10G-PON Chips Market Insights

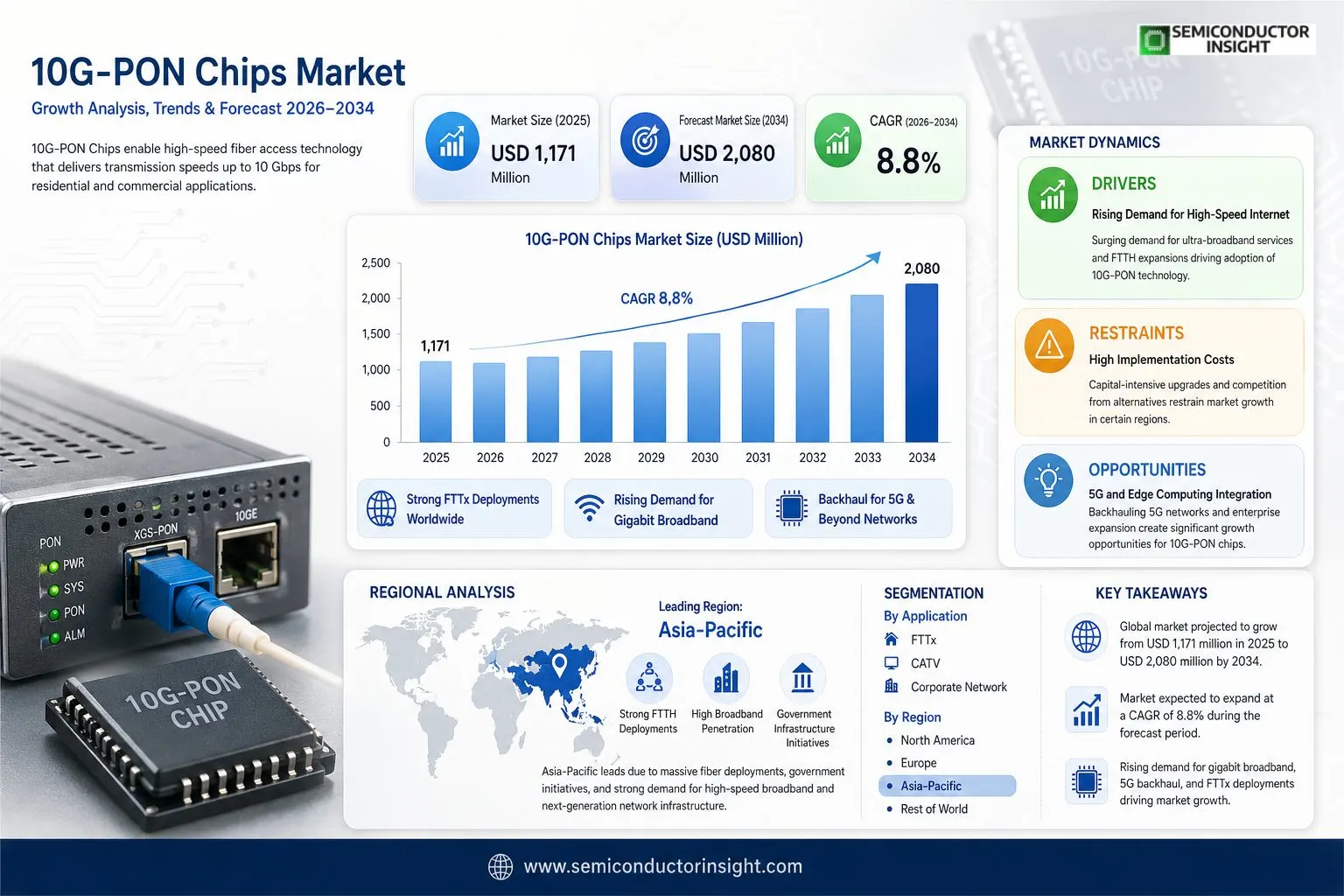

Global 10G-PON Chips market size was valued at USD 1,171 million in 2025. The market is projected to reach USD 2,080 million by 2034, exhibiting a CAGR of 8.8% during the forecast period.

10G-PON Chips enable high-speed fiber access technology that delivers transmission speeds of up to 10 Gbps for residential and commercial applications. Compared with previous generations of fixed access technologies, 10G-PON networks represent major advancements in bandwidth, user experience, and connection capacity. Uplink and downlink rates achieve symmetrical 10 Gbps, while latency drops to less than 100 μs. The PON chipset comprises an EPON/GPON controller, burst mode transceiver, and other optical components; the PON control chip integrates a central processor and hardware accelerator.

