3D heterogeneous integrated Lidar receiver chip with SPAD array Market Insights

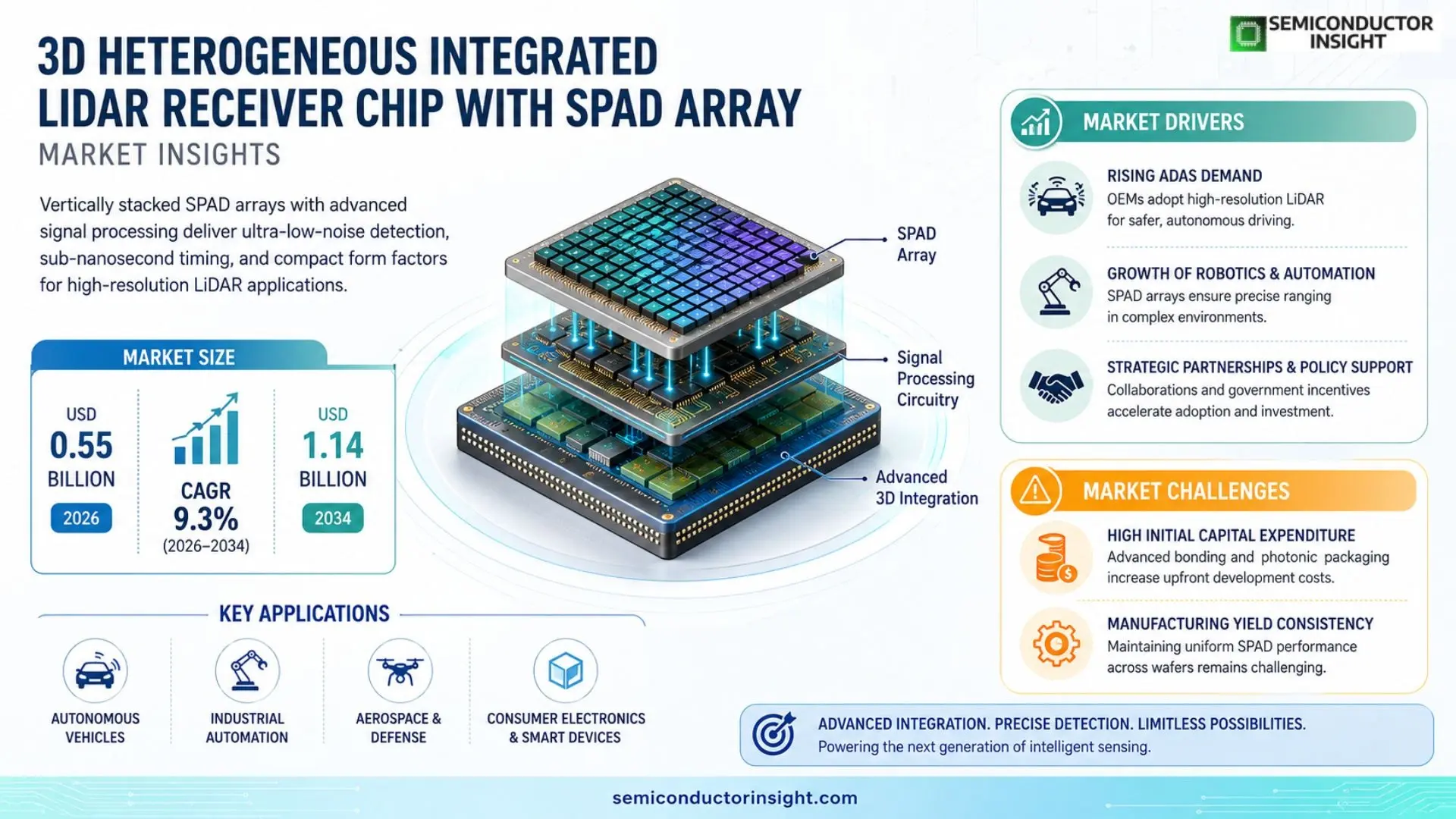

Global 3D heterogeneous integrated Lidar receiver chip with SPAD array market size was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.55 billion in 2026 to USD 1.14 billion by 2034, exhibiting a CAGR of 9.3 % during the forecast period.

A 3D heterogeneous integrated Lidar receiver chip combines vertically stacked semiconductor layers that integrate a Single‑Photon Avalanche Diode (SPAD) array with advanced signal‑processing circuitry on a single substrate. This architecture enables ultra‑low‑noise photon detection, sub‑nanosecond timing resolution, and compact form factors essential for high‑resolution ranging and imaging applications in autonomous vehicles, robotics, and aerospace.

The market is accelerating because automotive OEMs are scaling production of driverless platforms, while defense programs demand reliable long‑range sensing under adverse conditions. Furthermore, advances in silicon photonics and wafer‑level bonding are reducing unit costs, encouraging broader adoption across consumer electronics and industrial automation sectors.

