MARKET INSIGHTS

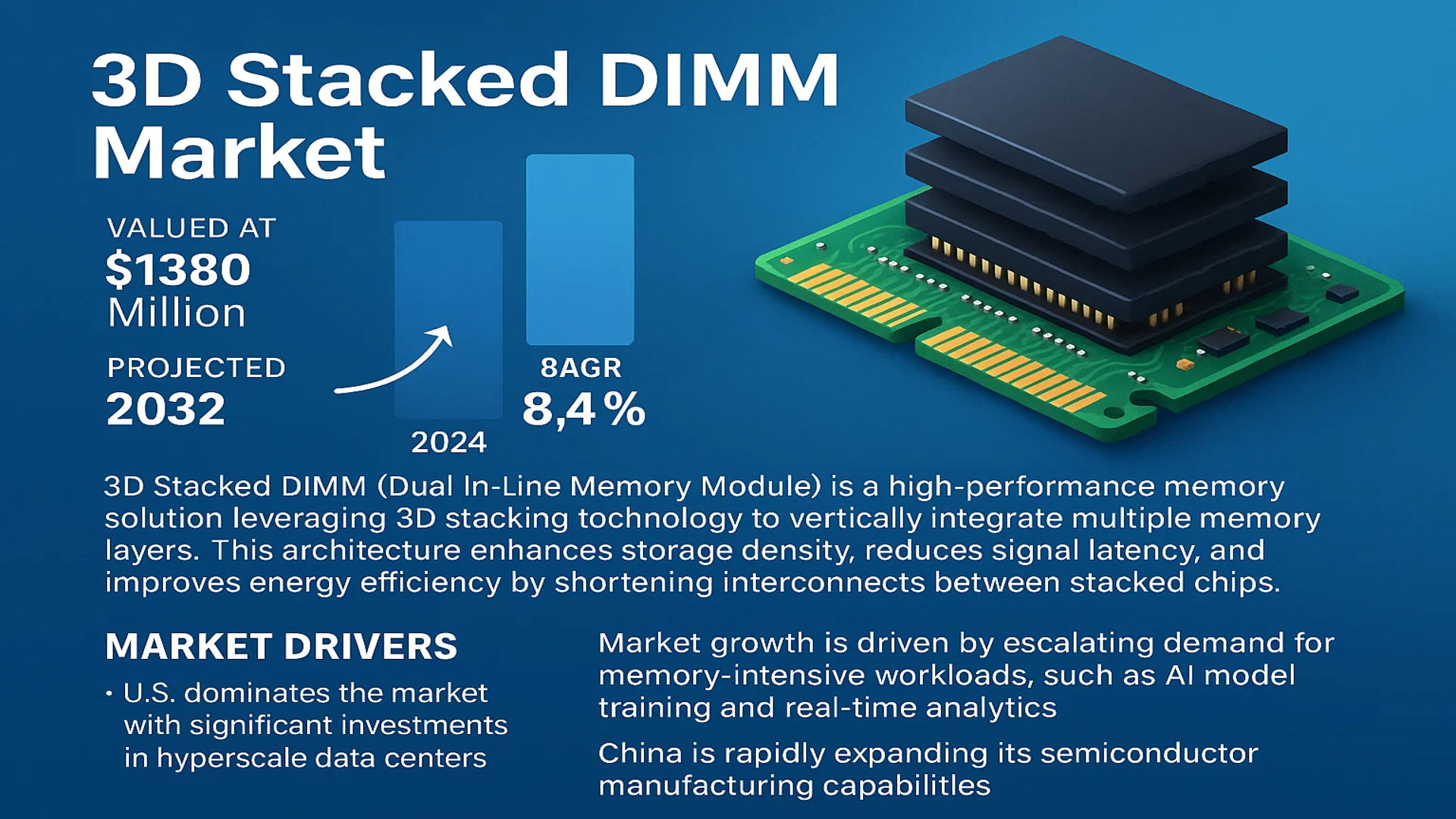

The global 3D Stacked DIMM Market was valued at 1380 million in 2024 and is projected to reach US$ 2300 million by 2032, at a CAGR of 8.4% during the forecast period.

3D Stacked DIMM (Dual In-Line Memory Module) is a high-performance memory solution leveraging 3D stacking technology to vertically integrate multiple memory layers. This architecture enhances storage density, reduces signal latency, and improves energy efficiency by shortening interconnects between stacked chips. The technology is widely adopted in data centers, high-performance computing (HPC), and AI applications where bandwidth and capacity demands are critical.

