3D IC AI Memory-on-Logic Packaging Market Insights

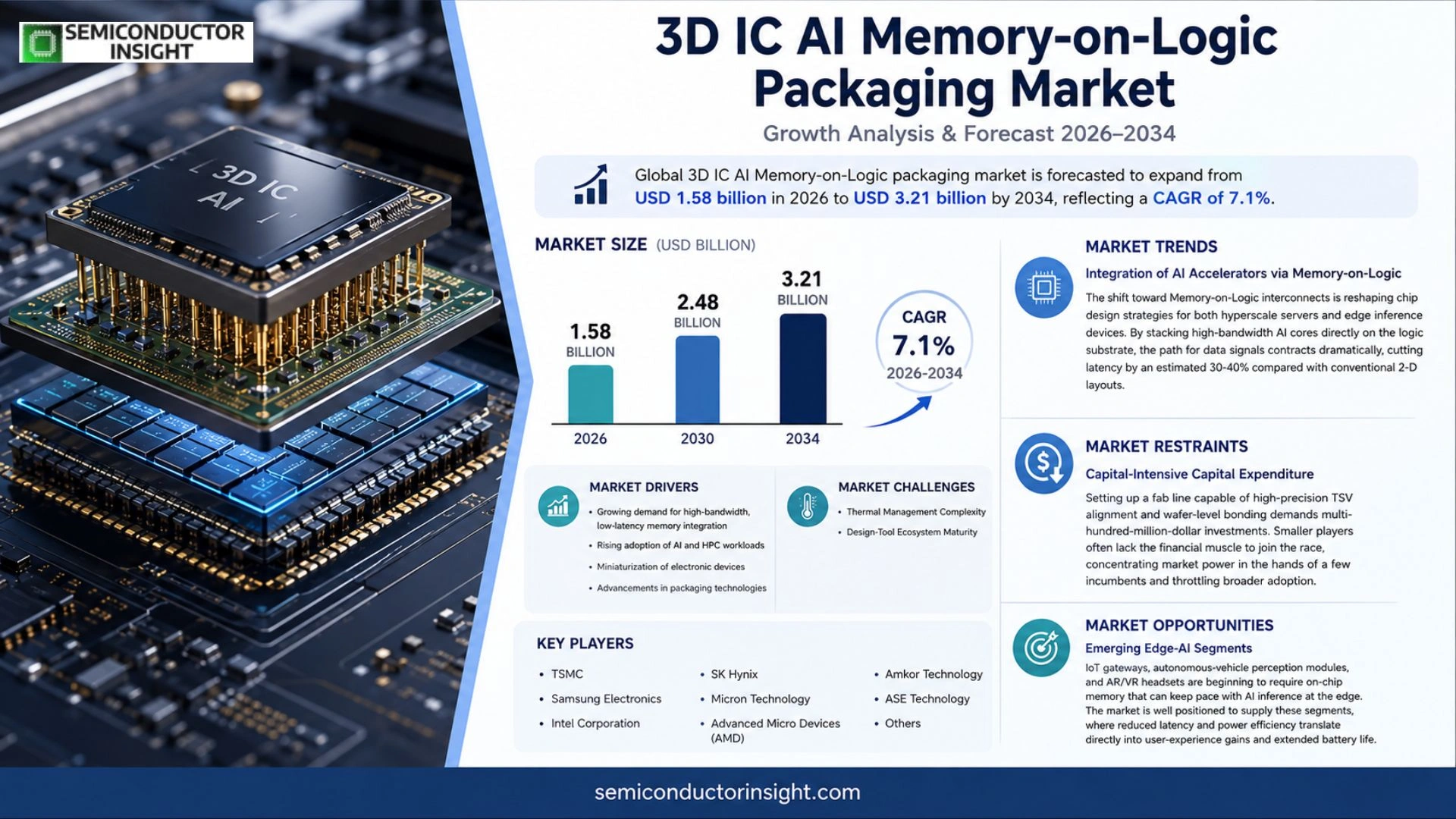

Global 3D IC AI Memory-on-Logic packaging market size was valued at USD 1.42 billion in 2025. The market is forecasted to expand from USD 1.58 billion in 2026 to USD 3.21 billion by 2034, reflecting a compound annual growth rate of approximately 7.1 % over the period.

