VCSEL Laser Diode Market to Surge from $1.89 Billion (2024) to $4.12 Billion by 2032: U.S. Holds 38 % Share While China Accelerates at 15.3 % CAGR

Why the VCSEL Moment Is Now

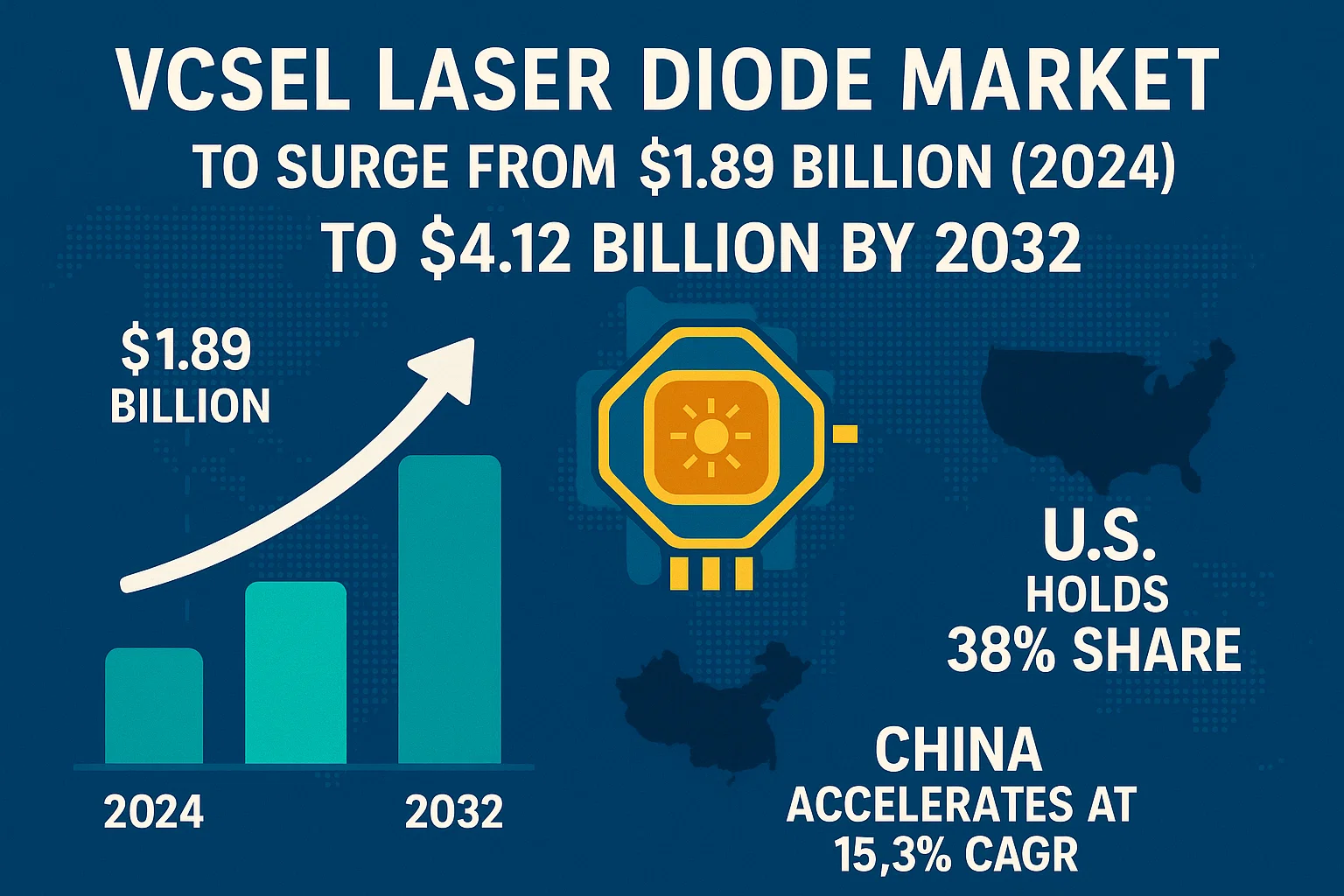

Vertical-cavity surface-emitting lasers (VCSELs) entered the mainstream two decades ago, quietly powering optical mice and short-reach datacom links. Today they stand at the center of a much bigger drama. From Face ID to in-cabin automotive lidar, VCSELs are enabling the machines around us to perceive depth, measure distance, and transfer data at terabit speeds—often inside devices you can slip into a pocket. Analysts now peg the global VCSEL laser-diode market at US $ 1.89 billion in 2024, and—on the back of rapid technology and application wins—project it will more than double to US $ 4.12 billion by 2032, a compound annual growth rate (CAGR) of 10.2 % between 2025 and 2032. The United States currently commands a 38 % revenue share (≈ US $ 456 million), but China is the headline growth story with a 15.3 % CAGR expected through 2032.

Market Snapshot: Bigger, Broader, Deeper

| Metric | 2024 | 2032 (Forecast) | CAGR (2025-2032) |

| Global revenue | US $1.89 B | US $4.12 B | 10.2 % |

| U.S. share | 38 % (US $456 M) | 32 % (share erosion expected) | 7.5 % |

| China share | 22 % | 30 % | 15.3 % |

Growth is no longer confined to 3D-sensing in smartphones. The new demand drivers are:

- Automotive lidar and driver-monitoring systems

- AI servers and next-gen optics for data centers

- AR/VR and spatial-computing headsets

- Biomedical imaging—especially optical-coherence tomography (OCT)

- Industrial position sensing and proximity detection

U.S. Leads… for Now

Silicon-Valley fabs and III-V foundry clusters in Arizona, Texas, and New York helped the United States build a commanding early lead. Apple’s use of GaAs VCSEL arrays for Face ID precipitated a wave of capital investment dating back to 2017, and U.S. fabs still dominate premium 940 nm parts. But that moat is narrowing. Why?

- China’s fab-first policy: Supported by low-interest loans and tax holidays, half a dozen “IDMs-in-the-making” from Xiamen to Wuxi are ramping GaAs/AlGaAs lines exclusively for VCSELs.