Market growth is driven by escalating demand for memory-intensive workloads, such as AI model training and real-time analytics. The U.S. dominates the market with significant investments in hyperscale data centers, while China is rapidly expanding its semiconductor manufacturing capabilities. Key players like Micron, Samsung Semiconductor, and SK Hynix are accelerating innovation, with Through Silicon Via (TSV) stacking emerging as the dominant technology segment. Recent advancements include Micron’s 2024 launch of 128GB 3D-stacked DIMMs for AI servers, reinforcing the technology’s pivotal role in next-generation computing.

MARKET DYNAMICS

MARKET DRIVERS

Explosive Growth in AI and HPC Workloads to Accelerate 3D Stacked DIMM Adoption

The global artificial intelligence market is projected to grow at over 35% CAGR through 2030, creating unprecedented demand for high-bandwidth memory solutions. 3D stacked DIMMs address this need by offering up to 8x higher memory density and 30% lower power consumption compared to traditional modules. Major cloud providers like AWS, Google Cloud, and Microsoft Azure are deploying these modules to handle the massive parallel processing requirements of AI training workloads, driving significant market expansion.

Data Center Modernization Initiatives Fueling Market Momentum

With hyperscale data centers projected to account for over 50% of all data center traffic by 2025, infrastructure upgrades are creating strong demand for 3D stacked DIMMs. These modules’ ability to provide 4-6TB/s bandwidth per socket makes them ideal for memory-intensive applications in next-generation servers. The shift toward software-defined infrastructure and composable architectures is further accelerating adoption, as cloud operators seek to optimize resource utilization and reduce total cost of ownership.

➤ The server market alone is expected to consume over 60% of all 3D stacked DIMM production by 2026, with forecasts indicating a 200% increase in cloud provider deployments compared to 2023 levels.

MARKET RESTRAINTS

Complex Manufacturing Processes Constraining Market Expansion

3D stacked DIMM production involves sophisticated TSV (Through-Silicon Via) technology with yield rates currently averaging 70-75% across manufacturers. This not only increases production costs by 25-30% compared to conventional DIMMs but also creates supply chain bottlenecks. The capital expenditure required for TSV-capable fabrication exceeds $5 billion per facility, limiting new market entrants and creating significant barriers to scaling production capacity.

Other Restraints

Compatibility Challenges

Legacy system architectures struggle to fully leverage 3D stacked DIMM capabilities, requiring expensive platform redesigns. Approximately 40% of potential enterprise customers report compatibility concerns delaying their adoption timelines, particularly in industries with long hardware refresh cycles.

Thermal Management Issues

The high component density of 3D stacked DIMMs generates thermal hotspots requiring advanced cooling solutions. These thermal constraints add 10-15% to total system cost and complicate deployment in space-constrained environments.

MARKET CHALLENGES

Supply Chain Vulnerabilities Threatening Market Stability

The 3D stacked DIMM market faces significant supply chain risks with over 80% of advanced packaging capacity concentrated in just three countries. Recent export controls on semiconductor equipment and materials have created uncertainty about long-term production stability. Lead times for critical components like interposers have extended to 26-32 weeks, compared to 8-12 weeks for traditional memory components.

Other Challenges

Testing Complexity

3D stacked DIMMs require 50% more test coverage than planar memory due to their vertical architecture. This testing overhead adds approximately 15% to manufacturing costs and creates bottlenecks in production throughput.

Skill Gaps

The specialized nature of 3D IC design creates a talent shortage, with fewer than 5,000 qualified 3D packaging engineers globally. Training programs are struggling to keep pace with industry demand, potentially slowing the rate of technology advancement.

MARKET OPPORTUNITIES

Emerging Applications in Edge Computing and 5G Networks Opening New Revenue Streams

The rollout of 5G networks and edge computing infrastructure represents a $120 billion opportunity for 3D stacked DIMMs by 2028. These applications require memory solutions that balance high performance with energy efficiency – precisely the strengths of 3D architecture. Telecom operators are increasingly specifying 3D stacked modules for their next-generation base stations and edge servers, creating a new high-growth vertical beyond traditional data center applications.

Heterogeneous Integration Revolution to Transform Memory Landscape

Advancements in chiplet architectures and 3D system-in-package designs are enabling novel applications for 3D stacked DIMMs. The integration of emerging memory technologies like MRAM and ReRAM with conventional DRAM in 3D configurations could unlock performance gains exceeding 40% for specialized workloads. Memory manufacturers are investing heavily in hybrid architectures, with prototypes demonstrating 100GB/s bandwidth at sub-5W power envelopes.