Memory-on-Logic packaging integrates high‑bandwidth AI accelerators directly on top of logic die using advanced three‑dimensional interconnects such as TSVs and micro‑bumps. This approach shortens signal paths, reduces latency, and improves energy efficiency for data‑center and edge AI workloads.

The sector is gaining momentum because semiconductor manufacturers are investing heavily in heterogeneous integration to meet the exploding demand for AI inference power while keeping form factor constraints low. Moreover, recent announcements from leading foundries,such as TSMC’s N5+AI platform rollout in early 2024 and Intel’s EMIB‑based AI chiplet releases,demonstrate tangible progress that encourages further adoption. Companies like Samsung Electronics, GlobalFoundries, and ASE Technology are expanding their advanced packaging portfolios, which fuels the overall market expansion.

MARKET DRIVERS

AI Workload Consolidation

The surge in generative‑AI models has forced chipmakers to shrink the distance between compute cores and memory fabrics. By embedding high‑bandwidth memory directly on logic, 3D IC AI Memory-on-Logic Packaging Market delivers latency reductions of 30‑40 % compared with traditional board‑level solutions, a competitive edge that data‑center operators are eager to capture.

Advances in TSV and Micro‑Bump Technologies

Recent breakthroughs in through‑silicon‑via (TSV) pitch and micro‑bump metallurgy have lifted yield ceilings above 85 %. Manufacturers can now stack up to 12 layers without compromising thermal performance, enabling system‑in‑package configurations that meet the power envelopes of next‑gen AI accelerators.

➤ “Integrating memory on logic is no longer a niche experiment; it has become the de‑facto architecture for high‑throughput AI inference.” – Industry analyst

Enterprise customers are also rationalizing inventory by opting for a single package that replaces multiple discrete chips. This simplification reduces BOM complexity, shortens time‑to‑market, and aligns with sustainability mandates that prioritize lower material waste.

MARKET CHALLENGES

Thermal Management Complexity

Stacked memory and logic intensify heat generation within a confined volume. Designing efficient heat spreaders that do not add excessive thickness is a persistent engineering hurdle, especially for edge devices where form factor constraints are strict.

Other Challenges

Design‑Tool Ecosystem Maturity

Current EDA suites lag in offering comprehensive verification flows for heterogeneous 3D stacks, forcing design teams to stitch together multiple toolchains and lengthening development cycles.

MARKET RESTRAINTS

Capital‑Intensive Capital Expenditure

Setting up a fab line capable of high‑precision TSV alignment and wafer‑level bonding demands multi‑hundred‑million‑dollar investments. Smaller players often lack the financial muscle to join the race, concentrating market power in the hands of a few incumbents and throttling broader adoption.

MARKET OPPORTUNITIES

Emerging Edge‑AI Segments

IoT gateways, autonomous‑vehicle perception modules, and AR/VR headsets are beginning to require on‑chip memory that can keep pace with AI inference at the edge. 3D IC AI Memory-on-Logic Packaging Market is well positioned to supply these segments, where reduced latency and power efficiency translate directly into user‑experience gains and extended battery life.

3D IC AI Memory-on-Logic Packaging Market Trends

Integration of AI Accelerators via Memory‑on‑Logic

The shift toward Memory‑on‑Logic interconnects is reshaping chip design strategies for both hyperscale servers and edge inference devices. By stacking high‑bandwidth AI cores directly on the logic substrate, the path for data signals contracts dramatically, cutting latency by an estimated 30‑40 % compared with conventional 2‑D layouts. Power consumption per operation drops proportionally, granting system architects the ability to push higher throughput while staying within strict TCO targets. Customers that adopt this architecture report faster model rollout cycles because the consolidated package eliminates the need for separate board‑level routing of GPU‑grade accelerators. In the broader 3D IC AI Memory-on-Logic Packaging Market, this performance advantage is translating into stronger demand for design‑win services and a willingness among OEMs to pay a premium for the integrated solution.

