3C Precision Metal Components Market Insights

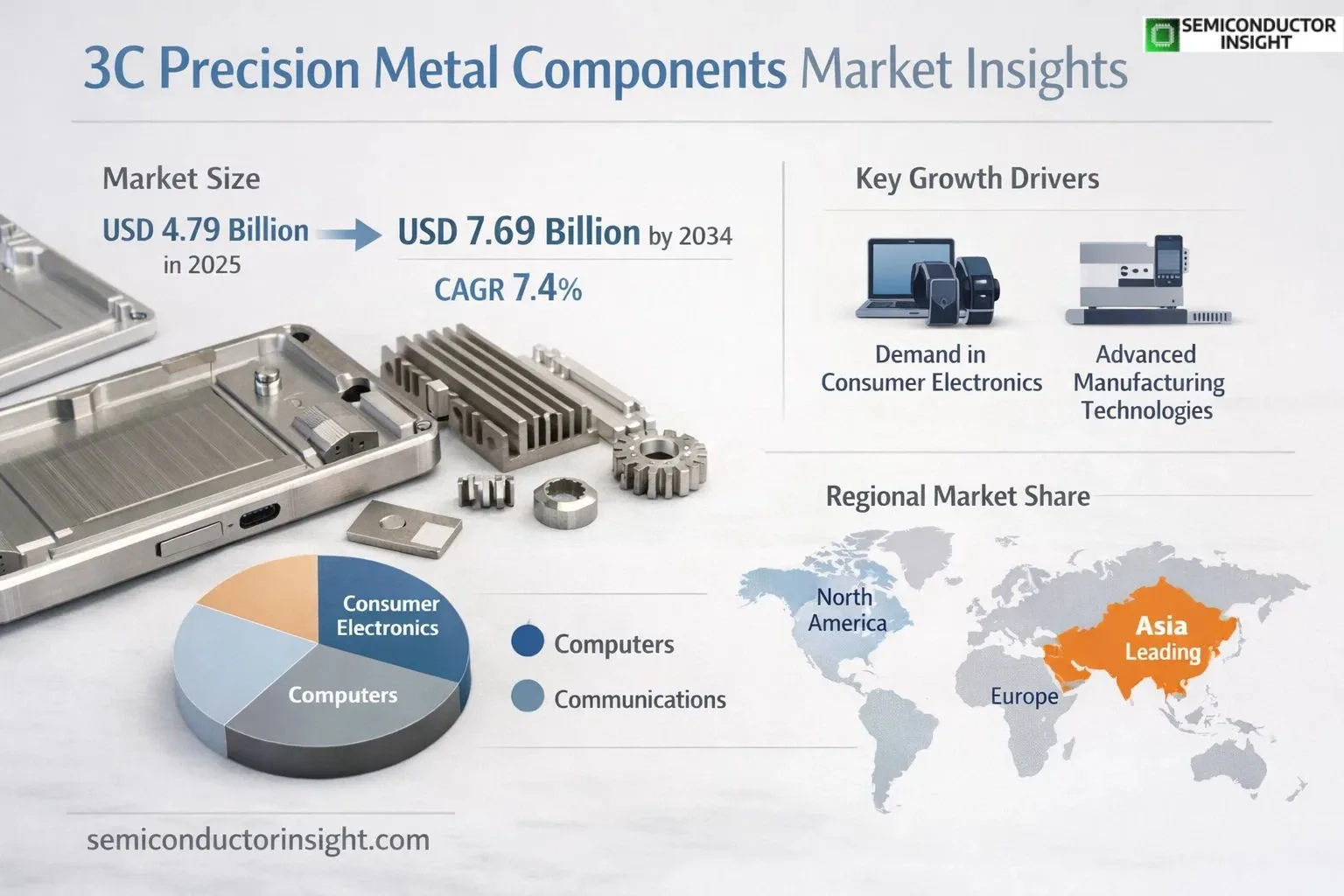

Global 3C Precision Metal Components market size was valued at USD 4.79 billion in 2025. The market is projected to grow from USD 5.15 billion in 2026 to USD 7.69 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period.

3C precision metal components refer to high-precision parts used in computers, communications, and consumer electronics applications. These components are manufactured with tight tolerances to meet the demands of miniaturization, lightweight design, and high performance in modern electronic devices. Key materials include stainless steel, aluminum alloys, and titanium alloys.

The market growth is driven by increasing demand for compact electronic devices, advancements in manufacturing technologies like CNC machining and metal injection molding, and the proliferation of smart devices globally. While China dominates production with its established manufacturing ecosystem, North America and Europe remain significant markets for high-end precision components used in premium electronics.