➤ Recent industry collaborations have demonstrated 3D stacked modules with integrated CPU logic layers, potentially revolutionizing memory hierarchy design and creating $10 billion in new market opportunities by 2030.

3D STACKED DIMM MARKET TRENDS

AI and High-Performance Computing Fuel Demand for 3D Stacked DIMM Solutions

The global market for 3D Stacked DIMM is experiencing rapid growth, driven primarily by the increasing demand for high-bandwidth memory solutions in artificial intelligence (AI), machine learning, and high-performance computing (HPC) applications. The technology’s ability to vertically stack multiple memory layers significantly enhances capacity while reducing signal latency, making it indispensable for data-intensive workloads. Projections indicate that by 2032, the market will reach $2.3 billion, growing at a CAGR of 8.4% from its 2024 valuation of $1.38 billion. Leading companies like Micron, Samsung Semiconductor, and SK Hynix are heavily investing in Through Silicon Via (TSV) Stacking, which remains the most adopted technology, expected to dominate 67% of the market share by 2032.

Other Trends

Accelerating Data Center Upgrades

Data centers are transitioning to hyperscale infrastructures, necessitating memory solutions with superior power efficiency and performance. The adoption of 3D Stacked DIMM in servers is projected to grow at a 9.2% CAGR through 2032, driven by cloud service providers optimizing for AI-driven workloads. This shift is particularly pronounced in North America, where investments in next-gen server architectures account for over 40% of global expenditures. Meanwhile, China’s aggressive push in semiconductor self-sufficiency has positioned it as the fastest-growing market, with a projected 12% annual growth rate.

Challenges in Cost and Manufacturing Complexity

Despite its advantages, the 3D Stacked DIMM market faces hurdles in cost-efficiency and yield rates. TSV-based stacking, while dominant, involves intricate manufacturing processes that result in higher production costs compared to traditional DDR modules. Industry experts note that yield rates for advanced stacking technologies hover around 75–80%, prompting manufacturers like Intel and ASE to invest in advanced packaging innovations to reduce defects. Additionally, thermal management remains a critical concern, as denser memory configurations require sophisticated cooling solutions to maintain stability in high-performance environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation Through Strategic Investments and Technological Advancements

The global 3D Stacked DIMM market features a highly competitive landscape dominated by major semiconductor and memory manufacturing giants, with the top five players accounting for a significant revenue share in 2024. Micron and Samsung Semiconductor currently lead the market, leveraging their extensive R&D capabilities and established supply chains to deliver high-performance 3D stacked memory solutions. These companies benefit from their vertically integrated production models, allowing them to maintain cost efficiencies while scaling production.

SK Hynix and Intel follow closely, specializing in Through Silicon Via (TSV) stacking technology – a critical segment projected to experience strong growth through 2032. Both companies have actively expanded their 3D memory offerings through collaborations with data center operators and AI hardware developers, positioning themselves as key enablers of next-generation computing architectures.

The market also sees dynamic participation from foundry and packaging specialists like ASE and Amkor Technology, whose advanced packaging solutions enable the production of complex 3D stacked DIMM modules. These companies help bridge the gap between memory design and high-volume manufacturing, becoming indispensable partners in the ecosystem.

Recent developments show market leaders focusing on capacity expansion and technological refinement. Micron recently announced plans to invest $15 billion in new memory fabrication facilities, while Samsung unveiled its fifth-generation 3D-stacked HBM memory with improved power efficiency. Such continuous innovation helps maintain competitive advantage in this rapidly evolving sector.

List of Key 3D Stacked DIMM Companies Profiled

- Micron Technology, Inc. (U.S.)

- Samsung Semiconductor (South Korea)

- SK Hynix (South Korea)

- Intel Corporation (U.S.)

- ASE Technology Holding Co., Ltd. (Taiwan)

- GlobalFoundries Inc. (U.S.)

- SMBOM (China)

- KIOXIA (China) Co., Ltd. (China)

- Western Digital (U.S.)

- Amkor Technology, Inc. (U.S.)

