MARKET INSIGHTS

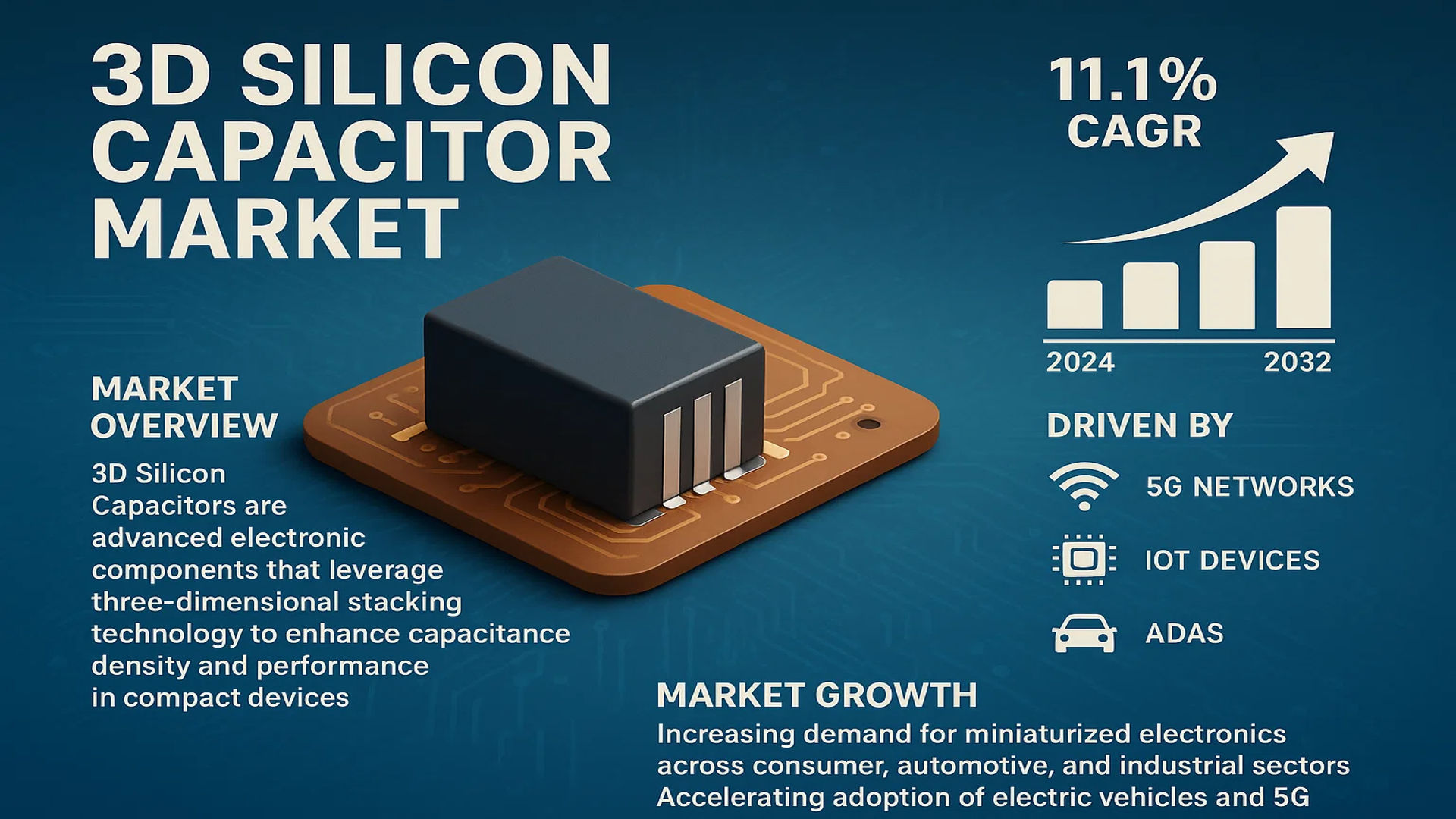

The global 3D Silicon Capacitor Market was valued at 185 million in 2024 and is projected to reach US$ 389 million by 2032, at a CAGR of 11.1% during the forecast period.

3D Silicon Capacitors are advanced electronic components that leverage three-dimensional stacking technology to enhance capacitance density and performance in compact devices. Unlike traditional planar capacitors, these utilize vertical integration of electrodes and dielectrics, enabling superior energy storage in minimal space. The technology is particularly crucial for applications demanding high-frequency performance and miniaturization, such as 5G networks, IoT devices, and advanced driver-assistance systems (ADAS) in automotive electronics.

