3D SoIC hybrid bonding for wafer-on-wafer stacking Market Insights

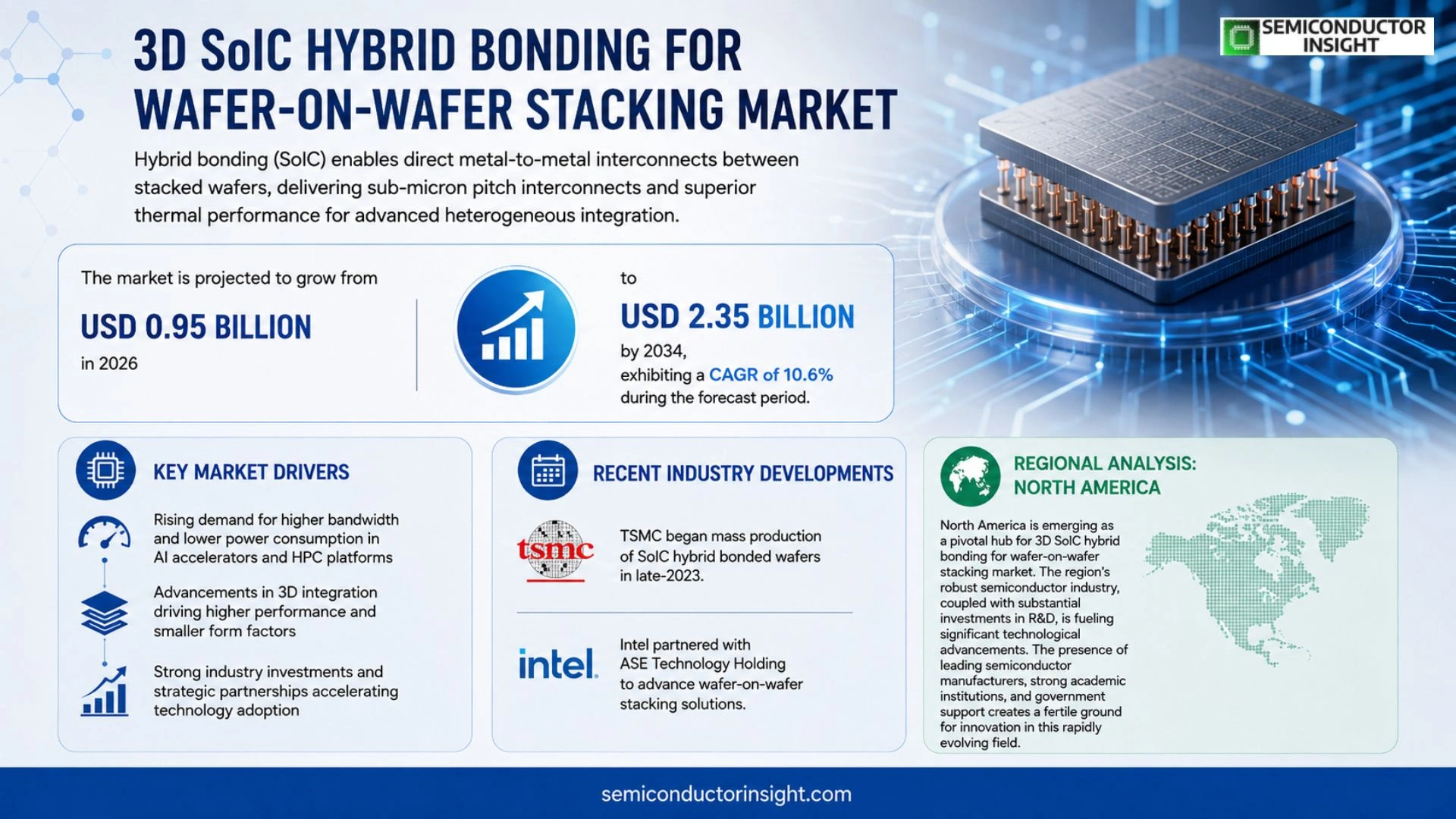

Global 3D SoIC hybrid bonding for wafer-on-wafer stacking market size was valued at USD 0.95 billion in 2025. The market is projected to grow from USD 0.95 billion in 2025 to USD 2.35 billion by 2034, exhibiting a CAGR of 10.6% during the forecast period.

Hybrid bonding, also referred to as silicon‑on‑insulator (SoIC) technology, creates direct metal‑to‑metal interconnects between stacked wafers without solder or adhesive layers, delivering sub‑micron pitch interconnects and superior thermal performance for advanced heterogeneous integration.

The market is accelerating because semiconductor manufacturers are pursuing higher bandwidth and lower power consumption for AI accelerators and high‑performance computing platforms.

Furthermore, recent announcements,such as TSMC’s mass production of SoIC hybrid bonded wafers in late‑2023 and Intel’s partnership with ASE Technology Holding on wafer‑on‑wafer stacking,are driving adoption.

MARKET DRIVERS

Increasing Demand for High‑Performance Computing

3D SoIC hybrid bonding for wafer-on-wafer stacking Market is being propelled by data‑center operators seeking higher bandwidth and lower power consumption. 3D integration enables chip‑to‑chip interconnects with sub‑10 µm pitch, delivering up to 30 % performance uplift compared with traditional 2D packages.