- Automotive alliances: Chinese lidar start-ups such as Hesai and Robosense now co-design custom multi-junction VCSEL arrays with domestic epi suppliers, shortening design cycles and lowering bill of materials.

- Supply-chain resilience: After chip shortages in 2021–22, global Tier-1s want a dual-sourcing strategy that includes at least one Chinese vendor.

The payoff is clear: China’s VCSEL revenue is forecast to triple by 2032, closing the gap with the U.S.

Inside the Device: Why VCSELs Win

VCSELs emit perpendicular to the wafer surface, allowing on-wafer testing and dense 2-D arrays. Edge-emitters still win at high continuous-wave power, but VCSELs dominate when size, yield, and integration are paramount. Their circular beam, narrow divergence, and low speckle are ideal for depth sensing, while their low threshold currents permit operation from coin-cell batteries.

Corporate Moves – M&A Heats Up

Thorlabs × Praevium Research: Tunable VCSELs Go Mainstream

In January 2025, U.S. photonics powerhouse Thorlabs acquired Praevium Research, a California company famed for MEMS-tuned VCSELs used in swept-source OCT scanners. The deal folds Praevium’s agile-wavelength technology into Thorlabs’ vertically integrated manufacturing stack, promising cheaper and faster tunable sources for biomedical imaging.

What it Means

- Consolidation of IP: Thorlabs now holds dozens of Praevium patents covering MEMS mirrors and broadband DBRs.

- Lower system cost: Integrating tunable VCSEL engines with Thorlabs’ detectors could shave 15–20 % off OCT bill-of-materials, broadening adoption beyond ophthalmology.

- Competitive pressure: Rival swept-source vendors will need to rethink cost structures, possibly driving another wave of mergers.

Wavelength Breakthrough – The First Blue VCSELs

Until recently, commercial VCSELs were confined to the near-IR and red bands. Nichia broke new ground in June 2025 at Laser World of Photonics (Munich), unveiling a 442 nm blue VCSEL prototype. This is more than a lab curiosity—it could:

- Revolutionize AR/VR micro-displays. Blue arrays are the missing puzzle piece for full-color RGB lasers on silicon waveguides.

- Enable compact underwater LiFi links, where blue light tolerates aquatic attenuation better than IR.

- Open a path to visible-light lidar, potentially sidestepping eye-safety power limits in the near-IR.