The market is experiencing rapid growth due to surging demand for gigabit broadband, widespread FTTx deployments, and the need for robust backhaul in 5G and beyond. Furthermore, government initiatives promoting digital infrastructure worldwide are accelerating adoption. Key players driving innovation include Broadcom, Cortina Access (Realtek), Microchip, Sanechips, Airoha Technology (MTK), Fisilink (Fiberhome), Semtech, and MaxLinear, offering diverse portfolios to meet evolving network requirements.

MARKET DRIVERS

Rising Demand for High-Speed Internet

10G-PON Chips Market is propelled by surging consumer demand for ultra-broadband services, with global fixed broadband subscriptions exceeding 1.4 billion in 2023. Telecom operators are upgrading to 10G-PON technology to deliver symmetrical speeds up to 10 Gbps, supporting bandwidth-intensive applications like 8K streaming and cloud gaming.

FTTH Network Expansions

Major deployments in North America and Asia-Pacific, where FTTH connections grew by 15% annually, drive chip demand. Providers like Verizon and China Telecom invest heavily in XGS-PON infrastructure, necessitating advanced optical chips for ONTs and OLTs to achieve low latency and high efficiency.

➤ Government initiatives, such as the U.S. BEAD program allocating $42 billion for broadband, accelerate 10G-PON adoption worldwide.

Enterprise sectors, including data centers and smart cities, further boost the market as 10G-PON chips enable scalable, cost-effective backhaul solutions over legacy GPON networks.

MARKET CHALLENGES

Interoperability and Compatibility Issues

10G-PON Chips Market faces hurdles in ensuring seamless integration with existing GPON systems, where compatibility mismatches lead to deployment delays. Vendors struggle with varying standards across regions, complicating multi-vendor environments.

Other Challenges

Supply Chain Disruptions

Semiconductor shortages, intensified by geopolitical tensions, have increased lead times for 10G-PON chip production by up to 20%, raising costs for manufacturers and operators.High power consumption in 10G-PON chips poses energy efficiency challenges, particularly in dense urban deployments where cooling and sustainability concerns limit scalability.

MARKET RESTRAINTS

High Implementation Costs

Capital-intensive upgrades restrain 10G-PON Chips Market, with OLT and ONT replacements costing operators 30-50% more than GPON equivalents. Small-scale providers in developing regions hesitate due to ROI timelines exceeding 5 years.Competition from alternatives like cable-based DOCSIS 4.0, offering similar speeds at lower costs, diverts investments away from fiber optics in hybrid networks.Regulatory delays in spectrum allocation and permitting for fiber trenching further slow market penetration, especially in Europe where compliance adds 15-20% to project expenses.

MARKET OPPORTUNITIES

5G and Edge Computing Integration

10G-PON Chips Market holds potential in backhauling 5G networks, with fronthaul traffic projected to grow 25% yearly, enabling low-latency converged servicesExpansion into enterprise private networks and IoT applications in smart cities offers new revenue streams, as 10G-PON chips support massive device connectivity with enhanced security features.Asia-Pacific’s rural broadband push, targeting 300 million new connections by 2025, creates demand for cost-optimized 10G-PON solutions, fostering innovation in chip design for emerging economies.

10G-PON Chips Market Trends

Rising Demand for High-Speed Fiber Access Technologies

10G-PON Chips Market is experiencing robust growth driven by the need for advanced fiber optic networks capable of delivering symmetrical 10Gbps speeds for both residential and commercial applications. This technology represents a significant evolution from previous fixed access generations, offering substantial improvements in bandwidth, user experience, and connection capacity. With uplink and downlink rates reaching up to 10Gbps and latency reduced to under 100 microseconds, 10G-PON chips enable gigabit broadband networks that support bandwidth-intensive services like 8K streaming, cloud gaming, and smart city infrastructures. Key components such as EPON/GPON controllers, burst mode transceivers, and optical elements integrated within PON chipsets facilitate efficient transmission, positioning 10G-PON Chips Market as a cornerstone for next-generation connectivity.