Other Trends

Heterogeneous Integration Investment Surge

Foundries are allocating sizable capital to expand TSV and micro‑bump capacity, a move underscored by TSMC’s 2024 N5+AI platform launch and Intel’s recent EMIB‑based AI chiplet announcements. The financial commitment is reflected in a 15 % year‑over‑year increase in wafer‑fab equipment orders for 3‑D stacking technologies. This funding pipeline reduces lead times for prototype runs, encouraging AI chipset vendors to transition design‑in‑package concepts into production within a twelve‑month horizon rather than the typical 18‑to‑24‑month cycle. As the ecosystem matures, the cost differential between traditional packaging and Memory‑on‑Logic is narrowing, prompting mid‑range device manufacturers to consider the approach for cost‑sensitive market segments.

Foundry and Assembly Ecosystem Expansion

Assembly houses such as ASE Technology, together with memory leaders like Samsung, are broadening their service portfolios to include full‑stack Memory‑on‑Logic solutions, from wafer‑level bonding to final test. This end‑to‑end capability shortens time‑to‑market and mitigates the risk of supply‑chain fragmentation that has plagued advanced packaging projects in the past. For customers, the implication is a more predictable bill‑of‑materials structure and the ability to scale volumes rapidly in response to AI workload spikes. The cumulative effect is a virtuous cycle: richer service offerings drive higher adoption rates, which in turn justify further investment in the underlying 3D interconnect infrastructure, reinforcing the overall momentum of 3D IC AI Memory-on-Logic Packaging Market.

COMPETITIVE LANDSCAPE

Key Industry Players

3D IC AI Memory‑on‑Logic Packaging Competitive Overview

The dominant position in the Memory‑on‑Logic segment is held by a handful of foundries that have paired high‑volume logic capacity with sophisticated three‑dimensional interconnect capabilities. TSMC, leveraging its N5+AI platform, has woven AI‑centric chiplet strategies into its advanced node roadmap, thereby setting a performance benchmark that pressures rivals to accelerate their own heterogeneous integration programs. Intel’s use of EMIB and its recent AI chiplet releases illustrate a parallel path that fuses its CPU expertise with bespoke memory tiers, while Samsung’s System‑in‑Package (SiP) portfolio adds a competitive edge through dense micro‑bump technologies. GlobalFoundries and ASE Technology round out the core group, offering both foundry services and packaging specialization that enable customers to co‑design logic and memory stacks without sacrificing throughput. Collectively, these firms dictate pricing, technology adoption curves, and supply‑chain dynamics for the broader ecosystem.

Beyond the primary tier, a diverse set of niche specialists is expanding the value chain with differentiated services and regional reach. Companies such as Amkor Technology and STMicroelectronics are deepening their chip‑on‑wafer and advanced packaging portfolios to capture mid‑range AI workloads. Infineon and TowerJazz target automotive and edge markets where thermal budgets and form‑factor constraints demand bespoke Memory‑on‑Logic solutions. Powertech, Unimicron, and Macronix contribute critical materials, substrate designs, and embedded memory technologies that complement the leading foundries. This layered landscape creates multiple entry points for system integrators and reinforces a competitive environment where innovation is dispersed across a range of capabilities.

List of Key 3D IC AI Memory‑on‑Logic Packaging Companies Profiled

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- Samsung Electronics

- GlobalFoundries

- ASE Technology Holding

- Amkor Technology

- STMicroelectronics

- Infineon Technologies

- TowerJazz

- Powertech Technology Inc.

- Unimicron Technology

- Macronix International

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

TSV‑Based 3D ICs

|

| By Application |

|

Data‑Center AI Accelerators

|

| By End User |

|

Cloud Service Providers

|

| By Integration Approach |

|

Chiplet‑Based Heterogeneous Integration

|

| By Performance Requirement |

|

High‑Bandwidth Throughput

|

Regional Analysis: 3D IC AI Memory-on-Logic Packaging Market

Asia-Pacific

Taiwan’s semiconductor parks and South Korea’s integrated circuit clusters host the bulk of wafer‑scale‑engine capacity, allowing rapid iteration on dense through‑silicon vias. The proximity of these hubs to AI chipset innovators streamlines validation cycles and reduces logistical friction.