Miniaturization of IoT and Edge Devices

Edge AI and wearable sensors require ultra‑compact form factors. 3D SoIC hybrid bonding allows multiple dies to be stacked without increasing the footprint, supporting the trend toward sub‑5 mm² module sizes while maintaining thermal reliability.

➤ Industry analysts project that adoption of wafer‑on‑wafer stacking will exceed 40 % of new high‑end ASIC launches by 2028.

Regulatory push for energy‑efficient electronics in Europe and North America also encourages manufacturers to migrate to 3D SoIC solutions, creating a sustainable growth pathway for the market.

MARKET CHALLENGES

Process Complexity and Yield Management

Implementing hybrid bonding requires precise planarization and alignment at the sub‑nanometer level. Any deviation can lead to yield losses, and the current average first‑pass yield hovers around 75 %, which restrains large‑scale adoption.

Other Challenges

Cost Sensitivity

The capital outlay for dedicated bonding tools can exceed $15 million, making entry difficult for smaller fabless firms. Consequently, cost‑effective shared‑facility models are emerging as a mitigation strategy.

MARKET RESTRAINTS

Equipment Capital Expenditure

High‑precision bonding equipment and advanced metrology tools represent a significant financial hurdle. Many incumbents defer investment until a clear ROI is demonstrated, slowing the overall market momentum.

MARKET OPPORTUNITIES

Emerging Applications in AI Accelerators

The surge in AI inference workloads creates a demand for densely packed compute modules. 3D SoIC hybrid bonding enables heterogeneous integration of memory and logic dies, offering a pathway to meet the sub‑100 ns latency targets set by next‑generation AI accelerators.

3D SoIC hybrid bonding for wafer-on-wafer stacking Market Trends

Accelerated Adoption Driven by AI and High‑Performance Computing

3D SoIC hybrid bonding for wafer-on-wafer stacking Market is experiencing rapid uptake as semiconductor manufacturers seek sub‑micron interconnect pitch and superior thermal performance for next‑generation AI accelerators and high‑performance computing platforms. Recent production announcements, such as TSMC’s mass‑production of SoIC hybrid‑bonded wafers in late‑2023 and Intel’s partnership with ASE Technology Holding on wafer‑on‑wafer stacking, illustrate a clear shift from pilot to volume manufacturing. Leading fabs,including Samsung Electronics, Amkor Technology, GlobalFoundries and ASE,are expanding dedicated process lines, reducing cycle time and improving yield, which together reinforce the momentum behind heterogeneous integration strategies.

Other Trends

Manufacturing Capacity Expansion

Key players are scaling capacity to meet rising demand. Samsung has introduced a dedicated SoIC bonding line that integrates double‑patterning lithography with low‑temperature annealing, enabling consistent copper‑to‑copper contacts across 300‑mm wafers. GlobalFoundries recently upgraded its wafer‑bonding cluster with advanced alignment sensors, increasing throughput by 20 % while maintaining interconnect resistance below 10 µΩ·cm². ASE’s new modular bonding platforms support both 200‑mm and 300‑mm substrates, allowing flexible production schedules for customers transitioning from traditional 2.5‑D to full 3D integration. These infrastructure investments are complemented by tighter process controls that drive defect densities below 0.5 defects/cm², positioning the ecosystem for sustained volume growth.

Strategic Partnerships and Ecosystem Development

Beyond hardware, 3D SoIC hybrid bonding for wafer-on-wafer stacking Market is benefitting from collaborative ecosystems that align design tools, IP libraries, and packaging standards. Intel’s joint roadmap with ASE includes co‑development of design‑for‑bonding guidelines that streamline layout constraints for sub‑50 µm pitch interconnects. Meanwhile, EDA vendors are integrating SoIC‑aware simulation modules, allowing chip designers to evaluate thermal and signal integrity impacts early in the design phase. These partnerships accelerate time‑to‑market for complex heterogeneous solutions and reinforce confidence among OEMs that the technology can meet the stringent performance targets required for emerging workloads.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of 3D SoIC Hybrid Bonding for Wafer‑on‑Wafer Stacking

The market is currently dominated by a handful of large semiconductor foundries that have already invested in high‑volume hybrid‑bonding lines. TSMC announced mass production of SoIC‑bonded wafers in late‑2023, positioning it as the de‑facto leader for AI‑accelerator and high‑performance computing customers. Intel’s strategic partnership with ASE Technology Holding accelerates its entry into wafer‑on‑wafer stacking, while Samsung Electronics leverages its advanced packaging platform to offer sub‑micron interconnects for next‑generation mobile SoCs. GlobalFoundries and Amkor Technology round out the core group, each expanding their process portfolios to include 3‑D SoIC services, thereby reinforcing a market structure where a few Tier‑1 players control the majority of capacity and technology leadership.