Challenges remain—chiefly epitaxial defects in GaN/AlGaN VCSELs and mirror design—but the proof-of-concept moved the goalposts.

Validation from the Press – “Star Still Shining Bright”

A March/April 2025 SPIE Photonics Focus feature declared that VCSELs have cemented dominance in low-power, short-distance optical links, edging out traditional edge-emitters, especially in consumer electronics and automotive cabins. The article spotlighted:

- The higher percentage yield per wafer

- Simplified passive alignment in module assembly

- Resilience to vibration—critical in cars and drones

The take-home: incremental efficiency gains haven’t plateaued yet, and VCSELs still enjoy a healthy innovation runway.

The Looming Rival – PCSELs vs. VCSELs

While VCSEL market share is safe in the short term, photonic-crystal surface-emitting lasers (PCSELs) are nipping at their heels. An April 2024 Photonics Media analysis highlighted PCSELs’ ultra-narrow beam divergence—down to 0.1°—and scalability to several watts without external optics. For long-range automotive lidar (> 200 m), PCSELs could eventually displace large VCSEL arrays. For now, hybrid systems that pair VCSEL flood illuminators with scanning PCSELs are appearing in R&D roadmaps.

Automotive Takes Center Stage

Sony’s SPAD Depth Sensor

Sony Semiconductor has commercialized a single-photon avalanche diode (SPAD) depth sensor pitched at automotive lidar. The reference design spotlights VCSEL arrays as the illumination engine, reinforcing the “solid-state + CMOS” synergy being embraced by Tier-1 automotive suppliers.

ams OSRAM’s EVIYOS™ Shape

At CES 2025, ams OSRAM showcased EVIYOS™ Shape—a 25 600-pixel adaptive micro-LED array whose underlying VCSEL driver platform was derived from its IR illumination business. The pitch: pixel-by-pixel road-sign projection and glare-free high beams in a single chip.

Together, these announcements cement VCSEL arrays as the de-facto illumination source for the next generation of advanced driver-assistance systems (ADAS) and smart headlights.

Beyond the Car – Consumer & Industrial Momentum

Smartphones & Tablets

Face-authentication installs now exceed 1.5 billion units globally, and Apple’s entry into spatial computing with Vision Pro doubled per-device VCSEL content (eye-tracking, hand-tracking, spatial mapping). Android OEMs from Samsung to Xiaomi have followed.

Industrial IoT & Logistics

Warehouses deploy VCSEL-based Time-of-Flight (ToF) cameras for shelf scanning and autonomous forklift navigation. With e-commerce fulfillment times shrinking to same-day windows, accuracy and uptime trump the modest cost premium over LED flood illumination.

Optical Interconnects in AI Servers

VCSEL-powered multi-fiber MPO links at 100G/lane are the workhorse inside data-center GPUs. As generative-AI clusters scale, single-mode on-board optics (OBO) at 1310 nm are on the horizon, but analysts believe IR VCSELs will remain dominant for short-reach (< 100 m) backplane links throughout the forecast window.

Healthcare – Tunable VCSELs Democratize OCT

Swept-source OCT historically cost six figures, limiting use to retinal specialists. Tunable MEMS-VCSEL engines from Praevium (now Thorlabs) offer sweep rates up to 400 kHz, enabling compact desktop scanners priced under US $25 000. This could unlock primary-care screenings for diabetic retinopathy and even point-of-care dental imaging.

Manufacturing and Supply Chain Shifts

- Epitaxy Gets Smarter: AI-driven metrology now detects wafer-level defects after the first DBR deposition, improving overall yield by 7–10 %.

- Hybrid Bonding: Apple’s packaging team popularized copper-to-copper hybrid bonding between VCSEL chips and driver ASICs. Several OSATs in Taiwan and China are adding capacity, slashing assembly cycle time from minutes to seconds.

- Recycling GaAs: Circular-economy pilots in Germany are reclaiming GaAs substrates, reducing raw-material cost pressure and lowering environmental impact.

R&D Investment – Follow the Money

A 2025 survey of 120 photonics R&D budgets found that 70 % of spending is earmarked for energy-efficient laser diodes, and 66 % for thermal-management solutions. VCSEL modules top both lists, out-pacing silicon photonics and micro-LEDs.