Other Trends

Intensifying Competition Among Leading Manufacturers

In 10G-PON Chips Market, prominent players including Broadcom, Cortina Access (Realtek), Microchip, Sanechips, Airoha Technology (MTK), Fisilink (Fiberhome), Semtech, and MaxLinear are shaping the competitive landscape. These top manufacturers collectively command a substantial revenue share, focusing on innovation in chipset design, hardware accelerators, and central processors to enhance performance. Recent industry surveys highlight ongoing developments, including mergers, acquisitions, and product launches aimed at addressing price pressures, demand fluctuations, and supply chain challenges. This competitive dynamic fosters technological advancements and cost efficiencies, benefiting downstream markets in FTTx deployments.

Growth in Key Application Segments

10G-PON Chips Market shows strong momentum in application areas such as FTTx, CATV, and corporate networks. FTTx remains the leading segment, driven by widespread fiber-to-the-home and fiber-to-the-building initiatives that demand high-capacity PON solutions. Meanwhile, CATV operators leverage 10G-PON chips to upgrade networks for higher video throughput, and corporate networks adopt them for reliable, low-latency enterprise connectivity. Type segments like 10G-GPON and 10G-EPON are gaining traction, with 10G-GPON offering compatibility advantages in existing GPON infrastructures. Regionally, Asia, particularly China, leads adoption due to massive broadband expansions, followed by North America and Europe, where regulatory pushes for fiber infrastructure accelerate deployment. These trends underscore 10G-PON Chips Market’s pivotal role in enabling scalable, future-proof optical access networks amid rising data demands.

COMPETITIVE LANDSCAPE

Key Industry Players

10G-PON Chips Market Leading Manufacturers and Strategic Insights

10G-PON Chips Market is led by established semiconductor giants like Broadcom, which dominates with advanced PON controllers, burst mode transceivers, and integrated optical components enabling symmetrical 10Gbps speeds and low latency under 100μs. The market structure remains moderately concentrated, where the global top five players,Broadcom, Cortina Access (Realtek), Microchip, Sanechips, and Airoha Technology,command a substantial revenue share in 2025, amid robust growth from US$1,171 million to US$2,080 million by 2034 at an 8.8% CAGR. These leaders focus on high-performance chipsets for FTTx, CATV, and corporate networks, driving innovation in hardware accelerators and central processors to meet surging broadband demands.

Complementing the top tier, niche and regional players such as Fisilink (Fiberhome), Semtech, MaxLinear, and Hisense Broadband offer specialized, cost-effective 10G-PON solutions, particularly strong in Asia-Pacific markets like China. These firms emphasize application-specific optimizations for 10G-GPON and 10G-EPON segments, fostering competitive pricing and rapid deployment in emerging networks. The landscape features ongoing mergers, such as Cortina’s integration into Realtek, and R&D investments to counter challenges like supply chain constraints, positioning the sector for expanded global adoption in next-generation fiber access technologies.

List of Key 10G-PON Chips Companies Profiled

- Broadcom

- Cortina Access (Realtek)

- Microchip

- Sanechips

- Airoha Technology (MTK)

- Fisilink (Fiberhome)

- Semtech

- MaxLinear

- Hisense Broadband

- MACOM Technology Solutions

- Centron Technology

- Marvell Semiconductor

- Shanghai Belling

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

10G-GPON leads due to its robust compatibility with existing GPON deployments and support for advanced broadband requirements.

|

| By Application |

|

FTTx dominates as the cornerstone for delivering ultra-high-speed broadband to homes and businesses.

|

| By End User |

|

Telecom Operators spearhead adoption with extensive network upgrade initiatives.

|

| By Chip Function |

|

PON Controllers are pivotal for orchestrating high-speed optical network operations.

|

| By Deployment |

|

ONU/ONT Chips prevail owing to widespread customer-premises deployments.

|

Regional Analysis: 10G-PON Chips Market

Asia-Pacific

Key drivers include rapid urbanization and digital economy growth, compelling telecom providers to deploy 10G-PON chips for ultra-broadband access. Government subsidies for FTTH projects amplify adoption, while consumer shift to remote work and online education boosts demand for reliable, high-capacity networks.

Leading chipmakers from China and South Korea dominate, offering customized ASICs for 10G-PON ONTs and OLTs. Strategic alliances with equipment vendors streamline supply chains, enabling faster market penetration and tailored solutions for diverse operator needs.

