MARKET INSIGHTS

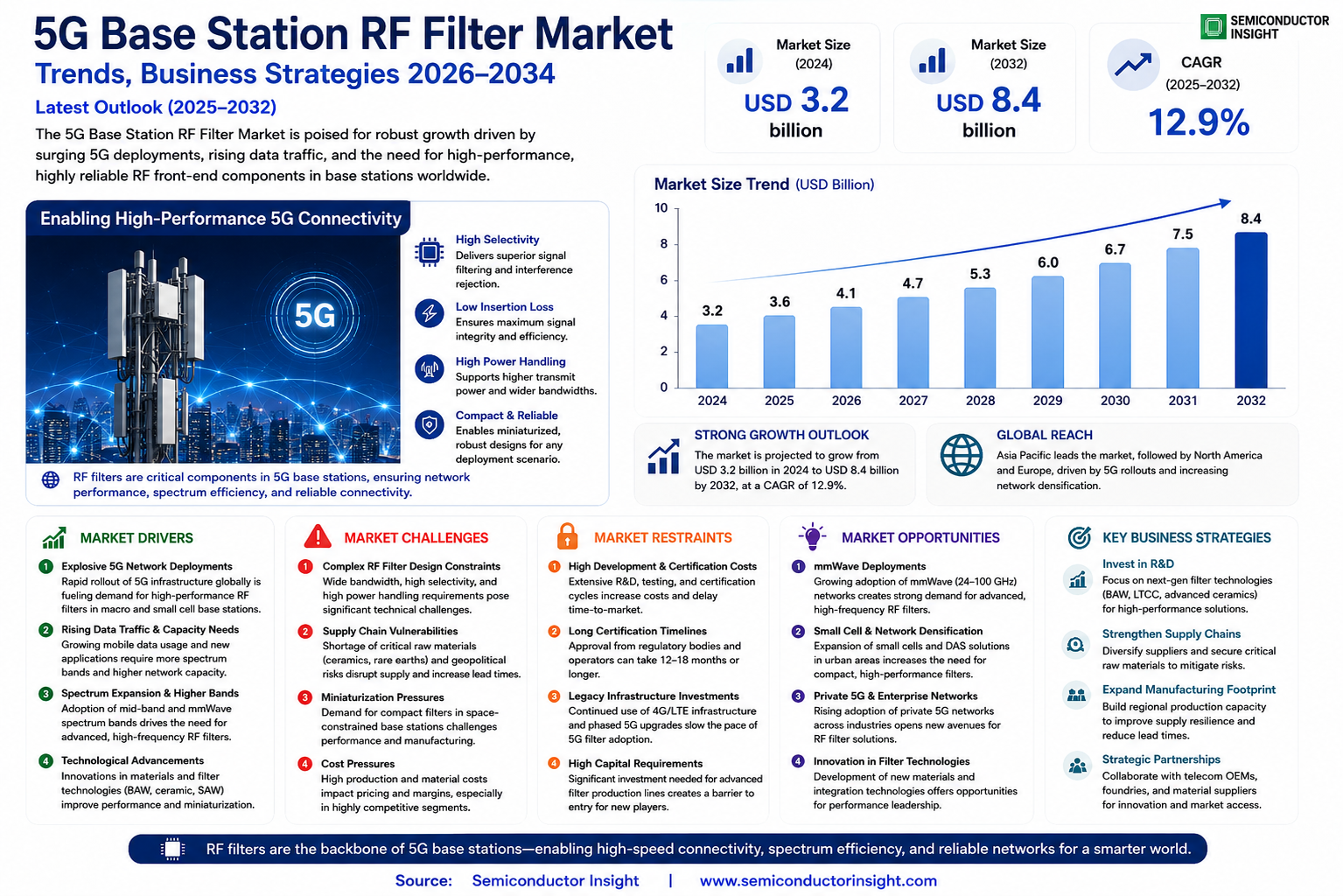

The global 5G Base Station RF Filter Market size was valued at US$ 3.2 billion in 2024 and is projected to reach US$ 8.4 billion by 2032, at a CAGR of 12.9% during the forecast period 2025-2032.