Standards & Regulation

- IEC 60825-1 (Ed. 3.2) revisions tighten eye-safety calculations for wavelength bands 1300–1400 nm but leave the 850–940 nm VCSEL sweet-spot largely unchanged.

- UNECE lidar guidelines (2024) require functional-safety clauses in VCSEL driver ASICs—boosting demand for integrated self-test circuitry.

- U.S.–China Export Controls: The October 2024 Commerce Department rules added certain high-performance VCSEL drivers to the entity list. So far, exemptions for automotive and medical shipments have kept the supply chain moving, but dual-use scrutiny is rising.

Forecast Methodology

Our 10.2 % CAGR projection blends bottom-up unit forecasts (smartphones, cars, servers, wearables) with a top-down macro filter (GDP growth, semiconductor capital intensity). We model ASP erosion at 6 % per year—slower than historical norms—thanks to richer multi-VCSEL modules and specialty wavelengths entering production.

- Base case: $4.12 B by 2032

- Bull case (aggressive AR/VR adoption): $4.95 B

- Bear case (auto-lidar slowdown): $3.55 B

Application Split – 2032 Outlook

| Application | Revenue Share | Key Notes |

| Consumer 3D-sensing | 34 % | Saturated smartphone market but rising ASP per module |

| Automotive (lidar + DMS) | 28 % | Standard on L3+ vehicles by 2029 |

| Datacom & AI servers | 18 % | Co-packaged optics keeps IR VCSELs relevant |

| Industrial & IoT | 11 % | Logistics robots, factory ToF cameras |

| Healthcare & Life Sciences | 9 % | Low-cost OCT, flow cytometry innovations |

Success Factors for Vendors

- Spectrum Agility: Firms that master wavelengths from 650 nm to 1310 nm will own future AR displays and silicon photonics interposers.

- Packaging Integration: Wafer-level optics and hybrid bonding drive cost and footprint advantages.

- Automotive Functional Safety: ISO 26262-compliant VCSEL drivers with redundant monitoring are a ticket to the auto supply chain.

- Localized Supply: Dual fabs—one in North America/Europe, one in Asia—mitigate geopolitical risk.

- IP Portfolio: A strong patent moat around DBR design, current-spread control, and thermal shunts deters commoditization.

Risks and Challenges

- Thermal Runaway in Dense Arrays – Requires novel gold/tungsten heat spreaders and predictive drive algorithms.

- Competing Architectures – PCSELs and micro-LED flood illuminators could steal share in mid-decade.

- Regulatory Shocks – Export-control expansions or stricter eye-safety rules could derail timelines.

- Supply-Chain Black Swans – Gallium and arsenic price volatility, or geopolitical disruptions in epi-wafer hotspots.

Strategic Recommendations

- OEMs: Lock in second-source VCSEL suppliers now; diversify across at least two regions.

- Foundries: Invest in GaAs reclaim and high-volume DBR MOCVD reactors; blue VCSEL epi is a longer-term but higher-margin bet.

- System Integrators: Bundle eye-safety firmware and driver ICs into module quotes; end customers increasingly want turnkey solutions.

- Start-ups: Focus on specialized niches—visible VCSELs for AR waveguides, or ultra-high-power IR arrays for industrial cutting—to avoid head-on wars with tier-one giants.

- Investors: Watch for companies that marry VCSEL IP with AI inference hardware; co-packaged optics will blur the line between photonics and compute.

Doubling Down on Photonic Potential

VCSELs have journeyed from niche component to cornerstone technology powering the sensing economy. The next seven years will see them integrated into more cars, cameras, servers, and head-worn computers than ever imagined when the first commercial devices shipped in the mid-1990s. Yet the real story is qualitative: expanding into new colors, new materials, and new market footholds. With macros pointing to US $4.12 billion in annual revenue by 2032, the VCSEL ecosystem—fabricators, equipment vendors, packagers, and software stack developers—stands on the cusp of its most transformative decade.

Stakeholders that invest early in spectrum agility, functional safety, and vertically integrated supply chains are poised to capture outsized rewards. For everyone else, the message is clear: adapt quickly or watch opportunity evaporate in a puff of photonic progress.

Comments (0)