MARKET DRIVERS

Growing Demand in Consumer Electronics

The 3C Precision Metal Components Market is experiencing steady growth driven by increasing demand for high-performance components in smartphones, laptops, and wearables. Major electronics manufacturers require tighter tolerances and superior surface finishes, pushing adoption of precision metal parts. The market grew approximately 7.2% year-over-year as devices incorporate more metal for durability and thermal management.

Advancements in Manufacturing Technologies

Investment in CNC machining, laser cutting, and micro-milling enables production of complex geometries needed for modern 3C devices. Automation improvements have reduced production costs by 15-20% while maintaining micron-level precision. These technological advancements make precision metal components more accessible across price segments.

➤ Leading manufacturers report that over 60% of new device designs now incorporate at least 5 precision metal components, up from 40% five years ago

The miniaturization trend continues to drive innovation, with component sizes shrinking 30% on average while maintaining structural integrity. This creates ongoing demand for advanced metal forming and finishing techniques.

MARKET CHALLENGES

Supply Chain Volatility

Unstable raw material prices for aluminum alloys, stainless steel, and specialty metals create pricing pressures in the 3C Precision Metal Components Market. Lead times for certain alloys have extended by 2-3 weeks compared to pre-pandemic levels, impacting production schedules.

Other Challenges

Quality Control Demands

Maintaining consistent quality across high-volume production runs remains challenging, with defect rates needing to stay below 0.5% to meet industry standards. This requires significant investment in inspection equipment and skilled technicians.

MARKET RESTRAINTS

High Initial Capital Requirements

The 3C Precision Metal Components Market faces barriers to entry due to substantial equipment costs. A full-scale production line requires $2-5 million investment in CNC machines, surface treatment systems, and quality control instruments. This limits participation primarily to established manufacturers with significant resources.

MARKET OPPORTUNITIES

Emerging Applications in AR/VR Devices

The growing augmented and virtual reality sector presents new opportunities for precision metal components, particularly in headset frames and heat dissipation solutions. Industry projections suggest AR/VR could account for 12-15% of the 3C Precision Metal Components Market by 2026, up from 5% currently.

MAIN TITLE HERE (3C Precision Metal Components Market) Trends

Growing Demand for Miniaturized Components in 3C Sector

The 3C Precision Metal Components Market is witnessing significant demand for ultra-precise, miniaturized parts as consumer electronics continue trending toward compact designs. Manufacturers are focusing on micron-level tolerances to meet requirements for smartphones, wearables, and IoT devices. Advanced CNC machining and micro-stamping technologies enable production of components with sub-millimeter features while maintaining structural integrity.

Other Trends

Material Innovation for Enhanced Performance

Leading manufacturers are developing specialized aluminum alloys and stainless steel variants optimized for 5G device shielding and heat dissipation. These materials maintain strength at reduced thicknesses while meeting electromagnetic compatibility requirements. Titanium alloys are gaining traction for premium devices due to their exceptional strength-to-weight ratio and corrosion resistance.

Regional Supply Chain Realignment

The market is experiencing geographic shifts in production, with Southeast Asian facilities expanding capacity to complement traditional manufacturing hubs in China. This diversification aims to mitigate supply chain risks while maintaining cost competitiveness. Automated production lines are being deployed globally to ensure consistent quality standards across manufacturing locations.

Integration with Advanced Manufacturing Technologies

Industry leaders are implementing AI-driven quality control systems that detect microscopic defects in real-time during production. Additive manufacturing is being adopted for prototyping complex geometries, though traditional subtractive methods remain dominant for mass production. The convergence of these technologies is reducing time-to-market for new component designs.

Sustainability Considerations in Metal Component Production

Environmental regulations are driving adoption of closed-loop water recycling systems in machining processes and the development of recyclable alloy formulations. Major suppliers are obtaining ISO 14001 certifications, with some pioneering carbon-neutral production initiatives through renewable energy adoption in their facilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Global 3C Precision Metal Components Market Leaders and Challengers

The 3C precision metal components market is dominated by Asia-based manufacturers, particularly Chinese firms that control approximately 45% of global production capacity. LeadTech International has emerged as the market leader with comprehensive capabilities in aluminum alloy and stainless steel components for smartphones and laptops. The top five players collectively hold about 32% market share, indicating a moderately concentrated industry structure with significant competition among mid-sized specialists.