5G base station RF filters are critical components that ensure signal integrity by eliminating interference in the high-frequency bands used for 5G networks. These filters operate across various frequency ranges, including 2.6GHz and 3.5GHz, which are among the most widely adopted 5G spectrums globally. The technology enables efficient spectrum utilization while maintaining compliance with stringent regulatory standards.

The market growth is primarily driven by rapid 5G infrastructure deployment worldwide. China leads in adoption, accounting for over 60% of global 5G base stations as of 2022. The country added 887,000 new stations in 2022 alone, reaching a total of 2.31 million. Furthermore, with 561 million 5G users in China, the demand for high-performance RF filters continues to surge. While developed markets are accelerating deployments, emerging economies are also increasing investments to bridge the digital divide. Key players like Murata, Molex, and GrenTech are expanding production capacities to meet this growing demand, particularly for small cell applications in urban environments.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Global 5G Network Expansion Driving RF Filter Demand

The accelerated global deployment of 5G infrastructure is creating unprecedented demand for RF filters in base stations. Global mobile users exceeded 5.4 billion by the end of 2022, with 5G networks rapidly becoming the new standard for telecommunications. China leads this expansion with over 887,000 new 5G base stations added in 2022 alone, bringing its total to 2.31 million stations – representing more than 60% of the world’s 5G infrastructure. This massive infrastructure buildout requires highly specialized RF filters to ensure signal clarity and prevent interference across multiple frequency bands. The transition from 4G to 5G networks typically triples the number of RF filters needed per base station because 5G operates across a broader spectrum of frequencies while requiring stricter signal isolation standards.

Spectrum Efficiency Requirements Pushing Filter Technology Innovation

Modern 5G networks demand increasingly sophisticated RF filters to maximize spectrum utilization while minimizing interference. The shift toward higher frequency bands (including mmWave spectrum above 24 GHz) and the implementation of carrier aggregation technologies require filters with superior selectivity and power handling capabilities. This technological shift has led to a notable transition from traditional surface acoustic wave (SAW) filters to bulk acoustic wave (BAW) filters, which offer better performance at higher frequencies. The global 5G base station RF filter market is responding with innovative solutions, including thermally stable ceramic filters and tunable filters that can adapt to different frequency bands dynamically. These advancements are critical as mobile operators seek to optimize their network performance and capacity.

Government Support and Smart City Initiatives Boosting Investments

National digital infrastructure programs and smart city initiatives worldwide are catalyzing investments in 5G infrastructure. Countries are implementing policies to accelerate 5G deployments as part of broader economic development strategies. The establishment of 110 gigabit-capable cities in China demonstrates how national priorities are driving 5G infrastructure development. Similar initiatives in North America, Europe, and Asia-Pacific are creating sustained demand for base station components, including RF filters. Government funding for 5G research and pilot programs, combined with private sector investments in network densification, are establishing a strong foundation for long-term market growth in the RF filter segment.

➤ Network densification efforts in urban areas frequently require small cell deployments with specialized filter solutions to handle high-density traffic without interference.

Furthermore, the increasing adoption of massive MIMO (Multiple Input Multiple Output) antenna systems in 5G networks is multiplying the need for compact, high-performance RF filters, as these advanced antennas require individual filters for each radiating element to maintain signal integrity.

MARKET CHALLENGES

Complex RF Filter Design Constraints Posing Technical Barriers

The 5G revolution brings significant technical challenges in RF filter design, as these components must meet increasingly stringent performance requirements. Modern filters need to handle wider bandwidths while maintaining sharp rejection of adjacent frequency bands – a combination that pushes the limits of current materials science and manufacturing capabilities. The transition to higher frequency bands compounds these challenges, as filter performance becomes more sensitive to manufacturing tolerances and material properties. This complexity leads to higher development costs and extended qualification periods, particularly for cutting-edge ceramic and BAW filters that dominate the high-performance segment of the market.