Segment Analysis:

By Type

Through Silicon Via (TSV) Stacking Dominates the Market Due to Its Superior Performance in High-Bandwidth Applications

The market is segmented based on type into:

- Through Silicon Via (TSV) Stacking

- Subtypes: Wide I/O, Hybrid Memory Cube (HMC), and others

- Package-level Stacking

- Subtypes: PoP (Package on Package), PiP (Package in Package), and others

By Application

Servers Segment Leads Due to High Demand for Data Center Memory Solutions

The market is segmented based on application into:

- Servers

- Mobile Devices

- High-Performance Computing (HPC) Systems

- Artificial Intelligence Hardware

- Others

Regional Analysis: 3D Stacked DIMM Market

Asia-Pacific

The Asia-Pacific region dominates the global 3D Stacked DIMM market, accounting for the largest revenue share due to rapid technological adoption and strong semiconductor manufacturing capabilities. Countries like China, South Korea, and Japan are driving growth with substantial investments in AI infrastructure, data centers, and 5G networks. China’s semiconductor self-sufficiency initiatives and South Korea’s leadership in memory technology (home to Samsung and SK Hynix) give the region a competitive edge. India’s emerging IT sector and government-backed digital economy projects are creating additional demand for high-performance memory solutions. While cost sensitivity remains a factor, the region’s focus on advanced computing and automation continues to fuel 3D Stacked DIMM adoption across enterprise and consumer applications.

North America

North America is the second-largest market for 3D Stacked DIMMs, propelled by cutting-edge R&D and early adoption of high-performance computing technologies. The U.S. leads the region with its robust data center ecosystem (hosting nearly 40% of global hyperscale facilities) and strong presence of tech giants like Intel, Micron, and NVIDIA. Demand stems from AI/ML workloads, cloud computing expansion, and government-funded supercomputing projects. Canada is emerging as a growth market with investments in quantum computing and AI research clusters. However, export restrictions on advanced memory technologies to certain markets pose moderate challenges for regional suppliers.

Europe

Europe maintains steady growth in the 3D Stacked DIMM market through focused semiconductor sovereignty initiatives and high-performance computing investments. The EU Chips Act’s €43 billion investment plan aims to double Europe’s global semiconductor market share by 2030, benefiting memory technology development. Germany, France, and the Nordic countries lead in adopting 3D Stacked DIMMs for automotive computing, industrial IoT, and scientific research applications. However, the region faces intense competition from Asian memory manufacturers and relies heavily on imports for advanced packaging technologies like TSV stacking.

Middle East & Africa

The MEA region shows emerging potential in the 3D Stacked DIMM market through strategic digital transformation initiatives. Countries like Israel, UAE, and Saudi Arabia are investing in AI infrastructure and smart city projects that require high-bandwidth memory solutions. Israel’s strong semiconductor design ecosystem (particularly in memory controllers) complements growing regional demand. While market penetration remains low compared to other regions, increasing data center construction and government-led technology adoption programs present long-term opportunities. Infrastructure limitations and the lack of local manufacturing remain key constraints.

South America

South America represents a nascent but growing market for 3D Stacked DIMM technology, primarily driven by Brazil’s expanding data center infrastructure and Argentina’s fintech sector. The region faces significant challenges including limited local semiconductor expertise, economic volatility, and dependency on memory imports. However, increasing adoption of cloud services by financial institutions and gradual 5G network deployments are creating new demand pockets. Local production remains minimal, with most 3D Stacked DIMMs sourced through global suppliers like Micron and Samsung.

Report Scope

This market research report provides a comprehensive analysis of the global 3D Stacked DIMM market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global 3D Stacked DIMM market was valued at USD 1,380 million in 2024 and is projected to reach USD 2,300 million by 2032, growing at a CAGR of 8.4%.

- Segmentation Analysis: Detailed breakdown by product type (Through Silicon Via (TSV) Stacking, Package-level Stacking), application (Servers, Mobile Devices), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants, including Micron, Samsung Semiconductor, SK Hynix, Intel, ASE, GlobalFoundries Inc., SMBOM, KIOXIA (China) Co., Ltd., Western Digital, Amkor Technology, among others. In 2024, the top five players held approximately % market share.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, and evolving industry standards in 3D stacking technology.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as increasing demand for high-performance computing and AI applications, along with challenges like supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the 3D Stacked DIMM market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 3D Stacked DIMM Market?

-> 3D Stacked DIMM Market was valued at 1380 million in 2024 and is projected to reach US$ 2300 million by 2032, at a CAGR of 8.4% during the forecast period.

Which key companies operate in Global 3D Stacked DIMM Market?

-> Key players include Micron, Samsung Semiconductor, SK Hynix, Intel, ASE, GlobalFoundries Inc., SMBOM, KIOXIA (China) Co., Ltd., Western Digital, and Amkor Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-performance computing, AI applications, data center expansion, and the need for high-bandwidth memory solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market due to strong semiconductor industry presence.

What are the emerging trends?

-> Emerging trends include advancements in TSV technology, increasing adoption in mobile devices, and integration with AI/ML workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...