The market growth is driven by increasing demand for miniaturized electronics across consumer, automotive, and industrial sectors. Furthermore, the rapid adoption of electric vehicles and 5G infrastructure is accelerating demand, as these applications require capacitors with high reliability and power density. Key players like Murata Manufacturing and KYOCERA AVX are investing in R&D to develop next-generation 3D silicon capacitors, further propelling market expansion. For instance, in 2023, Murata launched a new series of ultra-compact 3D silicon capacitors specifically designed for high-frequency RF applications in 5G base stations.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Miniaturization in Electronics to Propel Market Growth

The relentless push for smaller, more powerful electronic devices is a key driver for the 3D silicon capacitor market. Consumer electronics manufacturers are increasingly demanding passive components that offer higher capacitance in smaller footprints. 3D silicon capacitors, with their vertical stacking architecture, provide up to 10 times higher capacitance density compared to traditional planar capacitors. This technology perfectly aligns with the miniaturization trend in smartphones, wearables, and IoT devices, where space optimization is critical. Recent advancements in semiconductor packaging techniques like System-in-Package (SiP) and 3D IC integration are further accelerating adoption of these components.

Electric Vehicle Revolution Creating New Growth Avenues

The automotive industry’s rapid transition toward electrification is generating substantial demand for high-performance power electronics where 3D silicon capacitors excel. Modern electric vehicles require robust energy storage solutions for battery management systems, power converters, and charging infrastructure. 3D silicon capacitors demonstrate superior performance in high-temperature environments and offer the reliability needed in automotive applications. With projections indicating that EVs will account for over 30% of new car sales by 2030, automakers are increasingly incorporating these advanced components into their designs to improve energy efficiency and vehicle range.

MARKET RESTRAINTS

High Manufacturing Costs Limiting Widespread Adoption

While 3D silicon capacitors offer superior performance, their complex fabrication process results in significantly higher production costs compared to traditional MLCCs. The specialized semiconductor processes involved, including deep silicon etching and precision deposition techniques, require expensive equipment and stringent process controls. These costs make 3D silicon capacitors less competitive in price-sensitive applications, particularly in consumer electronics where component cost reduction is paramount. Manufacturers face the ongoing challenge of developing more cost-effective production methods without compromising the performance advantages that justify the premium pricing.

Supply Chain Disruptions Affecting Material Availability

The global semiconductor supply chain complexities are impacting the availability of specialized materials needed for 3D silicon capacitor production. High-purity silicon wafers and advanced dielectric materials face periodic shortages due to capacity constraints at fabrication facilities. The capital-intensive nature of expanding production capacity creates long lead times that can disrupt the supply-demand balance, particularly during periods of increased demand. These supply chain vulnerabilities create uncertainty for manufacturers trying to scale production to meet growing market needs.

MARKET CHALLENGES

Technical Challenges in Scaling Production Capacity

Scaling 3D silicon capacitor manufacturing to meet increasing demand presents several technical hurdles. The precision required in creating three-dimensional structures with nanoscale features makes high-volume production challenging. Yield optimization becomes increasingly difficult as manufacturers attempt to scale, with even minor process variations potentially causing significant performance degradation. Developing reliable testing methodologies for these complex three-dimensional structures also requires substantial R&D investment, creating barriers to entry for new market players.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure Creating New Application Areas

The global rollout of 5G networks presents significant opportunities for 3D silicon capacitor manufacturers. 5G base stations and RF modules require components that can operate at high frequencies while maintaining excellent signal integrity and power efficiency. 3D silicon capacitors’ low parasitic inductance and high-frequency performance make them ideal for these applications. Additionally, the need for compact, high-performance components in millimeter-wave 5G equipment is driving innovation in capacitor designs, with manufacturers developing specialized products tailored to these demanding requirements.

Medical Electronics Offering High-Growth Potential

Advanced medical devices represent another promising growth area for 3D silicon capacitors. Implantable medical devices and diagnostic equipment increasingly require miniature, high-reliability components that can operate in sensitive environments. The biocompatibility and long-term stability of silicon-based capacitors make them particularly suitable for medical applications. Emerging technologies like wireless neural interfaces and portable medical imaging systems are creating new opportunities for specialized capacitor solutions that can meet stringent medical safety standards while delivering exceptional performance.

3D SILICON CAPACITOR MARKET TRENDS

Miniaturization and High-Performance Electronics Driving Market Growth

The global 3D silicon capacitor market is experiencing rapid expansion, largely driven by the increasing demand for miniaturized electronic components with superior performance. Cumulative device shrinkage has become a critical trend in consumer electronics, telecommunications, and automotive industries, where space optimization is paramount. With the 3D silicon capacitor market projected to grow at a CAGR of 11.1% from 2024 to 2032, advancements in semiconductor fabrication techniques are enabling higher capacitance densities in smaller packages compared to traditional 2D capacitors. Vertical stacking technology allows manufacturers to achieve high capacitance values while occupying minimal PCB space, making them indispensable for next-generation electronics.