MARKET DRIVERS

Rising Demand for Advanced Driver‑Assistance Systems (ADAS)

The rapid integration of ADAS in passenger and commercial vehicles is compelling OEMs to adopt high‑resolution Lidar solutions. 3D heterogeneous integrated Lidar receiver chip with SPAD array Market benefits from this trend as manufacturers seek compact, low‑power sensors that can deliver centimeter‑level depth accuracy.

Growth of Robotics and Automation

Industrial robotics, warehouse automation, and mobile robots require precise ranging in cluttered environments. Photon‑counting SPAD arrays enable reliable operation under varying lighting conditions, positioning 3D heterogeneous integrated Lidar receiver chip with SPAD array Market as a preferred technology for these sectors.

➤ Strategic partnerships between semiconductor foundries and automotive Tier‑1 suppliers are accelerating time‑to‑market for next‑generation Lidar modules.

In parallel, government incentives for low‑emission transportation and safety‑critical infrastructure are fostering capital investment, reinforcing steady revenue growth for vendors operating within 3D heterogeneous integrated Lidar receiver chip with SPAD array Market.

MARKET CHALLENGES

High Initial Capital Expenditure

The development of heterogeneous integration platforms demands sophisticated wafer‑scale bonding and advanced photonic packaging, driving up‑front costs that can deter early‑stage entrants and slow scale‑up for established players.

Other Challenges

Manufacturing Yield Consistency

Achieving uniform SPAD performance across large wafers remains difficult, leading to yield variability that can affect pricing competitiveness and delivery schedules.

MARKET RESTRAINTS

Regulatory and Safety Certification Barriers

Stringent functional‑safety standards such as ISO 26262 and emerging Lidar‑specific regulations require extensive validation. The time‑intensive certification process can delay product launches, especially for startups lacking dedicated compliance resources.

MARKET OPPORTUNITIES

Emergence of 5G‑Enabled Edge Computing

The convergence of 5G connectivity with edge‑AI processing opens new use‑cases for real‑time 3D perception in smart cities and autonomous drones. Integrating SPAD‑based Lidar receivers at the edge reduces latency and bandwidth costs, presenting a lucrative growth avenue for stakeholders in 3D heterogeneous integrated Lidar receiver chip with SPAD array Market.

3D heterogeneous integrated Lidar receiver chip with SPAD array Market Trends

Rise of Integrated Photon Detection in Autonomous Systems

3D heterogeneous integrated Lidar receiver chip with SPAD array is gaining traction as manufacturers seek ultra‑low‑noise photon detection and sub‑nanosecond timing resolution. By vertically stacking semiconductor layers, the architecture merges a SPAD array with signal‑processing circuitry on a single substrate, delivering compact form factors essential for high‑resolution ranging. Automotive OEMs are expanding driverless platform production, creating a clear demand for sensors that can operate reliably in varied lighting conditions. Simultaneously, defense programs require long‑range sensing that tolerates adverse environments, reinforcing the technology’s strategic importance across multiple high‑value sectors.

Other Trends

Cost Reduction through Wafer‑Level Bonding

Advances in silicon photonics and wafer‑level bonding techniques are directly lowering the unit cost of 3D heterogeneous integrated Lidar receiver chips. These processes enable precise alignment of stacked layers while maintaining high yield, which translates into more affordable solutions for consumer electronics and industrial automation. As a result, manufacturers are increasingly confident in scaling production beyond niche automotive and defense markets, opening pathways for integration into robotics, drones, and smart infrastructure where cost sensitivity has previously limited adoption.

Expanding Applications beyond Automotive

Beyond the automotive sphere, the market is witnessing rapid entry into robotics, aerospace, and high‑precision manufacturing. The ability to deliver reliable photon detection in compact packages makes the technology suitable for drone navigation and satellite‑based remote sensing, where payload weight and power consumption are critical constraints. Industrial automation firms are also leveraging the high‑resolution imaging capabilities for quality inspection and predictive maintenance, further diversifying the demand landscape and reinforcing the long‑term growth trajectory of 3D heterogeneous integrated Lidar receiver chip with SPAD array market.

COMPETITIVE LANDSCAPE

Key Industry Players

Emerging Landscape of 3D Heterogeneous Integrated Lidar Receivers

The market is currently anchored by a handful of vertically integrated semiconductor firms that have mastered 3‑D stacking and SPAD‑array fabrication. Lumentum Holdings leads the space, leveraging its legacy in high‑performance photonics to deliver wafer‑level bonded receiver chips with sub‑nanosecond timing. Bosch and Sony follow closely, combining deep automotive sensor expertise with silicon‑photonic integration platforms that enable volume‑scalable production for autonomous‑vehicle OEMs. These incumbents dictate pricing dynamics and set reference architectures, shaping a market structure that blends high‑margin niche applications (defense, aerospace) with rapidly expanding automotive volume.