Opportunities lie in 5G fixed-wireless convergence and smart city projects, where 10G-PON chips provide robust backhaul. Expanding rural connectivity initiatives open new avenues for cost-effective chip deployments, enhancing overall regional digital inclusion.

Intense competition pressures pricing, while supply chain vulnerabilities from geopolitical tensions pose risks. Regulatory harmonization across countries remains crucial to sustain 10G-PON Chips Market momentum amid evolving standards.

North America

North America exhibits steady growth in 10G-PON Chips Market, driven by mature telecom infrastructures seeking upgrades to meet escalating data demands from hyperscale data centers and enterprise applications. Major operators focus on symmetrical 10G-PON deployments to support business services and residential gigabit internet, leveraging chips with advanced error correction for long-haul performance. Business strategies revolve around vertical integration, where cable MSOs retrofit HFC networks with 10G-PON compatible chips to counter fiber overbuilds. Innovation centers in Silicon Valley pioneer low-latency designs, aligning with edge computing trends. However, high installation costs and regulatory hurdles slow widespread adoption, prompting operators to prioritize urban densification before suburban rollouts. Collaborative R&D with universities accelerates chip miniaturization, ensuring competitiveness in global 10G-PON trends through strategic mergers and IP licensing deals.

Europe

Europe’s 10G-PON Chips Market advances through EU-mandated gigabit connectivity goals, emphasizing sustainable network upgrades across diverse geographies. Operators in Western Europe lead with trials of disaggregated 10G-PON architectures, utilizing versatile chips for multi-operator PON sharing to optimize capex. Eastern Europe’s cost-sensitive markets favor imported chips with high interoperability, supporting rural broadband subsidies. Strategies include cross-border consortia for spectrum-efficient chip development, addressing fragmentation while aligning with green energy directives for power-optimized designs. Challenges persist in legacy copper displacement and varying national regulations, yet public-private partnerships foster innovation in open-access models, positioning Europe as a key player in 10G-PON Chips Market evolution toward unified standards by 2034.

South America

South America emerges as a promising frontier in 10G-PON Chips Market, propelled by urbanization and digital inclusion programs in Brazil and Mexico. Telecom firms deploy 10G-PON chips to bridge urban-rural divides, prioritizing rugged designs resilient to tropical conditions and power fluctuations. Business strategies emphasize affordable chip variants for mass-market FTTH, partnering with regional assemblers to cut logistics costs. Growth hinges on foreign investments funding spectrum auctions and infrastructure sharing, though economic volatility and terrain challenges temper pace. Optimism surrounds e-government initiatives driving demand, with local content rules spurring domestic R&D in 10G-PON integration, gradually elevating South America’s role in broader market dynamics.

Middle East & Africa

The Middle East & Africa region in 10G-PON Chips Market showcases divergent trajectories, with Gulf states investing heavily in smart nation visions via oil-funded fiber rollouts. High-end 10G-PON chips enable luxury residential and hospitality services, featuring AI-enhanced diagnostics for remote management. In Africa, mobile-first markets transition to hybrid fixed-wireless using entry-level chips for community Wi-Fi hubs. Strategies focus on PPPs for scalable deployments, navigating infrastructure gaps with modular chip solutions. Security concerns drive demand for domestically secured components, while talent development programs build local expertise. Despite power and economic hurdles, visionary projects position the region for accelerated 10G-PON adoption aligned with global trends.

Report Scope

This market research report provides a comprehensive analysis of the 10G-PON Chips Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as telecommunications, broadband networks, FTTx, and optical access technologies.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 10G-PON Chips Market?

-> 10G-PON Chips Market was valued at USD 1171 million in 2025 and is expected to reach USD 2080 million by 2034, at a CAGR of 8.8% during the forecast period.

Which key companies operate in 10G-PON Chips Market?

-> Key players include Broadcom, Cortina Access (Realtek), Microchip, Sanechips, Airoha Technology (MTK), Fisilink (Fiberhome), Semtech, MaxLinear, among others.

What are the key growth drivers?

-> Key growth drivers include demand for high-speed fiber access technology up to 10Gbps, improvements in bandwidth, user experience, and connection capacity for residential and commercial applications.

Which region dominates the market?

-> Asia, particularly China, is a key market, with significant presence in North America including the U.S.

What are the emerging trends?

-> Emerging trends include symmetrical 10Gbps uplink and downlink rates, latency reduced to less than 100μs, and advanced PON chipsets with EPON/GPON controllers and burst mode transceivers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...