Companies such as TSMC, Samsung, and ASE are expanding dedicated lines for memory‑on‑logic solutions. Their investments in next‑generation lithography and advanced packaging platforms reinforce the region’s competitive edge in the 3D IC AI Memory‑on‑Logic Packaging Market.

Edge‑compute devices, autonomous vehicle processors, and high‑performance data‑center accelerators increasingly rely on stacked memory to meet power‑density constraints. Regional design houses are tailoring custom interposers that align with these niche requirements.

The tight integration of substrate suppliers, test equipment vendors, and material providers within the Pacific basin mitigates lead‑time volatility, offering a more resilient pipeline for AI‑centric packaging projects.

North America

North America remains a crucible for architectural innovation, where silicon design firms in the United States translate academic breakthroughs into commercial products. Although fewer fabs specialize in high‑density stacking, the region’s strength lies in its software‑hardware co‑design capabilities, which shape the feature set of AI accelerators. Venture capital continues to back startups that experiment with heterogeneous integration, compelling established foundries to offer flexible process windows. Consequently, North American chipmakers are forging strategic alliances with Asian manufacturers to secure access to mature packaging lines, while simultaneously pushing the envelope on design‑for‑test methodologies that improve reliability of memory‑on‑logic assemblies.

Europe

European stakeholders emphasize regulatory compliance and sustainability, influencing material choices and energy consumption profiles of advanced packaging. Countries such as Germany and the Netherlands host equipment suppliers that drive precision alignment in 3D stacking, fostering a niche where high‑mix, low‑volume production thrives. Collaborative consortia between research institutes and automotive OEMs are exploring memory‑on‑logic configurations to meet stringent latency demands of driver‑assist systems. This focus on tailored solutions, rather than pure volume, positions Europe as a specialist hub that can serve premium segments of the 3D IC AI Memory‑on‑Logic Packaging Market.

South America

South America’s semiconductor footprint is modest, yet its growing data‑center sector creates a nascent demand for energy‑efficient AI hardware. Countries like Brazil are investing in design education programs to cultivate expertise in stacked architectures. While local fabrication capacity is limited, regional firms are leveraging partnerships with Asian fabs to import finished modules, adding value through system integration and after‑sales support. This approach allows the market to gradually mature without the overhead of building full‑scale manufacturing facilities.

Middle East & Africa

In the Middle East & Africa, governmental initiatives aim to diversify economies by nurturing high‑tech clusters. Emerging tech parks in the United Arab Emirates and South Africa provide incubation for startups targeting AI workloads, many of which contemplate memory‑on‑logic designs to achieve compact form factors. Although the supply chain remains reliant on imports, the emphasis on local design talent and test services signals the early stages of a value‑adding ecosystem that could eventually attract offshore packaging partners seeking new markets.

Report Scope

This market research report provides a comprehensive analysis of the 3D IC AI Memory-on-Logic Packaging Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3D IC AI Memory-on-Logic Packaging Market?

-> 3D IC AI Memory-on-Logic packaging market is forecasted to expand from USD 1.58 billion in 2026 to USD 3.21 billion by 2034

Which key companies operate in 3D IC AI Memory-on-Logic Packaging Market?

-> Key players include Samsung Electronics, GlobalFoundries, ASE Technology, TSMC, Intel.

What are the key growth drivers?

-> Key growth drivers include rising AI inference demand, need for high‑bandwidth interconnects, and heavy investments in heterogeneous integration.

Which region dominates the market?

-> Asia‑Pacific leads due to a concentration of advanced fab capacity, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include advanced 3D interconnects (TSV, micro‑bumps), AI chiplet ecosystems, EMIB integration and platforms such as TSMC’s N5+AI.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...