Other Challenges

Supply Chain Vulnerabilities

The RF filter market faces persistent supply chain challenges, particularly for specialized raw materials like high-purity ceramics and rare earth elements used in advanced filter designs. Geopolitical factors and trade restrictions have created bottlenecks in the availability of these critical materials, disrupting production schedules and increasing lead times. The specialized nature of filter manufacturing means that establishing alternative supply sources requires substantial capital investment and lengthy qualification processes.

Miniaturization Pressures

The space constraints in modern 5G base stations, especially for small cell deployments, demand increasingly compact filter solutions without sacrificing performance. This miniaturization challenge requires innovative packaging technologies and novel materials that can maintain filter Q-factors (quality factors) while reducing physical dimensions. The industry faces a formidable technical hurdle in balancing these competing demands of size, performance, and cost.

MARKET RESTRAINTS

High Development Costs and Prolonged Certification Cycles Slowing Innovation

The RF filter market faces significant constraints from the substantial investments required for product development and certification. Designing filters that meet the exacting standards of 5G networks typically requires extensive simulation, prototyping, and testing cycles. The certification process with regulatory bodies and network operators often takes 12-18 months, delaying time-to-market for new filter solutions. Furthermore, the capital expenditure for establishing production lines capable of manufacturing advanced ceramic and BAW filters can exceed tens of millions of dollars, creating a high barrier to entry for new market participants. These financial and temporal constraints limit the pace of innovation and create a challenging environment for smaller suppliers.

Legacy Infrastructure Investments Limiting 5G Filter Adoption Rates

Despite the accelerating 5G rollout, many network operators continue to maintain substantial investments in 4G/LTE infrastructure, which utilizes different filter technologies. This dual-network operation creates budgetary pressures that can slow the full transition to 5G-specific filter solutions. The economic lifecycle of existing base station equipment means that operators often phase in 5G upgrades gradually rather than through complete infrastructure replacements. This staggered transition tempers the immediate demand for 5G RF filters, particularly in markets where 4G networks still effectively serve current capacity requirements.

MARKET OPPORTUNITIES

Emerging mmWave Deployments Creating Demand for Advanced Filter Solutions

The ongoing deployment of 5G networks in millimeter wave frequency bands (24-100 GHz) presents significant growth opportunities for RF filter manufacturers. These high-frequency bands require filters with exceptional performance characteristics to manage the challenging propagation conditions while preventing interference between closely-spaced channels. The mmWave market segment is expected to grow as network operators address capacity constraints in dense urban environments. This transition creates demand for novel filter technologies that can operate effectively at these elevated frequencies while maintaining acceptable insertion loss and power handling capabilities.

Open RAN Architectures Driving Diversity in Filter Supply Chains

The growing adoption of Open Radio Access Network (O-RAN) architectures is reshaping the RF filter market landscape. O-RAN’s modular approach encourages multi-vendor interoperability, creating opportunities for specialized filter suppliers to compete with traditional integrated solutions. This architectural shift reduces barriers to entry for innovative filter technologies and promotes competition based on technical merit rather than proprietary system integration. The Open RAN movement is particularly significant for small and mid-sized filter manufacturers that can develop optimized solutions for specific frequency bands or deployment scenarios.

Additionally, the integration of artificial intelligence in network optimization is creating demand for adaptive filtering solutions that can dynamically adjust to changing network conditions and traffic patterns. These intelligent filtering technologies represent the next frontier in RF component innovation, promising to enhance spectral efficiency and network performance.

5G BASE STATION RF FILTER MARKET TRENDS

Global 5G Network Expansion Driving RF Filter Demand

The rapid expansion of 5G networks worldwide is accelerating the demand for RF filters, essential components in base stations that ensure signal clarity by eliminating interference. With over 2.3 million 5G base stations deployed globally by 2023—60% of which are in China alone—the market for high-performance RF filters continues to surge. As mobile operators invest in high-band (mmWave) and mid-band (3.5GHz) spectrum deployments, filter manufacturers are innovating to meet stringent performance requirements for insertion loss, thermal stability, and power handling capacity.