Beyond the tier‑one players, a broad cohort of niche innovators is accelerating adoption through differentiated form‑factors or specialized process nodes. Companies such as Velodyne Lidar, Luminar Technologies, and Aeva are integrating SPAD arrays with proprietary signal‑processing ASICs to target long‑range perception. Start‑ups like Ouster and Quanergy focus on modular, cost‑optimized modules for robotics and industrial automation. Traditional semiconductor foundries—including Texas Instruments, STMicroelectronics, and GlobalFoundries—offer multi‑project wafer services that lower entry barriers for emerging players. Meanwhile, optics specialists like Lattice and AMS supply custom photonic IP, reinforcing a collaborative ecosystem that fuels rapid technology diffusion.

List of Key 3D Heterogeneous Integrated Lidar Receiver Chip with SPAD Array Companies Profiled

- Lumentum Holdings

- Bosch Sensortec

- Sony Semiconductor

- Velodyne Lidar

- Luminar Technologies

- Aeva

- Ouster Inc.

- Quanergy Systems

- Texas Instruments

- STMicroelectronics

- GlobalFoundries

- AMS AG

- Panasonic Automotive Solutions

- Intel (Mobileye)

- Sharp Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hybrid SPAD Integration

|

| By Application |

|

Autonomous Vehicles

|

| By End User |

|

Automotive OEMs

|

| By Technology |

|

Wafer‑Level Bonding

|

| By System Architecture |

|

Heterogeneous Multi‑Chip Module

|

Regional Analysis: North America

The automotive industry represents the largest application segment for 3D heterogeneous integrated Lidar receiver chips with SPAD array in North America. The drive towards full autonomy necessitates high-resolution, long-range 3D perception, making these chips essential for ADAS and autonomous driving systems.

The expanding robotics market, particularly in industrial automation and logistics, is a significant driver. 3D Lidar enables robots to perceive their surroundings with greater accuracy, facilitating navigation, object recognition, and manipulation tasks. Integration with artificial intelligence algorithms further enhances the capabilities of these robotic systems.

Applications in aerospace and defense, including surveillance, mapping, and target detection, are fostering demand. The need for robust and reliable 3D sensing in challenging environments is a key factor driving adoption in this sector.

The growth of AR/VR applications, encompassing gaming, enterprise training, and industrial design, is creating a demand for precise 3D environment mapping and user tracking capabilities. 3D Lidar plays a vital role in enhancing the immersive experience and enabling accurate spatial interaction.

Europe

Europe is witnessing steady growth in 3D heterogeneous integrated Lidar receiver chip with SPAD array Market, primarily driven by the automotive industry’s increasing focus on ADAS and electrification. Stringent safety regulations and a growing emphasis on autonomous driving technologies are propelling demand. The region’s strong innovation ecosystem, particularly in Germany, France, and the UK, is fostering advancements in Lidar technology. Furthermore, the aerospace and defense sectors in Europe represent a significant application area, with ongoing investments in surveillance and security systems.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for 3D heterogeneous integrated Lidar receiver chips with SPAD array. The region’s burgeoning automotive industry, particularly in China and Japan, is a key driver. Government initiatives promoting the development of autonomous vehicles and smart cities are further fueling market expansion. The increasing adoption of 3D Lidar in robotics, industrial automation, and consumer electronics is also contributing to growth in this region.

United States

The United States represents a substantial market for 3D heterogeneous integrated Lidar receiver chips with SPAD array, with strong adoption across automotive, robotics, and defense sectors. Significant investments in autonomous driving research and development, coupled with a supportive regulatory environment, are driving market growth. The region’s leading technology companies are actively involved in the development and deployment of advanced Lidar systems.

South America

South America is an emerging market with potential for growth, driven by increasing investments in infrastructure development and the growing adoption of automotive technologies. The commercial and industrial sectors are also expected to contribute to the demand for 3D Lidar solutions in the coming years.

Middle East & Africa

The Middle East & Africa region presents a niche market with potential growth in specific sectors like defense and security. Increasing investments in smart city initiatives and the development of autonomous transportation solutions are expected to drive demand for 3D Lidar technology in the long term.

Report Scope

This market research report provides a comprehensive analysis of the 3D heterogeneous integrated Lidar receiver chip with SPAD array Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3D heterogeneous integrated Lidar receiver chip with SPAD array Market?

-> 3D heterogeneous integrated Lidar receiver chip with SPAD array Market was valued at USD 0.48 billion in 2025 and is expected to reach USD 1.14 billion by 2034, reflecting a CAGR of 9.3 % over the forecast period.

Which key companies operate in 3D heterogeneous integrated Lidar receiver chip with SPAD array Market?

-> Key players include Lumentum Holdings, Finisar (II‑VI), STMicroelectronics, AMS, Sony, and other semiconductor and photonics innovators, among others.

What are the key growth drivers?

-> Key growth drivers include scaling of autonomous‑vehicle platforms, defense demand for long‑range sensing, advances in silicon photonics and wafer‑level bonding that lower costs, and expanding applications in consumer electronics and industrial automation.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia‑Pacific is the fastest‑growing region driven by strong automotive and electronics manufacturing activity.

What are the emerging trends?

-> Emerging trends include AI/ML‑enhanced signal processing, CMOS‑compatible SPAD array integration, and wafer‑scale heterogeneous integration techniques that improve performance and reduce form factor.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...