are leveraging advanced sintering techniques to enhance micro‑structural uniformity, thereby improving overall reliability for 5G infrastructure. |

| By Application |

|

Antenna Substrates are the primary growth driver as network operators demand ever‑higher signal fidelity. • Low‑loss characteristics of modern dielectrics enable compact antenna designs that fit dense urban deployments. • The shift toward massive MIMO arrays amplifies the need for substrates that sustain phase coherence across numerous elements. • Design engineers value material consistency, which reduces tuning cycles and accelerates time‑to‑market for new 5G hardware. |

| By End User |

|

Telecom Infrastructure Providers prioritize reliability and long‑term performance; they view advanced dielectrics as enablers of network resilience. • Their procurement teams favor suppliers with strong R&D pipelines, ensuring that new material releases align with evolving 5G standards. • Integration simplicity and compatibility with existing fabrication lines reduce operational friction. • Ongoing collaborations with material innovators foster co‑development of custom dielectric blends tailored to specific site conditions. |

| By Frequency Range |

|

60‑100 GHz segment is attracting attention due to its role in back‑haul and high‑capacity links. • Dielectric materials that retain low loss at these extreme frequencies are essential for maintaining link budget margins. • Industry experts note that hybrid composites, combining ceramic particles with polymer matrices, are emerging as optimal solutions for this band. • The focus on thermal management intensifies, as higher frequencies generate more heat within compact modules. |

| By Material Innovation |

|

Nanostructured Polymer Composites are reshaping the market by offering a balance of flexibility and performance. • Their engineered filler distribution reduces scattering losses, enhancing signal clarity. • The ability to process these materials at lower temperatures cuts production energy consumption, aligning with sustainability goals. • Collaborative research programs between academia and leading manufacturers are accelerating the translation of lab‑scale breakthroughs into commercially viable products. |

Regional Analysis: North America

United States

The ongoing rollout of 5G networks necessitates significant investment in base stations and supporting infrastructure, creating a consistent demand for high-quality 5G dielectrics. 5G Dielectrics Market growth is intertwined with the pace of this infrastructure expansion.

Continuous research and development in dielectric materials are enabling the development of components capable of handling higher frequencies and greater power levels, thereby driving innovation 5G Dielectrics Market.

Government support and regulatory frameworks are playing a crucial role in fostering the growth of the 5G sector and, consequently, 5G Dielectrics Market in the United States.

Growing demand from various end-use industries like telecommunications, automotive, and IoT is further propelling the expansion of 5G Dielectrics Market.

Europe

The European 5G dielectrics market is characterized by a strong emphasis on sustainability and energy efficiency. Several countries in Europe are leading the way in 5G deployment, particularly in sectors like smart cities and industrial automation. The regulatory landscape in Europe encourages the adoption of green technologies, influencing the development of environmentally friendly dielectric materials. While the market is fragmented across different European nations, there is a collective drive towards standardization and interoperability. The focus on data privacy and security also impacts the selection of dielectric components, with a preference for solutions that offer robust protection. 5G Dielectrics Market players in Europe are actively engaged in collaborative research projects to enhance material performance and reduce manufacturing costs.

Asia-Pacific

Asia-Pacific is projected to be the largest and fastest-growing 5G dielectrics market globally. Countries like China, Japan, and South Korea are at the forefront of 5G innovation and infrastructure development. The region’s robust manufacturing base and increasing adoption of 5G-enabled devices are major contributors to market growth. Government initiatives promoting technological self-reliance and the integration of 5G with other advanced technologies are further accelerating market expansion. 5G Dielectrics Market in Asia-Pacific is witnessing significant investment in R&D, with a focus on developing high-frequency dielectrics for next-generation 5G applications.

South America

5G Dielectrics Market in South America is in its nascent stages but is expected to witness considerable growth in the coming years. Increasing investments in telecommunications infrastructure and the growing adoption of 5G-enabled devices are driving market demand. The region presents significant opportunities for players offering cost-effective and reliable dielectric solutions. Government policies aimed at promoting digital inclusion are also contributing to the expansion of 5G Dielectrics Market.

Middle East & Africa

The Middle East and Africa represent a promising growth region for 5G Dielectrics Market. Rapid urbanization, increasing internet penetration, and government initiatives to upgrade telecommunications infrastructure are fueling demand. The region’s focus on smart cities and digital transformation creates a conducive environment for 5G deployment. 5G Dielectrics Market in this region is expected to see significant expansion in the coming years, driven by increasing investments in 5G infrastructure and the growing adoption of connected devices.

Report Scope

This market research report provides a comprehensive analysis of the 5G Dielectrics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 5G Dielectrics Market?

-> 5G Dielectrics Market size was valued at USD 1.48 billion in 2025. The market is projected to grow from USD 1.58 billion in 2026 to USD 3.14 billion by 2034, exhibiting a CAGR of 7.9%

Which key companies operate 5G Dielectrics Market?

-> Key players include Rogers Corporation, TDK Corporation, and Murata Manufacturing, among others.

What are the key growth drivers?

-> Key growth drivers include accelerated 5G network rollouts, demand for low‑loss dielectric substrates, and advancements in material science such as low‑temperature co‑fire ceramics and polymer composites.

Which region dominates the market?

-> Asia‑Pacific is emerging as the fastest‑growing region, while Europe remains a significant market.

What are the emerging trends?

-> Emerging trends include development of low‑temperature co‑fire ceramic dielectrics, polymer‑based composite materials, and integration of AI‑driven design for high‑frequency substrates.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...