Other Trends

Miniaturization and Integration

The push for compact and energy-efficient base stations, particularly for urban small cell deployments, is driving filter miniaturization. Advanced materials like gallium nitride (GaN) and low-temperature co-fired ceramics (LTCC) are gaining traction, enabling filters to achieve higher power densities while reducing footprint. This trend is critical as telecom operators densify networks to support IoT and ultra-reliable low-latency communications (URLLC) applications requiring sub-1ms latency.

Regional Market Diversification

While Asia-Pacific dominates with over 65% market share in 5G base station deployments, North America and Europe are now accelerating investments to bridge the infrastructure gap. The U.S. FCC’s C-band auction unlocked $81 billion in spectrum licenses, directly fueling demand for 3.5GHz RF filters. Meanwhile, European nations are prioritizing Open RAN architectures, creating opportunities for specialized filter solutions compatible with multi-vendor ecosystems. This geographical diversification is reshaping global supply chains, with manufacturers establishing local production facilities to mitigate trade restrictions.

Technological Evolution in Filter Design

Emerging tunable RF filter technologies are addressing the challenge of spectrum flexibility in 5G-Advanced networks. Contemporary designs now incorporate MEMS-based reconfigurable filters that dynamically adjust frequency response, reducing the need for multiple fixed filters in multi-band radios. Laboratories have demonstrated filters with 40% bandwidth reconfigurability while maintaining < 1.5dB insertion loss—a critical advancement for future-proofing base station investments. Furthermore, AI-driven filter optimization algorithms are enabling real-time performance adjustments based on network load and interference patterns.

COMPETITIVE LANDSCAPE

Key Industry Players

RF Filter Manufacturers Compete on Innovation and Cost Efficiency to Capture 5G Expansion

The global 5G Base Station RF Filter market features a dynamic competitive landscape with both established leaders and emerging challengers vying for market share. Chinese players dominate the volume supply, while international firms maintain strong footholds in high-performance segments. Murata Manufacturing leads the industry with its advanced ceramic filter technology, capturing approximately 18% of the global market share in 2024. Their dominance stems from decades of RF component expertise and strategic partnerships with major telecom equipment vendors.

Qorvo and Skyworks Solutions follow closely, leveraging their integrated RF solutions and strong presence in North American and European markets. These companies have successfully adapted their 4G filter technologies for 5G applications, particularly in the 3.5GHz band which accounts for nearly 45% of global 5G deployments. Their R&D investments in bulk acoustic wave (BAW) and surface acoustic wave (SAW) filter technologies continue to set industry benchmarks.

Meanwhile, Chinese manufacturers like Tongyu Communication and Fenghua Advanced Technology are rapidly expanding their market presence through aggressive pricing and scaled production. The Chinese government’s push for domestic 5G infrastructure has created a robust ecosystem for these suppliers, with local manufacturers now supplying over 70% of filters used in China’s massive 5G rollout.

The competitive intensity is further heightened by vertical integration strategies. Companies such as Molex and Taoglas have expanded beyond filters to offer complete RF front-end modules, creating stronger value propositions for base station manufacturers. This trend is expected to accelerate as 5G Advance and future 6G standards demand more integrated antenna-filter solutions.

List of Key 5G Base Station RF Filter Companies Profiled

- Murata Manufacturing (Japan)

- Qorvo, Inc. (U.S.)

- Skyworks Solutions (U.S.)

- Molex, LLC (U.S.)

- Taoglas Group (Ireland)

- Tongyu Communication Inc. (China)

- Fenghua Advanced Technology (China)

- GrenTech (China)

- Wuhan Fingu Electronic (China)

- DSBJ (China)

Segment Analysis:

By Type

3.5Hz Segment Leads the Market Due to Dominant Adoption in 5G Infrastructure Deployment

The market is segmented based on type into:

- 2.6Hz

- 3.5Hz

- Others

By Application

Large Cellular Base Station Segment Dominates Owing to Higher Network Coverage Requirements

The market is segmented based on application into:

- Small Cellular Base Station

- Large Cellular Base Station

By Frequency Band

Sub-6GHz Segment Shows Strong Growth Potential for Urban Deployments

The market is segmented based on frequency band into:

- Sub-6GHz

- mmWave

By Material

Ceramic RF Filters Maintain Dominance Due to Superior Thermal Properties

The market is segmented based on material into:

- Ceramic

- SAW

- BAW

- Others

Regional Analysis: 5G Base Station RF Filter Market

Asia-Pacific

The Asia-Pacific region dominates the 5G Base Station RF Filter market, with China leading in both production and deployment. By the end of 2022, China accounted for over 60% of global 5G base stations, with 2.312 million installations and 561 million 5G users. Rapid urbanization, government-backed digital infrastructure projects like China’s “Gigabit City” initiative, and the increasing adoption of IoT applications continue to drive demand for high-performance RF filters. Countries like Japan and South Korea are also investing heavily in 5G expansion, particularly in the 3.5Hz frequency band, which is widely used for mid-band deployments. However, supply chain dependencies on semiconductor components and geopolitical trade restrictions pose challenges for manufacturers in the region.

North America

With significant investments in Open RAN (O-RAN) architecture and private 5G networks, North America remains a key market for advanced RF filter solutions. The U.S. Federal Communications Commission’s (FCC) spectrum auctions, particularly for C-band frequencies, have accelerated demand for filters that minimize interference and enhance signal clarity. Major telecom operators are prioritizing small cellular base stations to improve urban coverage, creating opportunities for compact, high-efficiency RF filter designs. However, stringent testing requirements from organizations like the FCC and intense competition from Asian suppliers impact local manufacturers’ pricing strategies.

Europe

Europe’s 5G RF filter market is shaped by regulatory harmonization under the EU’s 5G Action Plan and the push for sustainable, energy-efficient networking equipment. Countries like Germany and the U.K. are focusing on industrial 5G applications, requiring ruggedized filters for manufacturing and logistics environments. While vendors are adopting gallium nitride (GaN) and bulk acoustic wave (BAW) technologies to improve performance, slower-than-expected spectrum allocation in some nations has delayed large-scale deployments. The region also faces challenges in reducing reliance on non-European suppliers for critical filter components.

South America

The 5G RF filter market in South America is in its early stages, with Brazil leading initial deployments. Auction delays and economic uncertainties have slowed progress, but increasing smartphone penetration and demand for enhanced mobile broadband services are driving gradual adoption. Local regulators are prioritizing cost-effective solutions, creating opportunities for suppliers offering durable, mid-range filters tailored to tropical climate conditions. Infrastructure limitations and fragmented spectrum policies, however, continue to hinder widespread 5G rollout and associated filter demand.

Middle East & Africa

Selected Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, are investing heavily in 5G infrastructure to support smart city initiatives and diversify their economies. High-temperature-resistant RF filters are in demand to withstand harsh desert environments, with a focus on minimizing power losses in base stations. In contrast, Sub-Saharan Africa faces slower adoption due to budget constraints and limited fiber backhaul networks. The region shows long-term potential as mobile operators gradually shift from 4G/LTE to 5G, though filter suppliers must navigate complex import regulations and localization requirements.

Report Scope

This market research report provides a comprehensive analysis of the global 5G Base Station RF Filter market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (2.6Hz, 3.5Hz, Others), application (Small Cellular Base Station, Large Cellular Base Station), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 5G Base Station RF Filter Market?

-> 5G Base Station RF Filter Market size was valued at US$ 3.2 billion in 2024 and is projected to reach US$ 8.4 billion by 2032, at a CAGR of 12.9% during the forecast period 2025-2032.

Which key companies operate in Global 5G Base Station RF Filter Market?

-> Key players include Murata, GrenTech, Molex, Partron, Ube Electronics, Taoglas, and Fenghua Advanced Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rapid 5G infrastructure deployment, increasing demand for high-frequency communication, and government initiatives supporting 5G adoption.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 60% of global 5G base station deployments, with China leading in both infrastructure and RF filter adoption.

What are the emerging trends?

-> Emerging trends include miniaturization of RF components, development of advanced filtering technologies, and integration of AI for optimized RF performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...