Beyond the Tier‑1 tier, a diverse set of niche and emerging players is expanding the competitive ecosystem. SMIC has begun pilot runs targeting the Chinese AI market, and IBM is exploring hybrid bonding for quantum‑ready processors. STMicroelectronics, Infineon Technologies, and NXP Semiconductors are developing specialized SoIC solutions for automotive and IoT applications. Equipment suppliers such as Applied Materials and Tokyo Electron provide critical bonding tools, enabling smaller fabless companies like Micron Technology, Renesas Electronics, and ASE’s subsidiary, Advanced Semiconductor Engineering, to offer boutique services. This widening base of specialized players enhances design flexibility and drives incremental innovation across the value chain.

List of Key 3D SoIC Hybrid Bonding for Wafer‑on‑Wafer Stacking Companies Profiled

- TSMC

- Intel

- Samsung Electronics

- ASE Technology Holding

- Amkor Technology

- GlobalFoundries

- SMIC

- IBM

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Micron Technology

- Renesas Electronics

- Applied Materials

- Tokyo Electron

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Wafer-to-Wafer Hybrid Bonding

|

| By Application |

|

AI Accelerators

|

| By End User |

|

Fabless Semiconductor Companies

|

| By Process Technology |

|

Nanometer‑Scale Pitch Bonding

|

| By Integration Level |

|

Logic‑Memory Stacking

|

Regional Analysis: North America

The United States represents the dominant force within the North American market, driven by a concentrated ecosystem of technology giants and innovative startups. Government initiatives aimed at bolstering domestic semiconductor manufacturing are further accelerating the adoption of 3D SoIC hybrid bonding. Focus remains on advanced packaging solutions for AI and high-performance computing.

Canada’s semiconductor sector is steadily gaining traction, benefiting from collaborative research efforts and strategic investments. The country’s strengths in materials science and advanced manufacturing provide a supportive environment for the development and implementation of 3D integration techniques.

Mexico’s proximity to the US market and its established manufacturing infrastructure position it as an increasingly important player. The growth of the automotive industry in Mexico is creating demand for advanced semiconductor packaging solutions, including 3D SoIC hybrid bonding, for electric vehicle applications.

While a smaller market, the Caribbean islands are witnessing a rise in technology adoption, particularly in areas like IoT and telecommunications. The demand for compact and power-efficient electronic devices is creating opportunities for 3D SoIC hybrid bonding solutions in this region.

Europe

Europe presents a dynamic landscape for 3D SoIC hybrid bonding for wafer-on-wafer stacking Market. Several European countries are actively investing in advanced semiconductor technologies to maintain their competitiveness in the global electronics industry. The European Union’s strategic initiatives, such as the European Chips Act, are driving significant investments in R&D and manufacturing capabilities. Key areas of focus include automotive electronics, industrial automation, and healthcare devices. The region’s emphasis on energy efficiency and sustainability aligns well with the benefits of 3D integration in power management and thermal dissipation.

Asia-Pacific

Asia-Pacific is anticipated to be the fastest-growing market for 3D SoIC hybrid bonding for wafer-on-wafer stacking Market. China’s aggressive push for self-sufficiency in semiconductor manufacturing, coupled with the rapid growth of its consumer electronics and automotive sectors, is creating substantial demand. Other key markets in the region, such as South Korea, Taiwan, and Japan, possess mature semiconductor industries and are actively investing in advanced packaging technologies. The region is witnessing strong adoption in mobile devices, AI, and high-performance computing applications.

South America

South America represents a nascent market for 3D SoIC hybrid bonding for wafer-on-wafer stacking Market, but it holds significant potential for future growth. The expanding electronics industry in countries like Brazil and Chile, driven by increasing internet penetration and smartphone adoption, is creating demand for advanced semiconductor packaging solutions. The automotive sector is also a key driver, with the growing production of vehicles requiring more sophisticated electronic components.

Middle East & Africa

The Middle East & Africa is an emerging market with growing opportunities for 3D SoIC hybrid bonding for wafer-on-wafer stacking Market. The region’s increasing investments in infrastructure development, telecommunications, and defense are driving demand for advanced electronic systems. The expansion of the automotive industry and the growing adoption of smart city technologies are also contributing to market growth. While the market is currently small, the potential for future expansion is considerable.

Report Scope

This market research report provides a comprehensive analysis of the 3D SoIC hybrid bonding for wafer-on-wafer stacking Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3D SoIC hybrid bonding for wafer-on-wafer stacking Market?

-> 3D SoIC hybrid bonding for wafer-on-wafer stacking Market was valued at USD 0.95 billion in 2025 and is expected to reach USD 2.35 billion by 2034.

Which key companies operate in 3D SoIC hybrid bonding for wafer-on-wafer stacking Market?

-> Key players include Samsung Electronics, Amkor Technology, GlobalFoundries and ASE, among others.

What are the key growth drivers?

-> Growth is driven by the demand for higher bandwidth and lower power consumption in AI accelerators and high‑performance computing platforms, as well as recent mass‑production announcements by TSMC and strategic partnerships such as Intel’s collaboration with ASE.

Which region dominates the market?

-> The reference material does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include the commercialization of SoIC hybrid bonding technology by major foundries, increased collaboration between semiconductor manufacturers and packaging specialists, and the expansion of process lines to support larger wafer‑on‑wafer stacks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...