Other Trends

Rising Adoption in Electric Vehicle Power Electronics

The shift toward electric mobility is catalyzing demand for efficient power management solutions, and 3D silicon capacitors are emerging as a key enabler. Their high energy storage capacity and rapid charge-discharge cycles make them ideal for electric vehicle (EV) applications, particularly in battery management systems (BMS), power converters, and onboard charging modules. With EV sales expected to surpass conventional vehicles in key markets by 2030, the need for compact, high-performance capacitors capable of operating under stringent thermal and voltage conditions is accelerating market adoption.

Integration with Advanced Semiconductor Architectures

System-on-Chip (SoC) and 3D IC packaging technologies are reshaping capacitor integration methodologies. Embedded 3D silicon capacitors eliminate parasitic inductance and reduce mounting space, allowing for seamless integration into microprocessors, RF modules, and high-speed memory applications. As semiconductor nodes continue to shrink below 5nm, the ability to incorporate passive components like capacitors directly into chip architecture – while minimizing signal loss – is becoming increasingly valuable. This trend is particularly evident in telecommunications, where 5G infrastructure demands high-frequency stability and low-loss characteristics.

Growing Demand in Medical Device Miniaturization

Medical electronics represent another burgeoning application sector, where implantable devices and portable diagnostic equipment require compact, high-reliability components. 3D silicon capacitors offer superior performance in medical-grade environments due to their stable capacitance under temperature variations and long operational lifespan. As wearable health monitors and minimally invasive surgical tools become more sophisticated, the demand for these capacitors in the medical sector is expected to grow significantly in the coming decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Capacitor Manufacturers Invest in 3D Silicon Innovation to Capture Market Share

The global 3D silicon capacitor market represents a dynamic competitive environment where established electronics component manufacturers compete with specialized semiconductor firms. Murata Manufacturing currently leads the market, holding approximately 22% of global revenue share in 2024, thanks to its vertically integrated production capabilities and strong relationships with consumer electronics OEMs. The company’s recent investment in Tokyo’s advanced capacitor research facility demonstrates its commitment to maintaining technological leadership.

ROHM Semiconductor and KYOCERA AVX follow closely, collectively accounting for nearly 30% of market share. These companies differentiate themselves through application-specific capacitor solutions, particularly in automotive and industrial sectors where reliability and miniaturization are critical. ROHM’s strategic partnership with a major electric vehicle manufacturer in 2024 highlights the growing importance of 3D silicon capacitors in next-generation transportation.

Mid-sized players like Vishay Intertechnology and Microchip Technology are gaining traction through innovative packaging solutions that enhance thermal performance – a crucial factor for high-density applications. Vishay’s recent breakthrough in 3D capacitor stacking technology has enabled 40% higher capacitance density compared to previous-generation products.

The competitive intensity is further amplified by emerging specialists such as Empower Semiconductor and ELSPES, which focus exclusively on power management applications. These agile innovators are challenging traditional manufacturers through patented architectures specifically designed for 5G infrastructure and AI hardware acceleration.

List of Key 3D Silicon Capacitor Manufacturers Profiled

- Murata Manufacturing (Japan)

- ROHM Semiconductor (Japan)

- KYOCERA AVX (U.S.)

- Vishay Intertechnology (U.S.)

- MACOM (U.S.)

- Microchip Technology (U.S.)

- Skyworks (U.S.)

- Empower Semiconductor (U.S.)

- ELSPES (Germany)

Segment Analysis:

By Type

MOS Capacitors Segment Dominates Due to Superior Integration in Silicon-Based Electronics

The market is segmented based on type into:

- MOS Capacitors (Metal-Oxide-Semiconductor)

- MIS Capacitors (Metal-Insulator-Semiconductor)

- Subtypes: Silicon Nitride, Silicon Dioxide, and others

- High-K Dielectric Capacitors

- Others

By Application

Network and Communication Segment Leads Due to Rising Adoption in 5G Infrastructure

The market is segmented based on application into:

- Network and Communication

- Automotive

- Medical

- Industrial

- Others

By End User

Semiconductor Foundries Lead Adoption for Advanced Chip Integration

The market is segmented based on end user into:

- Semiconductor Foundries

- Consumer Electronics Manufacturers

- Automotive Suppliers

- Telecom Equipment Providers

- Others

Regional Analysis: 3D Silicon Capacitor Market

Asia-Pacific

The Asia-Pacific region dominates the global 3D silicon capacitor market, primarily driven by China, Japan, and South Korea. This region accounts for over 45% of the global market share due to its thriving semiconductor industry and robust electronics manufacturing sector. China, in particular, is experiencing rapid adoption of 3D silicon capacitors in consumer electronics and electric vehicles (EVs). The increasing demand for high-performance, miniaturized components in smartphones, wearable devices, and IoT applications is accelerating growth. Additionally, initiatives such as China’s 14th Five-Year Plan emphasize semiconductor self-sufficiency, further boosting local production of advanced capacitors. While cost sensitivity remains a challenge, the region benefits from strong R&D investments by key players like Murata Manufacturing and ROHM Semiconductor.

North America

North America is a key innovator in the 3D silicon capacitor market, driven by demand from automotive, aerospace, and medical device applications. The U.S. holds the largest market share in the region, supported by leading semiconductor companies such as Vishay Intertechnology and Skyworks. The push for energy efficiency in EVs and data centers is fueling adoption, alongside strict performance requirements in defense and healthcare sectors. Government-funded initiatives, including the CHIPS and Science Act, are expected to enhance domestic semiconductor manufacturing, indirectly benefiting the 3D capacitor sector. However, supply chain disruptions and material costs pose challenges for manufacturers operating in this high-cost region.

Europe

Europe’s 3D silicon capacitor market is characterized by steady growth, supported by stringent environmental regulations and the region’s focus on green technology and Industry 4.0. Germany, France, and the U.K. lead in adoption, particularly in automotive and industrial automation applications. The EU’s Green Deal and circular economy policies encourage innovation in sustainable semiconductor solutions, fostering demand for efficient capacitors. Additionally, partnerships between research institutes and corporations, such as those involving Infineon Technologies, are advancing 3D capacitor integration in power electronics. Despite these drivers, bureaucratic hurdles and high manufacturing costs slow down large-scale deployment compared to Asia-Pacific.

South America

South America remains a nascent but emerging market for 3D silicon capacitors, with Brazil and Argentina representing the primary demand centers. Growth is driven by expanding telecommunications infrastructure and gradual adoption of EVs, though economic instability limits widespread investment. Local manufacturers face challenges in sourcing advanced materials, relying heavily on imports from Asia and North America. Nevertheless, increasing urbanization and government incentives for electronics manufacturing hint at long-term potential, albeit at a slower pace compared to more developed regions.

Middle East & Africa

The Middle East & Africa region shows modest growth in the 3D silicon capacitor market, primarily in the UAE, Saudi Arabia, and Israel. Demand stems from telecommunications, automotive (particularly luxury EVs), and smart city projects. While limited semiconductor infrastructure restricts local production, countries like Israel are investing in semiconductor R&D, supported by startups specializing in advanced capacitor technologies. Africa’s market is still in early stages, with growth hampered by logistical challenges and underdeveloped supply chains. However, foreign investments in tech hubs (e.g., Morocco’s industrial zones) could unlock opportunities in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Global 3D Silicon Capacitor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 185 million in 2024 and is projected to reach USD 389 million by 2032, growing at a CAGR of 11.1%.

- Segmentation Analysis: Detailed breakdown by product type (MOS Capacitors, MIS Capacitors), application (Network & Communication, Automotive, Medical, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates with over 42% market share in 2024.

- Competitive Landscape: Profiles of leading market participants including Murata Manufacturing, ROHM Semiconductor, KYOCERA AVX, Vishay Intertechnology, and others, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies in 3D semiconductor packaging, integration with SoC designs, and advancements in power management for compact electronics.

- Market Drivers & Restraints: Evaluation of factors such as miniaturization trends in electronics, EV market growth, and high manufacturing costs impacting market dynamics.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, electronics OEMs, and investors regarding emerging opportunities in high-density energy storage solutions.

The analysis employs both primary research (industry expert interviews) and secondary research (verified market data) to ensure accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 3D Silicon Capacitor Market?

-> 3D Silicon Capacitor Market was valued at 185 million in 2024 and is projected to reach US$ 389 million by 2032, at a CAGR of 11.1% during the forecast period.

Which key companies operate in Global 3D Silicon Capacitor Market?

-> Key players include Murata Manufacturing, ROHM Semiconductor, KYOCERA AVX, Vishay Intertechnology, MACOM, and Microchip Technology, among others.

What are the key growth drivers?

-> Key growth drivers include demand for miniaturized electronics, growth in electric vehicles, and advancements in semiconductor packaging technologies.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (42% in 2024), driven by semiconductor manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include 3D integration in SoC designs, high-density capacitors for 5G applications, and sustainable manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...