Regional challengers like IPE Group Limited have gained traction through partnerships with consumer electronics OEMs, while precision engineering firms such as Suzhou Heaten specialize in ultra-thin alloy components for wearables. The market also features several technology-focused manufacturers investing in microfabrication capabilities to meet the increasing demand for miniaturized components in next-generation 3C products.

List of Key 3C Precision Metal Components Companies Profiled

- LeadTech International

- Freewon

- Suzhou Heaten

- GUANGDONG RUIHUI INTELLIGENT TECHNOLOGY

- IPE Group Limited

- Huizhi Precision

- Panwell

- Allwell Cast

- Foxconn Precision Components

- Jabil Circuit

- Shenzhen Everwin Precision Technology

- BYD Electronic

- Luxshare Precision

- Compeq Manufacturing

- Nanfang Precision

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Aluminum Alloy Components are gaining traction due to their optimal balance of lightweight properties and structural integrity:

|

| By Application |

|

Communications sector demonstrates the most dynamic requirements driving precision metal component innovation:

|

| By End User |

|

OEMs dominate demand due to tight integration requirements and quality standards:

|

| By Manufacturing Process |

|

CNC Machining remains the most versatile process for high-mix production:

|

| By Component Function |

|

Shielding Components are experiencing accelerated innovation cycles:

|

Regional Analysis: 3C Precision Metal Components Market

Asia-Pacific

China accounts for over 60% of global 3C precision metal component production, with specialized industrial parks focusing on connector housings, EMI shielding parts, and heat dissipation solutions for electronics. The mature supply network enables rapid prototyping and mass production capabilities unmatched in other regions.

Japan leads in high-tolerance precision components for premium electronics, with manufacturers specializing in ultra-thin metal casings and corrosion-resistant alloys. The keiretsu system ensures tight integration between component suppliers and final assembly plants in the 3C precision metal components market.

Korean manufacturers focus on hybrid metal-polymer composites and nano-surface treatments for foldable devices. The chaebol-owned production facilities maintain vertically integrated supply chains for critical 3C precision metal components, reducing dependency on external suppliers.

Taiwan excels in miniature connectors and antenna components, leveraging world-class CNC machining capabilities. The island’s dense network of specialized workshops caters to global brands needing high-mix, low-volume 3C precision metal components with quick turnaround times.

North America

The North American 3C precision metal components market focuses on high-value specialty parts for defense, medical, and premium consumer electronics. U.S. manufacturers lead in titanium machining and complex geometries requiring aerospace-grade precision. Regional advantages include strong IP protection, advanced automation, and proximity to Silicon Valley’s product development centers. California and Texas host growing clusters of contract manufacturers serving Apple, Dell, and Cisco’s specialized component needs in the 3C precision metal components market.

Europe

European manufacturers specialize in luxury device components and environmentally compliant alloys for the 3C precision metal components market. Germany’s Mittelstand companies produce high-precision mechanical keyboards parts and industrial-grade connector systems. The region benefits from strong vocational training programs ensuring skilled machinists for complex 3C metal component production. REACH compliance and circular economy initiatives drive innovation in recyclable metal alloys.

Middle East & Africa

The Middle East is emerging as a niche player in aluminum casings and heat sinks for data center equipment through strategic JVs with Asian manufacturers. Dubai’s trade-free zones facilitate component redistribution to African markets. South Africa shows potential in copper-based 3C precision metal components for power distribution applications in communication infrastructure.

South America

Brazil maintains localized production of basic 3C precision metal components for regional electronics brands, particularly in brass contacts and zinc alloy housings. Government import substitution policies support domestic manufacturing capabilities, though the market remains dependent on Asian suppliers for advanced alloys and high-tolerance components.

Report Scope

This market research report provides a comprehensive analysis of the 3C Precision Metal Components Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3C Precision Metal Components Market?

-> Global 3C Precision Metal Components Market was valued at USD 4788 million in 2025 and is projected to reach USD 7687 million by 2034, growing at a CAGR of 7.4% during the forecast period.

Which key companies operate in 3C Precision Metal Components Market?

-> Key players include LeadTech International, Freewon, Suzhou Heaten, GUANGDONG RUIHUI INTELLIGENT TECHNOLOGY, IPE Group Limited, Huizhi Precision, Panwell, and Allwell Cast, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for miniaturization in 3C products, technological advancements in metal component manufacturing, and rising adoption of high-precision parts in consumer electronics.

Which region dominates the market?

-> Asia is the fastest-growing region, particularly China, while North America remains a significant market.

What are the main application segments?

-> The main application segments are Computers, Communications, and Consumer Electronics, which collectively account for the majority of market demand.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...